Your Ultimate Guide to a Springboard Car Loan: Drive Towards Financial Freedom

Your Ultimate Guide to a Springboard Car Loan: Drive Towards Financial Freedom Carloan.Guidemechanic.com

Getting a car is often more than just acquiring a vehicle; it’s a significant step towards independence, convenience, and sometimes, a crucial opportunity to build your financial future. For many, navigating the world of auto financing can feel like a complex maze. This is where the concept of a "Springboard Car Loan" comes into play. It’s not just about getting a loan; it’s about strategically using a car loan to propel you towards better financial standing, improved credit, and ultimately, greater financial freedom.

In this super comprehensive guide, we’ll dive deep into every facet of securing a car loan, especially for those looking to leverage it as a "springboard." Whether you’re a first-time buyer, someone with less-than-perfect credit, or simply looking to make a smart financial move, this article is designed to provide you with actionable insights, expert tips, and a clear roadmap. Our goal is to empower you with the knowledge to make informed decisions, avoid common pitfalls, and confidently drive away with a loan that truly serves your long-term financial health. Let’s unlock the secrets to a successful car loan journey together.

Your Ultimate Guide to a Springboard Car Loan: Drive Towards Financial Freedom

What Exactly is a "Springboard Car Loan" (and Why It Matters)?

The term "Springboard Car Loan" isn’t a specific financial product you’ll find advertised by lenders. Instead, it’s a strategic approach to vehicle financing, designed to give you a solid footing or an upward boost in your financial journey. It’s about more than just getting approved for a car loan; it’s about securing a loan on terms that allow you to manage payments effectively, build positive credit history, and open doors to future financial opportunities.

Think of it as using your car loan as a stepping stone. For some, it might be the first significant loan they acquire, establishing their creditworthiness. For others, particularly those with past credit challenges, it represents a chance to demonstrate responsible financial behavior and repair their credit score. The ultimate aim is to use the loan as a tool to improve your financial profile, not just to purchase a car.

Based on my experience, many people simply focus on the lowest monthly payment without considering the broader financial implications. A Springboard Car Loan, however, encourages a holistic view, emphasizing affordability, responsible borrowing, and long-term financial benefits. It’s an investment in both your transportation and your financial future.

Key Pillars to a Successful Springboard Car Loan Application

Securing any loan requires preparation, but a Springboard Car Loan demands a more strategic approach. By focusing on these core pillars, you’ll significantly enhance your chances of approval and ensure the loan serves your financial goals.

Understanding Your Credit Score: The Foundation

Your credit score is arguably the most critical factor lenders consider when you apply for a car loan. It’s a numerical representation of your creditworthiness, indicating how reliably you’ve managed debt in the past. A higher score typically translates to better interest rates and more favorable loan terms.

Why It’s Crucial: Lenders use your credit score to assess the risk of lending to you. A good score tells them you’re likely to repay your loan on time, making them more willing to offer competitive rates. Conversely, a low score suggests higher risk, often resulting in higher interest rates or even loan denial.

