Your Ultimate Guide to BPI Car Loan: Drive Your Dream Car Home with Confidence

Your Ultimate Guide to BPI Car Loan: Drive Your Dream Car Home with Confidence Carloan.Guidemechanic.com

Owning a car in the Philippines is more than just a convenience; it’s often a necessity, a symbol of progress, and a key to greater personal and professional mobility. For many, the journey to car ownership begins with securing a reliable car loan. Among the myriad of financial institutions, the Bank of the Philippine Islands (BPI) stands out as a formidable and trusted partner, offering competitive BPI Car Loan options that empower countless Filipinos to turn their automotive dreams into reality.

This comprehensive guide is meticulously crafted to be your definitive resource for everything you need to know about BPI Car Loans. We’ll dive deep into the application process, demystify eligibility requirements, shed light on interest rates, and arm you with insider tips to ensure a smooth and successful car loan journey. Our ultimate goal is to provide you with a pillar of knowledge, equipping you with the confidence to navigate the path to your dream car with BPI.

Your Ultimate Guide to BPI Car Loan: Drive Your Dream Car Home with Confidence

Why Choose a BPI Car Loan for Your Next Vehicle?

When considering a car loan, the institution you choose plays a pivotal role in your overall experience. BPI, with its century-long legacy in the Philippine banking industry, offers a compelling proposition for aspiring car owners. Their reputation for stability, customer-centric services, and innovative financial products makes them a top choice for many.

One of the primary advantages of opting for a BPI Car Loan is their established trust and extensive network. You’re not just getting a loan; you’re partnering with a bank that understands the local market dynamics and consumer needs. This translates into a more secure and reliable borrowing experience compared to less established lenders. Based on my extensive experience in financial services, the peace of mind that comes with dealing with a reputable bank like BPI is invaluable.

Furthermore, BPI is known for its competitive interest rates and flexible payment terms. While rates can fluctuate based on market conditions and your credit profile, BPI consistently strives to offer options that are attractive to a wide range of borrowers. Their commitment to providing accessible financing solutions means they often have various loan products tailored to different financial capacities, ensuring there’s likely a BPI Auto Loan package that fits your budget.

Understanding the Types of BPI Car Loans Available

BPI recognizes that car buyers have diverse needs, whether they’re eyeing a brand-new vehicle or a reliable pre-owned one. To cater to these varying requirements, BPI typically offers distinct types of car loans. Knowing these distinctions is crucial for choosing the right product for your specific situation.

The most common type is the New Car Loan. This is designed for individuals purchasing a brand-new vehicle directly from a dealership. These loans often come with the most favorable terms, including potentially lower interest rates and longer payment periods, reflecting the lower risk associated with financing a brand-new asset. BPI works closely with numerous car dealerships, streamlining the process for new car buyers.

For those considering a more budget-friendly option, BPI also provides Used Car Loans or Pre-Owned Car Loans. These are tailored for financing second-hand vehicles, usually from accredited dealerships or sometimes even private sellers, provided the vehicle meets certain age and condition criteria. While the terms might differ slightly from new car loans, BPI ensures that financing for pre-owned vehicles remains accessible, allowing more Filipinos to enter car ownership without breaking the bank. It’s essential to verify the vehicle’s age limit for financing, as banks usually have a cut-off (e.g., not older than 5-7 years).

Eligibility Requirements for a BPI Car Loan: Are You Qualified?

Before you even begin gathering documents, understanding the eligibility criteria is paramount. Meeting these foundational requirements is the first critical step toward getting your BPI Car Loan approved. Banks set these standards to assess a borrower’s capacity to repay the loan, ensuring responsible lending practices.

Generally, to be eligible for a BPI Car Loan, applicants must meet the following criteria:

- Citizenship and Residency: You must be a Filipino citizen or a Philippine resident foreigner. This ensures that the bank operates within its regulatory framework and can easily verify your identity and legal standing.

- Age Requirements: Applicants typically need to be at least 21 years old but not more than 65 years old upon loan maturity. This age range reflects the bank’s assessment of a borrower’s income-earning years and financial stability.

- Stable Source of Income: This is perhaps the most crucial factor. BPI requires applicants to have a stable and verifiable source of income. For employed individuals, this means a regular salary from a reputable company. For self-employed individuals or professionals, it involves demonstrating consistent income through business operations or professional practice. The bank needs assurance that you have the financial capacity to meet your monthly amortizations.

