Your Ultimate Guide to Canandaigua National Bank Car Loans: Drive Away with Confidence

Your Ultimate Guide to Canandaigua National Bank Car Loans: Drive Away with Confidence Carloan.Guidemechanic.com

Navigating the world of car financing can often feel like a complex journey, filled with jargon and countless options. For residents of the Finger Lakes region and Western New York, one local institution consistently stands out for its community focus and personalized service: Canandaigua National Bank (CNB). If you’re considering purchasing a new vehicle or refinancing an existing auto loan, understanding the ins and outs of a Canandaigua National Bank car loan is crucial.

This comprehensive guide will break down everything you need to know, from the types of loans available to the application process, key factors influencing approval, and invaluable tips to ensure a smooth, confident car buying experience. Our goal is to equip you with the knowledge to make an informed decision, securing the best possible financing solution for your automotive dreams.

Your Ultimate Guide to Canandaigua National Bank Car Loans: Drive Away with Confidence

Why Choose a Local Lender Like Canandaigua National Bank for Your Car Loan?

In an age dominated by large national banks and online-only lenders, the appeal of a local institution like Canandaigua National Bank remains strong, especially when it comes to significant purchases like a vehicle. Community banks offer a distinct advantage that often gets overlooked in the pursuit of the lowest interest rate. They are rooted in the very communities they serve.

Based on my experience in financial advising, local banks like CNB often provide a level of personalized service and understanding that larger entities simply cannot match. They understand the local economy, build long-term relationships with their customers, and can sometimes be more flexible in their lending decisions, especially for established community members. This local expertise can be a significant benefit when you’re looking for a Canandaigua National Bank car loan.

When you walk into a CNB branch, you’re not just a number; you’re a neighbor. This personal touch can translate into a smoother application process, clearer communication, and a lending partner who genuinely wants to see you succeed.

Exploring the Range of Canandaigua National Bank Car Loan Options

Canandaigua National Bank understands that not all car buying needs are the same. Whether you’re eyeing a brand-new model, a reliable used vehicle, or looking to improve the terms of an existing loan, CNB typically offers a variety of financing solutions designed to meet diverse customer requirements. Understanding these options is the first step toward securing the right Canandaigua National Bank car loan for you.

New Car Loans

For those who dream of driving a brand-new vehicle off the dealership lot, a new car loan from CNB provides the necessary financing. These loans are specifically tailored for vehicles that have never been previously titled and are typically purchased directly from an authorized dealership.

New car loans often come with attractive interest rates and flexible terms, reflecting the lower depreciation risk associated with brand-new vehicles. Lenders generally view new cars as lower risk due to their warranty coverage, pristine condition, and predictable value over the initial years. This often translates into more favorable loan conditions for the borrower.

Used Car Loans

Purchasing a used car is a popular and often more budget-friendly option for many consumers. Canandaigua National Bank offers competitive financing for used vehicles, allowing you to secure a reliable car without breaking the bank.

Used car loans typically have slightly higher interest rates compared to new car loans, primarily due to the increased depreciation and potential for unforeseen maintenance issues in pre-owned vehicles. However, CNB aims to make used car financing accessible and affordable, ensuring you can find a quality vehicle that fits your budget. It’s crucial to consider the vehicle’s age, mileage, and condition when applying for a used auto loan, as these factors can influence the loan terms offered.

Auto Loan Refinancing

Perhaps you already have a car loan but are looking for better terms. Auto loan refinancing is a smart strategy to potentially lower your interest rate, reduce your monthly payments, or even shorten your loan term. This involves taking out a new loan, often from a different lender like Canandaigua National Bank, to pay off your existing car loan.

Refinancing can be particularly beneficial if your credit score has improved since you first took out your original loan, or if interest rates have dropped. It’s also a valuable option if your financial situation has changed, allowing you to adjust your payment schedule to better suit your current budget. A Canandaigua National Bank car loan for refinancing could save you a significant amount over the life of your loan.