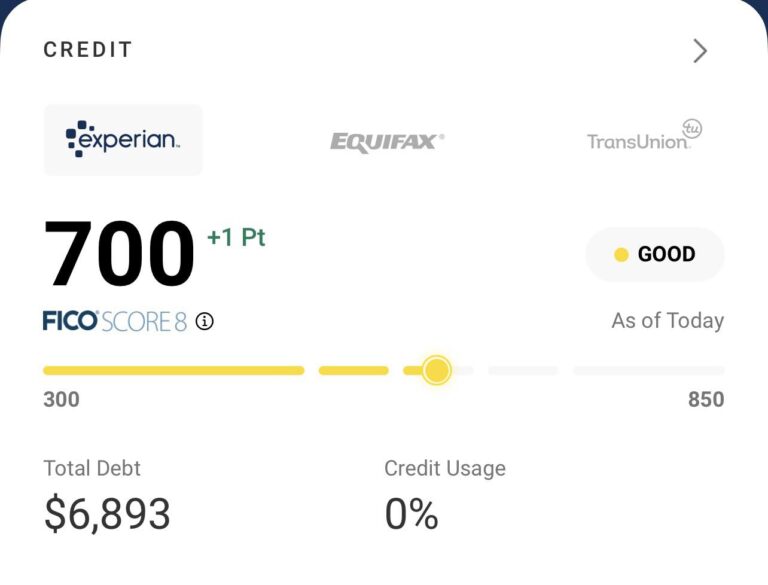

How to Check It: Before you even think about applying, pull your credit reports from all three major bureaus: Equifax, Experian, and TransUnion. You’re entitled to a free report from each once a year via AnnualCreditReport.com. Review these reports meticulously for any inaccuracies, as errors can negatively impact your score.

Impact of Different Score Ranges: Generally, scores above 700 are considered good to excellent, qualifying you for the best rates. Scores between 600-699 are fair to good, still allowing for approval but with slightly higher rates. Below 600, you’ll likely face subprime rates or need to explore specific bad credit lenders. Understanding where you stand is your first step.

Tips for Improving It Before Applying: If your score isn’t where you want it, take steps to improve it. Pay down existing debts, especially high-interest credit card balances, and ensure all your bills are paid on time. Avoid opening new credit accounts right before applying for a car loan, as this can temporarily lower your score.

Pro tips from us: Always dispute any errors you find on your credit report immediately. Even small discrepancies can impact your score, and correcting them can give you a vital boost. Patience and diligent credit management are your best allies here.

Budgeting and Affordability: Beyond the Monthly Payment

Many prospective car buyers make the mistake of focusing solely on the monthly payment. While it’s an important factor, a true understanding of affordability requires a much broader perspective. A Springboard Car Loan emphasizes a realistic view of your financial capacity.

Don’t Just Look at Monthly Payments: A low monthly payment might seem attractive, but it often comes with a longer loan term, meaning you pay more interest over the life of the loan. Always consider the total cost of the loan, including interest, over its entire duration. This long-term view is essential for smart financial planning.

Total Cost of Ownership (TCO): Beyond the loan itself, remember the other costs associated with car ownership. These include insurance premiums, fuel, routine maintenance, repairs, registration fees, and potential parking costs. These expenses can quickly add up and impact your overall budget. Neglecting TCO is a common oversight.

Debt-to-Income Ratio (DTI): Lenders look at your DTI, which is the percentage of your gross monthly income that goes towards debt payments. A lower DTI (ideally below 36%) indicates you have enough disposable income to comfortably manage new debt. This ratio is a strong indicator of your financial health.

How Much Can You Truly Afford?: Create a detailed budget that accounts for all your income and expenses. Be honest with yourself about what you can comfortably pay each month without straining your finances. This includes considering your emergency fund and other savings goals. Your car loan should fit seamlessly into your financial life, not dominate it.

Common mistakes to avoid are: Underestimating the true cost of car ownership and allowing yourself to be swayed by a dealer who only highlights the monthly payment. Always calculate the total cost, including all associated expenses, before committing.

Down Payment Power: Your Financial Head Start

A down payment is the initial sum of money you pay upfront for the car. It directly reduces the amount you need to borrow, and its strategic use can significantly impact your loan terms and overall financial well-being. This is a powerful component of a Springboard Car Loan.

Benefits of a Larger Down Payment:

- Lower Monthly Payments: Less money borrowed means smaller installments.

- Less Interest Paid: You’re financing a smaller amount, so you accrue less interest over the loan term.

- Better Loan Terms: Lenders see a larger down payment as a sign of financial commitment and lower risk, often leading to more favorable interest rates.

- Reduced Loan-to-Value (LTV): A higher down payment means your LTV ratio is lower. This is the amount you owe on the car compared to its value. A lower LTV is always beneficial.

- Protection Against Negative Equity: Cars depreciate rapidly. A substantial down payment helps ensure you don’t owe more on the car than it’s worth, especially in the early years of ownership.

