Your Ultimate Guide to a $7000 Car Loan Payment: Drive Smart, Not Hard

Your Ultimate Guide to a $7000 Car Loan Payment: Drive Smart, Not Hard Carloan.Guidemechanic.com

Embarking on the journey to purchase a car, especially with a specific budget in mind like a $7000 car loan, can feel like navigating a complex maze. It’s not just about finding a vehicle; it’s about understanding the financial mechanics that determine your actual car loan payment. A $7000 car loan doesn’t mean your monthly payment will be $7000; it refers to the principal amount you intend to borrow. This figure is often a sweet spot for those looking for an affordable, reliable used car or a secondary vehicle without breaking the bank.

Based on my extensive experience in automotive financing and personal finance, securing a loan for $7000 requires careful planning and a deep understanding of several key factors. This comprehensive guide is designed to demystify the process, empower you with knowledge, and help you make informed decisions. Our ultimate goal is to help you secure a $7000 car loan payment that fits comfortably within your budget, without any hidden surprises.

Your Ultimate Guide to a $7000 Car Loan Payment: Drive Smart, Not Hard

In this article, we’ll dive deep into everything from interest rates and loan terms to credit scores and the all-important application process. We’ll explore where to find the best loans, common pitfalls to avoid, and crucial tips for managing your loan effectively. By the end, you’ll be well-equipped to navigate the world of car financing with confidence and secure a great deal.

Understanding the $7000 Car Loan: The Basics

When we talk about a "$7000 car loan," we are referring to the principal amount of money you borrow to purchase a vehicle. This typically means you are looking at used cars, as new vehicles rarely fall within this price range unless you’re making a substantial down payment. The used car market offers a wide variety of options at this price point, from older, well-maintained sedans to compact SUVs.

Many individuals seek a loan of this size for various reasons. It might be for a first-time driver, a college student needing reliable transportation, a family requiring a second vehicle, or someone simply looking for an affordable daily commuter. Whatever your motivation, understanding the fundamentals of this loan amount is the first step towards a smart purchase. It’s not just about the sticker price; it’s about the total cost of ownership over time.

Securing a $7000 car loan payment that is manageable involves looking beyond the monthly figure. It means evaluating the overall financial commitment and ensuring it aligns with your long-term financial goals. Let’s break down the core components that will shape your borrowing experience.

Key Factors Influencing Your $7000 Car Loan Payment

Your monthly payment for a $7000 car loan isn’t a fixed number; it’s a dynamic figure influenced by several critical variables. Understanding these factors is paramount to securing an affordable loan and avoiding financial strain. Let’s explore each one in detail.

1. The All-Important Interest Rate

The interest rate is arguably the most significant factor affecting your $7000 car loan payment. This is the cost you pay to borrow the money, expressed as a percentage of the principal loan amount. A higher interest rate means more money paid back to the lender over the life of the loan, directly increasing your monthly payment.

Interest rates are influenced by a multitude of factors, with your credit score being the primary determinant. Lenders assess your creditworthiness to gauge the risk involved in lending to you. A borrower with an excellent credit score (typically 760+) is considered low-risk and will likely qualify for the lowest available rates, sometimes even under 5%. Conversely, a borrower with a lower credit score (below 620) presents a higher risk, resulting in significantly higher interest rates, which can sometimes exceed 20% or even higher for a used car.

Market conditions, such as the prime rate set by the Federal Reserve, also play a role. When overall interest rates are high, car loan rates tend to follow suit. Different lenders—banks, credit unions, and online lenders—also offer varying rates, making it crucial to shop around. Pro tip from us: Don’t settle for the first offer you receive; comparing rates from multiple lenders can save you hundreds, if not thousands, of dollars over the loan term.