Other Vehicle Loans

Beyond traditional cars, CNB may also offer financing for other recreational vehicles. This could include motorcycles, RVs (recreational vehicles), boats, or even ATVs.

These specialized vehicle loans cater to different purposes and may have unique terms and conditions. If you’re looking to finance a non-standard vehicle, it’s always best to inquire directly with Canandaigua National Bank about their specific offerings and eligibility requirements. They often have dedicated loan officers who can guide you through the process for these distinct asset types.

The Canandaigua National Bank Car Loan Application Process: A Step-by-Step Guide

Applying for a car loan, whether it’s your first time or you’re a seasoned borrower, can seem daunting. However, breaking it down into manageable steps makes the process clear and straightforward. When seeking a Canandaigua National Bank car loan, you’ll find their approach to be customer-centric and transparent.

Step 1: Pre-Approval – Your Smart Starting Point

One of the best pieces of advice I can offer is to seek pre-approval before you start serious car shopping. Pre-approval means a lender, in this case, Canandaigua National Bank, reviews your financial information and tentatively agrees to lend you a certain amount at a specific interest rate.

Getting pre-approved gives you several powerful advantages. It sets a clear budget, allowing you to shop with confidence knowing exactly how much car you can afford. More importantly, it turns you into a cash buyer at the dealership, giving you stronger negotiation power on the vehicle’s price, as you won’t be reliant on their in-house financing. This separation of car price negotiation from financing negotiation is a pro tip from us that can save you thousands.

Step 2: Gathering Your Documentation

Once you decide to move forward, either with a pre-approval or a full application, you’ll need to provide certain documents. While the exact list can vary slightly, common requirements for a Canandaigua National Bank car loan typically include:

- Proof of Identity: A valid government-issued ID, such as a driver’s license or passport.

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2 forms, or tax returns if you’re self-employed. This helps CNB assess your ability to repay the loan.

- Proof of Residency: Utility bills, lease agreements, or mortgage statements to confirm your address.

- Vehicle Information (if applicable): For a specific car, you’ll need the VIN (Vehicle Identification Number), make, model, year, and mileage. For refinancing, you’ll need details of your existing loan.

- Down Payment Information: If you plan to make a down payment, details on the source of funds.

Having these documents ready beforehand will significantly speed up your application process.

Step 3: Submitting Your Application

You can typically apply for a Canandaigua National Bank car loan in several ways: online through their website, by visiting a local branch, or over the phone. Each method offers convenience, and choosing the one that best suits your comfort level is key.

When submitting, you’ll fill out a detailed application form, providing personal, financial, and employment information. This is where the bank gets a complete picture of your creditworthiness and financial health. Be thorough and accurate; any discrepancies could delay your approval.

Step 4: Credit Check and Loan Review

As part of the application process, Canandaigua National Bank will perform a credit check. This allows them to access your credit report and credit score, which are critical factors in determining your eligibility and the interest rate you’ll be offered.

A loan officer will then review your entire application, considering your income, debt, credit history, and the value of the vehicle you intend to purchase. They are looking for a clear indication that you can reliably make your monthly payments.

Step 5: Receiving a Decision and Closing the Loan

After the review, CNB will communicate their decision. If approved, you’ll receive a loan offer outlining the approved loan amount, interest rate, loan term, and monthly payment.

Carefully review all the terms and conditions. Don’t hesitate to ask your CNB loan officer any questions you may have. Once you’re comfortable and agree to the terms, you’ll sign the necessary paperwork, and the funds will be disbursed. Congratulations, you’re now the proud owner of your new or new-to-you vehicle, financed by a Canandaigua National Bank car loan!