How It Affects LTV: If a car costs $20,000 and you put down $4,000, your loan-to-value is 80% ($16,000 loan / $20,000 car value). A lower LTV is less risky for the lender and better for you. Aim for at least 10-20% if possible.

Strategies for Saving for a Down Payment: Start saving early and consistently. Consider setting up an automatic transfer from your checking to a dedicated savings account. Look for ways to cut unnecessary expenses or earn extra income temporarily. Every dollar saved for a down payment is a dollar you won’t pay interest on.

Choosing the Right Vehicle: A Strategic Match

The car you choose plays a crucial role in your Springboard Car Loan strategy. It’s not just about what you like, but what makes financial sense for your current situation and future goals.

New vs. Used – Pros and Cons for "Springboard" Purposes:

- New Cars: Offer the latest features, warranties, and often better financing rates (though not always for those with challenged credit). However, they depreciate significantly the moment you drive them off the lot, making them a less ideal "springboard" for building equity quickly.

- Used Cars: Generally more affordable, depreciate slower after the initial drop, and can offer excellent value. For a Springboard Car Loan, a reliable used car often presents a better opportunity to secure a manageable loan and avoid immediate negative equity.

Reliability and Depreciation: Opt for a vehicle known for its reliability and slower depreciation rates. Research brands and models that hold their value well. A car that constantly needs repairs will drain your finances and undermine your "springboard" efforts. Websites like Consumer Reports or JD Power provide valuable reliability data.

Researching Vehicle Value: Always research the market value of the specific car you’re interested in. Use resources like Kelley Blue Book (KBB), Edmunds, or NADA Guides to determine fair pricing for both new and used vehicles. This knowledge empowers you to negotiate effectively and avoid overpaying.

Navigating the Springboard Car Loan Application Process

Once you’ve laid the groundwork, it’s time to approach the application process with confidence and a clear strategy. This phase is where your preparation truly pays off.

Pre-Approval: Your Secret Weapon

Pre-approval is a game-changer in the car buying process. It’s an initial assessment by a lender to determine how much they’re willing to lend you, based on a soft credit inquiry. This is a crucial step for anyone seeking a Springboard Car Loan.

What It Is and Why It’s Beneficial: A pre-approval gives you a concrete loan offer, including the maximum amount, interest rate, and terms, before you even step foot in a dealership.

- Bargaining Power: You walk into the dealership as a cash buyer, knowing exactly how much you can spend. This shifts the negotiation power in your favor, allowing you to focus on the car price, not just the monthly payment.

- Clear Budget: It sets a realistic budget, preventing you from falling in love with a car you can’t truly afford.

- Avoids Multiple Hard Inquiries: Pre-approval typically involves a soft credit pull, which doesn’t affect your score. Once you’re ready to apply for the actual loan, the hard inquiry will occur. This prevents numerous hard inquiries from different dealers, which can ding your score.

How to Get Pre-Approved: You can apply for pre-approval directly through banks, credit unions, or online lenders. It’s a simple process, usually requiring basic personal and financial information. Aim to get pre-approved from a few different lenders to compare offers and find the best terms.

Gathering Your Documents: Be Prepared

The key to a smooth application process is preparation. Having all your necessary documents ready beforehand can save you time, stress, and potential delays.

List of Common Required Documents: While requirements can vary slightly by lender, typically you’ll need:

- Proof of Identity: Valid driver’s license or state ID.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Proof of Income: Recent pay stubs (usually 2-3 months), tax returns (for self-employed individuals), or bank statements.

- Social Security Number.

- Vehicle Information: If you’ve already chosen a car, details like VIN, make, model, and year.

- Proof of Insurance: You’ll need to show proof of adequate car insurance before driving the car off the lot.

Importance of Being Prepared: Having these documents organized and readily accessible demonstrates your seriousness and reliability to the lender. It streamlines the entire process, allowing for quicker approvals and less back-and-forth communication.