- Minimum Gross Monthly Income: BPI, like other banks, sets a minimum gross monthly income requirement. This threshold varies depending on the loan amount and the bank’s internal policies, but it ensures that the loan payment won’t unduly burden your finances. Always inquire about the current minimum income during your initial consultation.

- Employment or Business Tenure: For employed individuals, a minimum of two years of continuous employment with their current company is often required. For self-employed individuals, the business should typically be operational and profitable for at least three years. This tenure signifies stability and reliability in your income stream.

Pro tips from us: Even if you meet the basic requirements, having a good credit history significantly boosts your chances of approval. Regularly checking your credit report and addressing any discrepancies can put you in a stronger position.

Essential Documents for Your BPI Car Loan Application

Gathering the correct and complete set of documents is a critical, often underestimated, part of the BPI Car Loan application process. Incomplete documentation is a common reason for delays or even rejection. Based on my experience, preparing these documents meticulously beforehand can significantly speed up your application.

Here’s a breakdown of the typical documents BPI will require, categorized for clarity:

1. Personal Documents:

- Completely Filled-Out Application Form: This is your initial declaration of intent and provides the bank with essential personal and financial information. Ensure all fields are accurately and legibly filled.

- Valid Government-Issued IDs: You will need at least two valid IDs, such as a passport, driver’s license, SSS ID, Pag-IBIG ID, or PRC ID. These are for identity verification and fraud prevention. Make sure they are not expired and signatures match.

- Proof of Billing: Documents like a utility bill (electricity, water, internet) under your name, or a barangay certificate, serve as proof of your residential address. This helps the bank confirm your declared address.

2. Income Documents:

- For Employed Individuals (Local & Overseas Filipino Workers – OFWs):

- Certificate of Employment with Compensation (COEC): This document from your employer verifies your position, tenure, and gross monthly income. It should be recent, usually within the last 30-60 days.

- Latest Income Tax Return (ITR) / BIR Form 2316: This provides an official record of your declared income to the government.

- Latest Payslips: Usually, the last three months’ payslips are required to show consistent income and deductions.

- Proof of Remittance (for OFWs): For OFWs, consistent remittances to a Philippine bank account or a verifiable contract can serve as proof of income.

- For Self-Employed Individuals / Professionals:

- Latest Income Tax Return (ITR) with Audited Financial Statements: This is crucial for verifying the profitability and stability of your business.

- Bank Statements: Usually, the last six months’ bank statements (personal and/or business) are needed to show cash flow and transaction history.

- DTI/SEC Registration: Proof of business registration with the Department of Trade and Industry (DTI) for sole proprietorships or Securities and Exchange Commission (SEC) for partnerships/corporations.

- Business Permit / Mayor’s Permit: An updated permit validating your business operations.

- Commission Vouchers / Professional Fee Statements: For professionals like doctors or lawyers, these validate your income from practice.

3. Collateral Documents (for the vehicle itself):

- Pro-forma Invoice / Sales Quotation: This is provided by the car dealership and details the vehicle’s price, specifications, and any included accessories.

- Duly Accomplished Chattel Mortgage Application Form: This is a security agreement for the loan, where the vehicle serves as collateral.

Common mistakes to avoid are submitting expired IDs, incomplete ITRs, or payslips that are too old. Always double-check each document against the bank’s checklist.

The BPI Car Loan Application Process: A Step-by-Step Guide

Navigating the car loan application process can seem daunting, but breaking it down into manageable steps makes it much clearer. BPI has streamlined its process to be as efficient as possible, provided you come prepared. Here’s a detailed walkthrough:

Step 1: Initial Inquiry and Consultation

Your journey typically begins with an inquiry, either online through the BPI website, by visiting a BPI branch, or directly through an accredited car dealership that partners with BPI. During this initial phase, you can discuss your needs, get an estimate of potential loan amounts, and understand the current interest rates and terms. This is also the perfect time to clarify any eligibility questions you might have.

Step 2: Submit Your Application Form and Documents

Once you’ve identified the car you want and understood the basic terms, you’ll need to complete the BPI Car Loan application form. This form, along with all the required documents we outlined earlier, must be submitted to BPI. You can often submit these through the dealership if they have a BPI desk, or directly at a BPI branch. Ensure everything is complete and accurate to prevent delays.