Key Factors Influencing Your CNB Car Loan Approval & Terms

Securing a favorable Canandaigua National Bank car loan isn’t just about filling out a form; it’s about understanding the factors lenders prioritize. Several key elements play a significant role in determining whether your loan is approved and, crucially, the interest rate and terms you’ll receive. Being aware of these can help you better prepare and potentially improve your loan outcome.

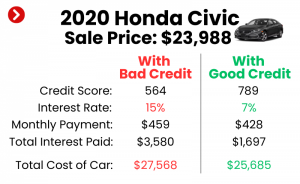

Your Credit Score: The Cornerstone of Lending

Your credit score is arguably the most influential factor in any loan application. It’s a numerical representation of your creditworthiness, based on your payment history, amounts owed, length of credit history, new credit, and credit mix. Lenders use it to predict the likelihood of you repaying your debt.

A higher credit score (typically 700+) indicates a lower risk to the lender, often resulting in lower interest rates and more flexible terms. Conversely, a lower score might lead to higher rates or even a denial. Pro tips from us: before applying, check your credit report for errors and work to improve your score if needed.

Debt-to-Income (DTI) Ratio

Your Debt-to-Income ratio is a crucial metric that shows how much of your gross monthly income goes towards debt payments. Lenders, including Canandaigua National Bank, want to ensure you have enough disposable income to comfortably afford your new car payment.

A generally accepted healthy DTI is below 36%, though some lenders might approve higher. To calculate it, divide your total monthly debt payments (including your prospective car payment, mortgage/rent, credit cards, student loans) by your gross monthly income. A lower DTI signifies less financial strain and a greater ability to manage additional debt.

Loan-to-Value (LTV) Ratio

The Loan-to-Value ratio compares the loan amount you’re requesting to the actual market value of the vehicle you intend to purchase. For instance, if a car is valued at $20,000 and you’re borrowing $18,000, your LTV is 90%.

Lenders prefer a lower LTV because it means you have more equity in the vehicle, reducing their risk if you default. A higher LTV, especially above 100% (often seen when rolling negative equity from a trade-in into a new loan), can make securing favorable terms more challenging.

Down Payment: Your Commitment Matters

Making a down payment on your car loan demonstrates your financial commitment and reduces the amount you need to borrow. This directly impacts your LTV ratio, making your loan more attractive to lenders.

A substantial down payment can lead to lower monthly payments, less interest paid over the life of the loan, and potentially a better interest rate. Common mistakes to avoid are underestimating the power of a down payment; even 10-20% can make a significant difference in your loan terms.

Loan Term: Balancing Monthly Payments and Total Cost

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A longer loan term generally results in lower monthly payments, which can be appealing for budget management.

However, a longer term also means you’ll pay more in total interest over the life of the loan. Conversely, a shorter term will have higher monthly payments but will save you money on interest and get you debt-free faster. Finding the right balance that suits your budget and financial goals is crucial when finalizing your Canandaigua National Bank car loan.

Understanding Interest Rates and Fees for Your CNB Auto Loan

When evaluating a Canandaigua National Bank car loan, understanding the interest rate and any associated fees is paramount. These components directly impact the total cost of your loan and your monthly payments. Don’t just look at the monthly payment; delve into the specifics to ensure you’re getting the best deal.

How Interest Rates are Determined

The interest rate is essentially the cost of borrowing money. For a car loan, it’s expressed as a percentage of the principal balance. Several factors influence the interest rate you’ll be offered by CNB:

- Your Credit Score: As discussed, a higher score typically leads to lower rates.

- Loan Term: Shorter terms often have slightly lower rates because the lender’s risk is spread over a shorter period.

- Loan-to-Value (LTV): A lower LTV (larger down payment) can result in a better rate.

- Current Market Conditions: Overall economic conditions and the prime interest rate set by the Federal Reserve influence all lending rates.

- Vehicle Type: New cars generally carry lower rates than used cars due to their predictable depreciation and reliability.

- Relationship with the Bank: As a community bank, CNB might offer slightly more favorable rates to long-standing customers with multiple accounts.