2. Loan Term: Shorter vs. Longer Repayment Periods

The loan term, or repayment period, is the length of time you have to pay back the borrowed money, typically expressed in months (e.g., 36, 48, 60 months). This factor has a direct, inverse relationship with your monthly payment and a direct relationship with the total interest paid. A longer loan term will result in lower monthly payments, which might seem attractive at first glance.

However, a longer term also means you’ll be paying interest for a longer period, significantly increasing the total amount you pay back over the life of the loan. For a $7000 car loan, common terms range from 36 to 60 months. Opting for a 60-month term might make your monthly payments more manageable, but you’ll likely pay more in total interest compared to a 36-month term.

It’s a delicate balance: choose a term that makes your monthly payment affordable without extending it so long that you end up paying excessive interest. Based on my experience, for a smaller loan like $7000, a shorter term (36-48 months) is often more financially prudent if your budget allows. This helps you pay off the car faster and minimize total interest costs.

3. The Power of a Down Payment

A down payment is an initial sum of money you pay upfront towards the purchase price of the car, reducing the amount you need to borrow. While it might seem counterintuitive to part with cash upfront, a down payment is a powerful tool for lowering your $7000 car loan payment and improving your overall loan terms. Even a small down payment can make a significant difference.

When you make a down payment, you reduce the principal amount of the loan, which in turn lowers your monthly payments. Furthermore, lenders often view borrowers who make a down payment as less risky, potentially qualifying you for a better interest rate. This is because you have a direct financial stake in the vehicle, indicating a higher likelihood of repayment.

For a $7000 car loan, putting down even $500 or $1000 can substantially impact your monthly obligation and total interest paid. It’s always a good strategy to save up for a down payment if possible, as it demonstrates financial discipline and can unlock better loan opportunities.

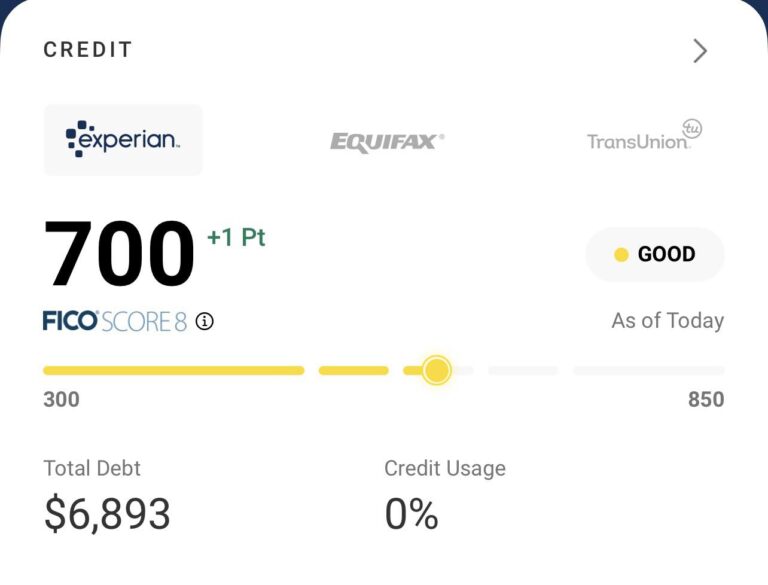

4. Your Credit Score: The Financial Gatekeeper

Your credit score is a numerical representation of your creditworthiness, derived from your credit history. It is a critical determinant of the interest rate you’ll be offered for your $7000 car loan. Lenders use this three-digit number to assess your reliability in repaying debts.

- Excellent Credit (760-850): You’ll receive the most competitive interest rates and favorable terms.

- Good Credit (700-759): You’ll still qualify for very good rates, though perhaps not the absolute lowest.

- Fair Credit (620-699): You can likely get approved, but expect higher interest rates.

- Poor Credit (300-619): Approval might be challenging, and interest rates will be significantly higher, often making the loan much more expensive.