Where to Apply: Lenders and Options

Choosing the right lender is as important as choosing the right car. Different lenders cater to different financial profiles, and exploring your options is crucial for a Springboard Car Loan.

- Banks: Traditional banks often offer competitive rates for borrowers with good to excellent credit. They provide a sense of security and established customer service.

- Credit Unions: These member-owned financial institutions are known for offering lower interest rates and more flexible terms, especially for members. They often have a more personalized approach and can be more lenient with borrowers who have less-than-perfect credit.

- Online Lenders: A growing number of online platforms specialize in auto loans, often offering quick application processes and competitive rates. They can be particularly useful for comparing multiple offers from various lenders.

- Dealership Financing: While convenient, dealership financing sometimes marks up interest rates to profit from the loan. Always compare their offer with your pre-approval to ensure you’re getting the best deal.

Consider Subprime Lenders if Credit is Challenging: If your credit score is low, traditional lenders might deny your application. Subprime lenders specialize in loans for individuals with poor credit. While their interest rates are higher, they can be a viable "springboard" option if you make consistent, on-time payments to rebuild your credit.

Understanding Loan Terms and Interest Rates

The fine print of your loan agreement contains critical details that will impact your financial journey. Understanding these terms is non-negotiable for a successful Springboard Car Loan.

APR vs. Interest Rate: The Annual Percentage Rate (APR) is the true cost of borrowing, encompassing the interest rate plus any additional fees or charges. The interest rate is just the cost of borrowing the principal amount. Always compare APRs when evaluating loan offers, as it provides a more accurate picture of the total cost.

Loan Term Length (Shorter vs. Longer):

- Shorter Terms (e.g., 36-48 months): Lead to higher monthly payments but significantly less interest paid over the life of the loan. This is often the more financially savvy choice if you can afford the payments.

- Longer Terms (e.g., 60-84 months): Result in lower monthly payments, making the car seem more affordable. However, you’ll pay substantially more in interest over the extended period, and you risk owing more than the car is worth for longer.

Fixed vs. Variable Rates:

- Fixed Rate: Your interest rate remains the same throughout the entire loan term, providing predictable monthly payments. This is generally preferred for stability.

- Variable Rate: Your interest rate can fluctuate based on market conditions. While it might start lower, it carries the risk of increasing, leading to higher payments down the line. For a Springboard Car Loan, fixed rates offer more certainty.

Reading the Fine Print: Never sign a loan agreement without thoroughly reading and understanding every clause. Pay attention to prepayment penalties, late fees, and any other hidden charges. Don’t hesitate to ask your lender for clarification on anything you don’t understand.

In my years of advising clients on financial decisions, I’ve seen countless individuals overlook the critical importance of understanding these terms. A seemingly small difference in APR or an extended loan term can cost you thousands of dollars over time. Be diligent.

Special Considerations for Springboard Car Loans

A Springboard Car Loan is particularly valuable for specific financial situations. Let’s explore how it can be tailored to meet unique needs.

Bad Credit Car Loans: A True Springboard Opportunity

For those with a less-than-perfect credit history, securing a car loan can feel daunting. However, it can also be a significant opportunity to turn things around. This is where the "springboard" concept truly shines.

How to Approach a Loan with Poor Credit: Don’t despair. Many lenders specialize in bad credit car loans. The key is to approach them with realistic expectations and a solid plan. Your rates will likely be higher, but the goal is to get approved for a manageable loan and then diligently make payments.

What Lenders Look For: Lenders who offer bad credit loans focus on current financial stability. They’ll scrutinize your:

- Stable Income: Proof of consistent employment and sufficient income to cover payments.

- Co-signer: A co-signer with good credit can significantly improve your chances of approval and secure better terms. They share responsibility for the loan, so choose someone you trust and who understands the commitment.

- Larger Down Payment: As discussed, a larger down payment reduces the lender’s risk and shows your commitment.