APR vs. Interest Rate: Know the Difference

It’s vital to distinguish between the stated interest rate and the Annual Percentage Rate (APR). The interest rate is simply the cost of borrowing the principal amount. The APR, however, represents the true annual cost of your loan, including the interest rate plus any additional fees charged by the lender.

For example, if a loan has a 5% interest rate but includes an origination fee, the APR might be 5.2%. Always compare APRs when shopping for loans, as it gives you the most accurate picture of the total cost of credit. This allows for a true apples-to-apples comparison between different offers.

Potential Fees Associated with a Car Loan

While Canandaigua National Bank strives for transparency, it’s always wise to inquire about any potential fees that might be part of your Canandaigua National Bank car loan. Common fees, though not all may apply to your specific loan, can include:

- Origination Fee: A charge for processing the loan application.

- Documentation Fee (Doc Fee): A fee for preparing and processing loan documents.

- Late Payment Fee: Incurred if you miss a payment deadline.

- Prepayment Penalty: Though less common with car loans, some lenders might charge a fee if you pay off your loan early. Always check for this.

- Title and Registration Fees: While not directly a bank fee, these are often rolled into the total cost of vehicle financing.

Always ask for a detailed breakdown of all costs and fees before signing any loan agreement. A reputable lender like CNB will be transparent about these charges.

Benefits of Choosing Canandaigua National Bank for Your Auto Loan

Opting for a Canandaigua National Bank car loan comes with a host of advantages, particularly for those who value local expertise and personalized service. While competitive rates are always a draw, the holistic experience of banking with a community institution often provides added value.

Local, Personalized Service

One of the most significant benefits is the access to local, personalized service. Unlike large national banks where you might be just another customer in a vast system, CNB offers a more intimate banking experience. You can walk into a local branch, speak directly with a loan officer who knows the area, and build a relationship with your financial institution. This personal touch can make the application process feel less intimidating and more collaborative.

Community Commitment

Canandaigua National Bank is deeply embedded in the Finger Lakes region. Choosing them for your car loan means you’re supporting a local business that reinvests in your community. This commitment often translates into a deeper understanding of local financial needs and a desire to foster the economic well-being of its customers.

Potentially Competitive Rates for Local Customers

While national lenders might advertise seemingly unbeatable rates, community banks like CNB often offer highly competitive rates, especially for their established customers. They might be more willing to work with local residents to find a rate that fits their budget, leveraging existing banking relationships.

Relationship Banking

If you already bank with CNB for your checking, savings, or other financial products, applying for a car loan there can be seamless. They already have a profile of your financial history, which can streamline the approval process. Furthermore, maintaining multiple accounts with one institution can sometimes unlock additional benefits or preferred rates.

Convenient Local Branches and Digital Access

CNB offers the best of both worlds: the convenience of local branches for in-person consultations and the accessibility of online banking and applications. This hybrid approach ensures you can manage your loan and finances how and when it suits you best, combining traditional service with modern efficiency.

Making the Best Decision: What to Compare

Securing a Canandaigua National Bank car loan is a significant financial decision, and like any major purchase, it pays to do your homework. While CNB offers many benefits, it’s always wise to compare their offer with other lenders to ensure you’re getting the best possible terms for your individual situation.

Shop Around – Don’t Settle for the First Offer

This is a critical piece of advice from experienced financial advisors: always shop around. Don’t feel pressured to take the first loan offer you receive, whether it’s from a dealership or a bank. Contact multiple lenders – other local credit unions, national banks, and online lenders – to get a range of quotes.

When comparing, focus on the APR (Annual Percentage Rate) rather than just the interest rate, as the APR includes all fees and gives you the true cost of borrowing. Also, compare loan terms, prepayment penalties (if any), and late payment fees. Most credit scoring models allow for a "rate shopping window," meaning multiple inquiries for the same type of loan within a short period (typically 14-45 days) will only count as one hard inquiry, minimizing the impact on your score.