Before applying for any car loan, it’s a pro tip from us to check your credit report from all three major bureaus (Experian, Equifax, TransUnion). Look for any errors that could be negatively impacting your score and dispute them immediately. Even a slight improvement in your score can translate to noticeable savings on your interest rate. If your credit score isn’t where you want it to be, consider taking steps to improve it before applying, such as paying down existing debts or making all payments on time. (For more detailed advice, you might find our article on (Internal Link 1 Placeholder) helpful.)

5. Other Costs to Consider

Beyond the principal and interest, several other costs contribute to the overall expense of owning a car, and some directly impact your initial outlay or ongoing budget. Ignoring these can lead to unexpected financial strain.

- Taxes and Fees: Depending on your state and local regulations, you’ll likely pay sales tax on the vehicle purchase. There may also be documentation fees, registration fees, and title fees. These are typically rolled into the loan or paid upfront.

- Car Insurance: When you finance a car, lenders almost always require you to carry full coverage insurance (collision and comprehensive) to protect their asset. The cost of insurance can vary wildly based on the car’s value, your driving record, age, and location. For a $7000 used car, insurance might even be a significant portion of your total monthly car expenses.

- Maintenance and Repairs: A $7000 car is usually a used vehicle, meaning it might require more frequent maintenance or unexpected repairs. It’s crucial to factor in a budget for these potential costs. A pre-purchase inspection by a trusted mechanic is highly recommended for any used car, especially in this price range.

Calculating Your Potential $7000 Car Loan Payment

While specific calculations require an online car loan calculator, understanding the components helps you estimate your potential payments. The primary variables are the loan amount ($7000), the interest rate (APR), and the loan term.

Let’s consider some hypothetical scenarios to illustrate the impact:

- Scenario 1: Excellent Credit

- Loan Amount: $7,000

- Interest Rate (APR): 5%

- Loan Term: 36 months

- Estimated Monthly Payment: Around $210 (Total interest paid: ~$550)

- Scenario 2: Good Credit

- Loan Amount: $7,000

- Interest Rate (APR): 8%

- Loan Term: 48 months

- Estimated Monthly Payment: Around $170 (Total interest paid: ~$1,150)

- Scenario 3: Fair Credit

- Loan Amount: $7,000

- Interest Rate (APR): 15%

- Loan Term: 60 months

- Estimated Monthly Payment: Around $165 (Total interest paid: ~$2,900)

As you can see, even with a smaller loan amount like $7000, interest rates and loan terms drastically affect both your monthly payment and the total cost of the loan. A common mistake to avoid is focusing solely on the lowest monthly payment without considering the total interest you’ll pay over the loan’s life. Always aim for the shortest term you can comfortably afford.

The Application Process for a $7000 Car Loan

Securing a $7000 car loan payment involves more than just filling out a form. A strategic approach can significantly improve your chances of approval and help you land the best possible terms.

Step 1: Budgeting and Financial Health Check

Before even looking at cars, honestly assess your financial situation. How much can you truly afford each month for a car payment, including insurance, fuel, and potential maintenance? Use a budget spreadsheet to track your income and expenses. A general rule of thumb is that your total car expenses (payment, insurance, fuel) shouldn’t exceed 10-15% of your net monthly income.

Based on my experience, many people overlook the total cost of ownership. A $7000 car might seem cheap, but if it requires frequent repairs or has high insurance premiums, it can quickly become a financial burden. Be realistic about your spending limits.

Step 2: Get Your Credit Report in Order

As discussed, your credit score is vital. Obtain your free annual credit reports from AnnualCreditReport.com. Review them thoroughly for any inaccuracies that could hurt your score. Dispute any errors immediately. Knowing your credit score upfront empowers you to set realistic expectations for interest rates and allows you to address any issues before applying.

Step 3: Pre-Approval is Your Power Play

Getting pre-approved for a loan before you visit a dealership is one of the smartest moves you can make. Pre-approval means a lender has conditionally agreed to lend you a specific amount (in this case, up to $7000) at a certain interest rate, based on your creditworthiness. This gives you immense negotiation leverage at the dealership.