The Goal: Use It to Rebuild Credit: The primary objective of a bad credit car loan, when viewed as a "springboard," is to establish a positive payment history. Every on-time payment you make is reported to credit bureaus, gradually improving your credit score. Over time, this improved score can open doors to better financial products.

- Read more about ‘Securing a Car Loan with Less-Than-Perfect Credit’ to gain further insights into navigating this specific challenge.

First-Time Buyers: Building Your Financial Foundation

If you’ve never taken out a loan before, you’re in a unique position. You might have excellent financial habits, but without a credit history, lenders have no data to assess your risk.

Challenges and Opportunities: The main challenge is the lack of a credit score. Lenders prefer to see a history of responsible borrowing. However, this also presents an opportunity to build a strong credit foundation from scratch.

Tips for Establishing Credit History:

- Secured Credit Card: Obtain a secured credit card, where you put down a deposit that acts as your credit limit. Use it responsibly and pay it off in full each month.

- Small Installment Loan: Consider a small personal loan, even if you don’t immediately need the funds, to demonstrate your ability to handle installment debt.

- Authorized User: Ask a trusted family member with good credit to add you as an authorized user on one of their credit cards. Their positive payment history can reflect on your report.

Co-signer Considerations: For first-time buyers, a co-signer is often the most effective way to secure a car loan with favorable terms. The co-signer’s established credit history provides the lender with the assurance they need. Again, ensure both parties understand the shared responsibility.

Refinancing Your Car Loan: The Ultimate Springboard

Refinancing means replacing your current car loan with a new one, often with a different lender. This is an incredible "springboard" strategy for improving your existing loan terms and saving money.

When and Why to Refinance:

- Improved Credit: If your credit score has significantly improved since you took out your original loan, you might qualify for a much lower interest rate.

- Lower Rates: Market interest rates may have dropped, or you might find a lender offering more competitive terms.

- Better Terms: You could shorten your loan term to pay it off faster and save interest, or lengthen it to reduce monthly payments (though this costs more in the long run).

- Remove a Co-signer: If your credit has improved, you might be able to refinance the loan in your name only, releasing your co-signer from their obligation.

How Refinancing Can Save You Money and Act as a Financial "Reset": A lower interest rate translates directly into less money spent over the life of the loan. By refinancing, you can significantly reduce your total cost of ownership, freeing up funds for other financial goals. It’s a powerful way to reset your financial path if your circumstances have improved.

Pro tips from us: Don’t just accept the first refinancing offer. Shop around aggressively, comparing rates and terms from multiple banks, credit unions, and online lenders. Just like your initial loan, competition among lenders can save you a lot.

The Post-Approval Phase: Making Your Springboard Work For You

Getting approved is just the beginning. The real work of leveraging your Springboard Car Loan for financial growth happens after you drive off the lot.

Making Timely Payments: Crucial for Credit Building

This is the cornerstone of making your car loan a true "springboard." Consistency is key.

Crucial for Credit Building: Every single on-time payment is reported to credit bureaus and contributes positively to your credit history. This consistent, responsible behavior is what builds a strong credit score over time. Missed payments, even one, can severely damage your credit.

Setting Up Auto-Pay: To avoid accidental late payments, set up automatic payments from your checking account. This ensures your payment is always made on time, every time, without you having to remember. It’s a simple yet highly effective strategy.

Monitoring Your Credit: Track Your Progress

Your credit score isn’t static; it evolves based on your financial activity. Regularly monitoring it helps you track the positive impact of your Springboard Car Loan.

Regularly Check Reports for Accuracy and Progress: Continue to pull your credit reports annually. Look for improvements in your score and ensure there are no new errors or unauthorized activity. Seeing your score improve can be incredibly motivating.

Considering Early Payoff: Save on Interest

Once you’ve established a solid payment history, you might consider paying off your car loan earlier than scheduled.

Benefits (Save Interest): Paying off your loan early significantly reduces the total amount of interest you pay. The quicker you eliminate debt, the more money you free up for other investments or savings.