Focus on the Total Cost of the Loan, Not Just Monthly Payments

While a low monthly payment might seem attractive, it can sometimes hide a longer loan term and a higher total amount of interest paid over time. Always calculate the total cost of the loan by multiplying your monthly payment by the number of months in the loan term, then adding any upfront fees.

A Canandaigua National Bank car loan officer can help you understand this total cost. A shorter loan term with slightly higher monthly payments might save you thousands in interest over the life of the loan. Balance your monthly budget with your long-term financial goals.

Read the Fine Print

Before signing any loan agreement, meticulously read all the terms and conditions. Pay close attention to clauses regarding:

- Prepayment Penalties: Can you pay off the loan early without extra charges?

- Late Payment Policies: What are the fees and grace periods for missed payments?

- Default Clauses: What constitutes a default, and what are the consequences?

- Insurance Requirements: Are there specific insurance requirements for the vehicle?

Common mistakes to avoid are signing without fully understanding every detail. If anything is unclear, ask for clarification. A reputable lender like CNB will be happy to explain everything. You can also consult trusted external sources like the Consumer Financial Protection Bureau (CFPB) for general guidance on auto loans.

Pro Tips for a Smooth CNB Car Loan Experience

To ensure your journey to securing a Canandaigua National Bank car loan is as smooth and stress-free as possible, here are some pro tips from our experience in the automotive financing world. These insights can help you navigate the process efficiently and confidently.

1. Get Pre-Approved

As mentioned earlier, pre-approval is your superpower. It gives you a clear budget, strengthens your negotiating position at the dealership, and separates the car-buying decision from the financing decision. A pre-approval from Canandaigua National Bank means you know exactly what you can afford before you even step onto a car lot.

2. Know Your Budget Inside and Out

Beyond the loan payment, remember to factor in other car ownership costs. This includes insurance, fuel, maintenance, registration, and potential repairs. A car is an ongoing expense, and understanding the full financial picture will prevent future stress. Don’t just budget for the monthly car loan payment; budget for the car.

3. Understand Your Credit Score and Report

Before applying, obtain your free credit report from all three major bureaus (Equifax, Experian, TransUnion) and check your credit score. This allows you to identify any errors that could negatively impact your application and gives you an idea of the rates you might qualify for. If your score needs improvement, address it before applying.

4. Negotiate the Car Price Separately

Armed with your CNB pre-approval, you can focus on negotiating the best possible price for the vehicle itself. Treat your pre-approval as cash. This strategy prevents dealerships from inflating the car price while giving you a "good" financing deal. Negotiate the car price first, then present your pre-approval.

5. Ask Plenty of Questions

Never be afraid to ask questions. Whether it’s about interest rates, loan terms, fees, or the application process, a knowledgeable loan officer at Canandaigua National Bank is there to help. Understanding every aspect of your loan agreement is your right and responsibility. There are no "dumb questions" when it comes to your finances.

Conclusion: Drive Forward with a Canandaigua National Bank Car Loan

Navigating the path to car ownership or refinancing can be an exciting yet challenging endeavor. By understanding the nuances of a Canandaigua National Bank car loan, you’re empowering yourself with the knowledge to make an informed and confident decision. CNB, with its strong local presence and commitment to personalized service, offers a compelling option for residents seeking reliable auto financing in the Finger Lakes region.

From understanding the different types of loans available, preparing for the application process, to recognizing the factors that influence your terms, this guide has aimed to provide a comprehensive overview. Remember to leverage the power of pre-approval, compare offers diligently, and always read the fine print.

With these insights, you’re well-equipped to secure a Canandaigua National Bank car loan that aligns with your financial goals, putting you in the driver’s seat of your next vehicle with peace of mind. Visit your local Canandaigua National Bank branch or explore their online resources today to take the next step towards your automotive future.