With a pre-approval in hand, you know exactly how much you can afford and what interest rate you qualify for. This separates the financing negotiation from the car price negotiation, allowing you to focus on getting the best deal on the vehicle itself. You can then compare the dealership’s financing offer against your pre-approval and choose the better option.

Step 4: Gather Your Documentation

Lenders will require various documents to verify your identity, income, and residency. Having these ready will streamline the application process. Common documents include:

- Government-issued photo ID (driver’s license, passport)

- Proof of income (pay stubs, tax returns, bank statements)

- Proof of residency (utility bill, lease agreement)

- Social Security number

- Vehicle information (once you’ve chosen a car)

Step 5: Compare Multiple Offers

This cannot be stressed enough. Whether you’re getting pre-approved or applying directly, solicit offers from at least three to five different lenders. This includes banks, credit unions, and online lenders. Credit unions, in particular, often offer very competitive rates, especially for smaller loan amounts like $7000, due to their member-focused structure.

Pro tip: Multiple credit applications within a short period (typically 14-45 days, depending on the credit scoring model) for the same type of loan are usually counted as a single inquiry. This means you can shop for rates without significantly damaging your credit score. Don’t be afraid to leverage this "rate shopping" window.

Where to Find a $7000 Car Loan

The landscape for car loans is diverse, offering several avenues for securing your $7000 financing. Each option has its own advantages and disadvantages.

- Traditional Banks: Large national and regional banks are a common source for car loans. They offer a wide range of products and often have competitive rates for borrowers with excellent credit. However, their approval processes can sometimes be slower, and they might be less flexible for those with less-than-perfect credit for smaller loan amounts.

- Credit Unions: These member-owned financial institutions are often an excellent choice, especially for a $7000 car loan. Credit unions are known for offering lower interest rates and more personalized service, particularly to their members. If you’re not already a member, consider joining one; the benefits often outweigh the initial effort.

- Online Lenders: Companies like LightStream, Capital One Auto Finance, and many others specialize in online auto loans. They offer convenience, quick approvals, and competitive rates, often catering to a broader range of credit profiles. Their streamlined digital process can be appealing for busy individuals.

- Dealership Financing: Most car dealerships offer financing options, often through partnerships with various banks and captive finance companies (e.g., Toyota Financial Services). While convenient, as it’s a one-stop shop, their rates might not always be the most competitive. Always compare their offer with your pre-approval or other independent loan offers. Common mistake to avoid: relying solely on dealership financing without comparing other options.

Special Considerations for a $7000 Car Loan

A $7000 car loan often comes with unique circumstances that merit specific attention.

Used Car Market Realities

For $7000, you will almost certainly be purchasing a used car. This means extra diligence is required.

- Pre-Purchase Inspection: Never buy a used car without a thorough inspection by an independent, trusted mechanic. This small investment can save you thousands in future repair costs. They can identify hidden issues that aren’t apparent during a test drive.

- Vehicle History Reports: Obtain a CarFax or AutoCheck report. These reports provide crucial information about the car’s past, including accident history, previous owners, service records, and odometer discrepancies. This transparency is vital for a used car in this price range. (You can learn more about vehicle history reports from trusted sources like the National Highway Traffic Safety Administration – External Link Placeholder: NHTSA Used Car Checklist).

- Reliability vs. Cost: For a $7000 car, prioritize reliability and lower maintenance costs over fancy features. Research models known for their longevity and inexpensive parts.

Navigating Bad Credit or No Credit

If your credit score is low or you have no credit history, securing a $7000 car loan payment can be more challenging, but it’s not impossible.

- Higher Interest Rates: Expect significantly higher interest rates, which will increase your monthly payment and total cost. Be prepared for rates in the double digits.