Step 3: Loan Evaluation and Credit Investigation

After submission, BPI’s credit officers will thoroughly review your application and documents. They will conduct a credit investigation, which includes checking your credit history with the Credit Information Corporation (CIC) and other financial institutions. They might also contact your employer or references to verify information. This stage is crucial as the bank assesses your creditworthiness and repayment capacity.

Step 4: Loan Approval or Further Requirements

If your application meets BPI’s criteria, you will receive a loan approval. This approval will detail the final loan amount, interest rate, payment terms, and any conditions. Sometimes, the bank might request additional documents or clarifications during the evaluation phase before making a final decision. Be responsive to these requests to keep your application moving forward.

Step 5: Sign Loan Documents and Release of Funds

Upon approval, you will be required to sign the loan agreement, promissory note, and chattel mortgage documents. Carefully read and understand all the terms and conditions before signing. Once these documents are executed and any down payment is settled with the dealership, BPI will release the loan proceeds directly to the car dealership.

Step 6: Vehicle Release and Start of Amortization

With the loan proceeds settled, the dealership can now release your brand-new or pre-owned car to you. Your monthly amortization payments will typically begin a month after the loan release date. It’s crucial to mark your payment due dates and ensure timely payments to maintain a good credit standing.

Navigating Interest Rates and Payment Terms

Understanding BPI Car Loan interest rates and payment terms is vital, as they directly impact the total cost of your car and your monthly budget. Don’t just focus on the headline interest rate; consider the entire financial package.

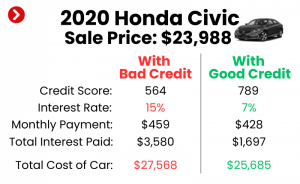

BPI typically offers fixed interest rates for the entire loan tenure. This means your interest rate will remain constant, providing predictable monthly payments. While variable rates exist in some markets, fixed rates are more common for car loans in the Philippines, offering stability for borrowers. Factors influencing your interest rate include prevailing market rates, your credit score, the loan tenure, and the type of vehicle being financed. A strong credit history and a larger down payment can often lead to more favorable rates.

Payment terms, or loan tenure, usually range from 12 months (1 year) to 60 months (5 years). Some special promotions might extend this, but five years is a common maximum for car loans. A longer payment term means lower monthly amortizations, but it also means you pay more in total interest over the life of the loan. Conversely, a shorter term leads to higher monthly payments but less overall interest paid.

Based on my experience, it’s always wise to strike a balance between affordability and minimizing total interest. Use a car loan calculator (you can find many online, or check out our guide on ) to compare different scenarios before committing.

Calculating Your BPI Car Loan: What to Expect Financially

Beyond the interest rate, several other financial components contribute to the total cost of your BPI Car Loan. Being aware of these helps you budget effectively and avoid surprises.

- Down Payment: This is the initial lump sum you pay to the dealership. BPI usually requires a minimum down payment, often ranging from 15% to 30% of the vehicle’s selling price. A larger down payment reduces your loan amount, which in turn lowers your monthly amortization and the total interest you’ll pay.

- Monthly Amortization: This is your regular, fixed payment to BPI, covering both a portion of the principal loan amount and the interest. This is the most significant recurring cost you’ll manage.

- Processing Fees: Banks charge a processing fee for handling your loan application. This is typically a one-time fee deducted from the loan proceeds or paid upfront.

- Documentary Stamp Tax (DST): A government tax levied on certain documents, including loan agreements. This is usually a small percentage of the loan amount.

- Chattel Mortgage Fee: This fee covers the registration of the chattel mortgage with the Land Transportation Office (LTO), making the vehicle the bank’s collateral until the loan is fully paid.

- Insurance Premiums: Comprehensive car insurance is mandatory for the entire loan duration. While you can often choose your preferred insurer, the premium will be factored into your annual cost. BPI may offer in-house insurance options or partner with various providers.

Pro tips from us: Always ask for a clear breakdown of all fees and charges during your application. Don’t hesitate to clarify anything you don’t understand. A transparent bank will readily provide this information.

Tips for a Smooth BPI Car Loan Application

A successful car loan application isn’t just about meeting the requirements; it’s also about strategic preparation. Here are some pro tips to increase your chances of a smooth and swift BPI Car Loan approval:

- Improve Your Credit Score: Before applying, check your credit report. A good credit score (by consistently paying bills on time, managing existing debts responsibly) signals reliability to the bank, potentially leading to faster approvals and better interest rates.