Check for Prepayment Penalties: Before making extra payments or paying off the loan in full, carefully review your loan agreement for any prepayment penalties. Some lenders charge a fee for paying off the loan ahead of schedule. Most standard auto loans do not have these, but it’s always wise to check.

Building a Financial Buffer: For Peace of Mind

Car ownership comes with unexpected costs. Having an emergency fund dedicated to vehicle-related expenses is a smart financial move.

Emergency Fund for Car Repairs, Insurance, etc.: Set aside money specifically for unexpected repairs, higher-than-anticipated insurance premiums, or even a temporary lapse in income. This buffer prevents you from relying on credit cards or high-interest loans when an emergency strikes, thus safeguarding your "springboard" progress.

Common Pitfalls and How to Avoid Them

Even with the best intentions, it’s easy to stumble into common traps during the car loan process. Being aware of these pitfalls is key to a smooth and financially sound Springboard Car Loan experience.

Ignoring the Total Cost: More Than Just Monthly Payments

As emphasized earlier, focusing solely on the monthly payment is a major pitfall. It can lead to taking on a longer loan term, paying significantly more interest, and ultimately, a more expensive car than you can truly afford.

Beyond the Monthly Payment: Always calculate the total cost of the car, including the purchase price, interest, fees, and the estimated total cost of ownership (insurance, fuel, maintenance). A lower monthly payment often means a higher overall cost.

Not Shopping Around: Accepting the First Offer

This is one of the most common and costly mistakes. Many buyers accept the first loan offer they receive, whether from their bank or the dealership, without exploring other options.

Accepting the First Offer: Never do this. Always compare offers from at least three different lenders (banks, credit unions, online lenders) and use your pre-approval as leverage when negotiating with a dealership. Competition works in your favor.

Falling for Dealer Add-ons: Unnecessary Expenses

Dealerships often try to sell you additional products and services at the point of sale. While some might be beneficial, many are unnecessary and can significantly inflate the total cost of your loan.

Extended Warranties, GAP Insurance (When Not Needed):

- Extended Warranties: Carefully evaluate if an extended warranty is truly worth the cost. Often, a new car’s factory warranty is sufficient, and for used cars, independent warranties might be cheaper.

- GAP Insurance: Guaranteed Asset Protection (GAP) insurance covers the "gap" between what you owe on your car and its actual cash value if it’s totaled or stolen. It’s essential if you put down a small down payment or have a long loan term. However, if you have a significant down payment or your loan-to-value is good, you might not need it, or your existing auto insurer might offer it cheaper. Always ask for a breakdown of these costs and evaluate their necessity.

Misunderstanding Loan Terms: Hidden Traps

Signing a contract you don’t fully understand can lead to financial headaches down the road.

Hidden Fees, Variable Rates: Always ask for a complete breakdown of all fees associated with the loan. Be wary of variable rates if you prefer predictability in your payments. Don’t be afraid to ask questions until every clause in the agreement is clear to you. Your financial future depends on it.

For more consumer protection advice on car loans, visit the Consumer Financial Protection Bureau (CFPB) website, which offers valuable resources and guidance.

Conclusion: Drive Towards Financial Freedom

Embarking on the journey of securing a "Springboard Car Loan" is about more than just purchasing a vehicle; it’s about making a deliberate, informed decision that empowers your financial future. By understanding your credit, meticulously budgeting, making strategic down payments, and choosing the right vehicle and lender, you transform a simple transaction into a powerful tool for financial growth.

Remember, every on-time payment you make is a brick laid in the foundation of your creditworthiness. Whether you’re a first-time buyer building credit from scratch, or someone with past challenges aiming for a fresh start, a well-managed car loan can be the ultimate catalyst for positive change. It’s an opportunity to demonstrate financial responsibility, improve your credit score, and unlock better opportunities down the line.

Don’t let the complexities of auto financing deter you. With the comprehensive knowledge and expert tips provided in this guide, you are now