- Co-signer Option: A co-signer with good credit can significantly improve your chances of approval and help you secure a better interest rate. However, remember that the co-signer is equally responsible for the loan, and their credit will be affected if you miss payments.

- Secured Loans: Some lenders offer secured loans where the car itself acts as collateral. These can be easier to obtain with bad credit but come with the risk of repossession if you default.

- Realistic Expectations: Be realistic about the type of car you can afford and the terms you’ll receive. Focus on making all payments on time to build positive credit history, which will help you qualify for better loans in the future.

Refinancing Possibilities

If you initially secure a $7000 car loan with a high interest rate (perhaps due to a lower credit score at the time), refinancing might be an option down the line. Refinancing involves taking out a new loan to pay off your existing one, ideally with a lower interest rate or better terms.

This can be particularly beneficial if your credit score has improved since you first took out the loan. Refinancing can potentially lower your monthly payments, reduce the total interest paid, or shorten your loan term. It’s always worth exploring if your financial situation has improved a year or two into your loan. (We have an article on (Internal Link 2 Placeholder) that covers this in more detail.)

Pro Tips for Smart $7000 Car Loan Management

Once you’ve secured your $7000 car loan, smart management can save you money and keep your finances healthy.

- Make Extra Payments: If your budget allows, make extra payments whenever possible. Even an additional $25-$50 per month can significantly reduce the total interest paid and shorten your loan term. Apply these extra payments directly to the principal.

- Set Up Auto-Pay: Automate your monthly payments to ensure you never miss a due date. This protects your credit score and helps you avoid late fees.

- Monitor Your Credit: Continue to monitor your credit report regularly. A good payment history on your car loan will positively impact your score, opening doors for better financial opportunities in the future.

- Build an Emergency Fund: For a $7000 used car, unexpected repairs are a real possibility. Having an emergency fund dedicated to car maintenance will prevent you from going into further debt or defaulting on your loan if a major repair arises.

- Understand Your Loan Agreement: Read the fine print of your loan agreement carefully. Know your interest rate, payment schedule, any prepayment penalties (rare for car loans but good to check), and what happens if you miss a payment.

Common Mistakes to Avoid When Taking Out a $7000 Car Loan

Even with the best intentions, it’s easy to fall into common traps. Here are some mistakes to actively avoid:

- Not Budgeting Properly: Failing to account for all car-related expenses (insurance, fuel, maintenance) beyond the loan payment can lead to financial stress.

- Focusing Only on Monthly Payment: While an affordable monthly payment is important, obsessing over the lowest possible payment can lead to longer loan terms and significantly more interest paid.

- Ignoring Total Cost of the Loan: Always calculate the total amount you’ll pay over the life of the loan (principal + total interest). A seemingly low monthly payment over a very long term can result in a shockingly high total cost.

- Skipping Pre-Approval: Going to the dealership without a pre-approval puts you at a disadvantage in negotiations.

- Not Checking Vehicle History or Getting an Inspection: For a $7000 used car, this is non-negotiable. Don’t let excitement override due diligence.

- Impulse Buying: Take your time. Research cars, compare loans, and make a decision free from pressure. An impulse car purchase, especially for a used vehicle, often leads to buyer’s remorse.

Conclusion: Drive Smart, Not Hard with Your $7000 Car Loan

Securing a $7000 car loan payment can be a straightforward and rewarding experience if approached with knowledge and strategy. It’s about empowering yourself with information, understanding the financial levers at play, and making choices that align with your budget and long-term financial health. From optimizing your credit score and making a down payment to shopping for the best interest rates and carefully considering the loan term, every step contributes to a more affordable and manageable loan.

Remember, a $7000 car loan represents not just a vehicle, but an investment in your mobility and independence. By avoiding common pitfalls and applying the pro tips outlined in this guide, you can navigate the process with confidence, secure a favorable loan, and enjoy your new-to-you car without financial worries. Start your journey wisely, and happy driving!