- Save for a Larger Down Payment: While BPI has minimum down payment requirements, putting down a larger sum reduces your loan amount and, consequently, your monthly payments and total interest. It also shows the bank your strong financial commitment.

- Organize Your Documents Meticulously: As emphasized earlier, having all required documents complete, valid, and organized beforehand can prevent delays. Create a checklist and tick off each item.

- Know Your Budget and Desired Car: Don’t apply for a loan for a car you can’t truly afford. Research car prices, insurance costs, and maintenance expenses. This shows the bank you’ve done your homework and are a responsible borrower.

- Be Transparent and Honest: Provide accurate information in your application. Any discrepancies or misrepresentations can lead to immediate rejection and can negatively impact your future banking relationships.

- Maintain a Good Relationship with BPI: If you’re an existing BPI client with a good banking history (savings, current accounts, other loans), this can sometimes work in your favor, as the bank already has a profile of your financial behavior.

- Consider a Co-Borrower (if applicable): If your income or credit history isn’t as strong as you’d like, adding a qualified co-borrower (like a spouse or immediate family member) can strengthen your application. Their income and credit history will be factored into the assessment.

Common Mistakes to Avoid When Applying for a BPI Car Loan

Even with the best intentions, applicants can sometimes make errors that hinder their BPI Car Loan approval. Being aware of these common pitfalls can help you steer clear of them.

- Over-borrowing: Applying for a loan amount that strains your financial capacity is a major red flag for banks. It’s tempting to go for the most expensive car, but it’s crucial to align your loan with your realistic budget. BPI assesses your Debt-to-Income (DTI) ratio, and if your proposed monthly amortization is too high relative to your income, your application might be rejected.

- Neglecting Hidden Fees: As discussed, beyond the principal and interest, there are processing fees, DST, chattel mortgage fees, and mandatory insurance. Not factoring these into your total cost can lead to unexpected financial strain. Always ask for a comprehensive breakdown.

- Not Comparing Options: While this guide focuses on BPI, it’s always wise to compare offers from different banks or financing institutions. While BPI is highly competitive, checking alternatives ensures you’re getting the best possible deal for your specific situation. This due diligence empowers you.

- Incomplete or Inaccurate Documentation: This is a persistent issue. Submitting an application with missing documents or providing incorrect information will inevitably lead to delays or outright rejection. Double-check everything before submission.

- Ignoring Your Credit History: Many applicants overlook the importance of their credit standing. A history of missed payments, defaults, or excessive debt can severely damage your credit score, making banks hesitant to approve new loans. Take steps to improve it before applying.

- Applying to Multiple Banks Simultaneously (without caution): While comparing is good, applying to too many banks at once in a short period can sometimes be viewed negatively. Each application generates a "hard inquiry" on your credit report, and too many hard inquiries can slightly lower your credit score temporarily, signaling potential desperation for credit.

What Happens After BPI Car Loan Approval?

Congratulations, your BPI Car Loan has been approved! This is an exciting milestone, but there are still a few final steps before you drive away in your new vehicle.

Once approved, BPI will send you a Letter of Advice or a formal approval notification. This document outlines the specifics of your approved loan, including the exact loan amount, interest rate, term, and monthly amortization. It’s crucial to review this carefully to ensure it matches your expectations.

The next step involves the signing of loan documents. You will typically visit a BPI branch or a designated signing location to execute the loan agreement, promissory note, and the chattel mortgage agreement. These are legally binding documents, so take your time to read and understand every clause before affixing your signature. Don’t hesitate to ask BPI representatives for clarifications on any terms you find unclear.

After the documents are signed and any required down payment is confirmed with the dealership, BPI will proceed with the release of funds. The loan amount will be directly disbursed to the car dealership. This usually happens electronically, ensuring a swift and secure transaction.

Finally, with the payment confirmed, the car dealership can then prepare your vehicle for release. This includes processing the necessary LTO registration, ensuring all accessories are installed, and conducting a final quality check. You’ll then be able to pick up your car and officially begin your journey as a car owner. Remember that your monthly amortization payments will commence approximately one month after the loan proceeds are released.

Managing Your BPI Car Loan Responsibly

Securing your BPI Car Loan is just the beginning. Responsible loan management is key to a stress-free ownership experience and maintaining a healthy financial standing.

The most important aspect of managing your BPI Car Loan is making timely payments. Set up reminders, consider enrolling in auto-debit arrangements from your BPI savings or current account, or ensure you pay via BPI online banking well before the due date. Missing payments can incur late payment charges and, more importantly, negatively impact your credit score, making it harder to secure future loans.

It’s also essential to understand your monthly statements. These statements provide a breakdown of your payments, showing how much goes towards the principal and how much towards interest. Regularly reviewing these helps you track your loan’s progress.

If your financial situation improves, you might consider early payment options. Some BPI Car Loans may allow for early settlement or lump-sum payments to reduce your outstanding principal. While this can save you a significant amount in interest over the long term, always inquire about any pre-termination fees or penalties that might apply. Weigh the pros and cons carefully.

BPI Car Loan vs. Other Financing Options: A Quick Look

While this guide focuses on BPI, it’s helpful to briefly understand how a BPI Car Loan stands in comparison to other financing avenues.

- In-house Dealership Financing: Many dealerships offer their own financing. While convenient, these often involve higher interest rates or less flexible terms compared to bank loans. Banks like BPI, being financial institutions, specialize in lending and typically offer more competitive packages.

- Other Banks: Other major banks in the Philippines also offer car loans. It’s prudent to compare their rates, terms, and processing times with BPI’s. However, BPI often stands out with its robust online infrastructure and widespread branch network, which can be a significant advantage.

- Personal Loans: While you could use a personal loan to buy a car, it’s generally not advisable. Personal loans usually have much higher interest rates and shorter terms than dedicated car loans because they are unsecured (no collateral). A BPI Car Loan is a secured loan, using the car as collateral, which allows for better terms.

For a secured and generally more affordable path to car ownership, a specialized car loan from a trusted bank like BPI is often the superior choice.

Frequently Asked Questions (FAQs) About BPI Car Loans

To further assist you, here are answers to some commonly asked questions regarding BPI Car Loans:

Q1: Can I apply for a BPI Car Loan online?

A: Yes, BPI offers an online application portal for convenience. You can typically fill out the application form and submit some initial documents digitally. However, you might still need to visit a branch or dealership for final document submission, verification, and signing.

Q2: How long does BPI Car Loan approval take?

A: The approval timeline can vary. If all documents are complete and there are no issues with your credit standing, approval can sometimes be as quick as 3-7 banking days. However, it can extend to 2 weeks or more if additional documents or verifications are required. Proactively submitting all necessary documents speeds up the process significantly.

Q3: What if I’m self-employed or an OFW? Are the requirements different?

A: Yes, the income document requirements are slightly different. For self-employed individuals, audited financial statements, DTI/SEC registration, and business permits are crucial. For OFWs, verifiable proof of remittances, overseas employment contracts, and valid work permits are essential. BPI has specific loan products and requirements tailored for these groups.

Q4: Can I choose my own car insurance provider for my BPI Car Loan?

A: Yes, generally you can choose your preferred insurance provider, provided it is accredited by BPI. Comprehensive car insurance is mandatory for the entire loan term, and the policy must include BPI as the loss payee.

Q5: What happens if I can’t pay my monthly amortization?

A: If you anticipate difficulty in making a payment, it’s crucial to contact BPI immediately. They may offer solutions like payment restructuring or grace periods, depending on your situation. Ignoring the issue can lead to late payment fees, a negative impact on your credit score, and ultimately, repossession of the vehicle.

Q6: Can I apply for a BPI Car Loan for a second-hand car?

A: Yes, BPI offers financing for pre-owned vehicles. However, there are usually age restrictions on the vehicle (e.g., not older than 5-7 years from the manufacturing date) and it must pass BPI’s inspection and valuation criteria.

Conclusion: Drive Your Dream Car with BPI

Securing a BPI Car Loan is a well-trodden path for many Filipinos aspiring to car ownership. With its reputation for reliability, competitive offerings, and a structured application process, BPI provides a robust solution for financing your dream vehicle. By understanding the eligibility criteria, meticulously preparing your documents, navigating the application steps, and managing your loan responsibly, you are well-equipped to make an informed decision.

This guide has aimed to be your ultimate companion, offering insights and practical advice gleaned from years of observing financial processes. Remember, the journey to car ownership should be exciting, not overwhelming. With the right preparation and BPI as your trusted partner, you’re not just getting a car loan; you’re opening the door to greater mobility, convenience, and the fulfillment of a significant personal goal. Take the first step today, and drive home with confidence!