Your Ultimate Guide to Capital One For Car Loans: Drive Smart, Finance Smarter

Your Ultimate Guide to Capital One For Car Loans: Drive Smart, Finance Smarter Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used vehicle is an exciting prospect. However, for many, the financing aspect can often feel overwhelming, even daunting. This is where a reliable and transparent lender becomes invaluable. Capital One has established itself as a significant player in the automotive financing landscape, offering a range of solutions designed to simplify the car buying process.

But what exactly makes Capital One a strong contender for your car loan needs? Is it truly the right fit for your specific situation? In this comprehensive guide, we’ll dive deep into everything you need to know about securing a car loan with Capital One. From understanding their unique pre-qualification process to navigating the dealership, we’ll equip you with the knowledge to drive smart and finance even smarter.

Your Ultimate Guide to Capital One For Car Loans: Drive Smart, Finance Smarter

Why Consider Capital One for Your Car Loan? Unpacking the Advantages

When you’re shopping for a car loan, you’ll encounter a multitude of lenders, each with their own set of offerings. Capital One stands out for several compelling reasons that cater to a broad spectrum of car buyers. Understanding these advantages can help you determine if they align with your financial goals and car purchasing strategy.

1. The Power of Pre-Qualification with Auto Navigator:

One of Capital One’s most celebrated features is its Auto Navigator tool. This innovative platform allows you to pre-qualify for a car loan without impacting your credit score. Based on my experience, this initial step is a game-changer, providing a clear picture of your potential loan terms before you even set foot in a dealership.

The Auto Navigator offers personalized loan terms, including estimated interest rates and monthly payments, tailored to your credit profile. This transparency empowers you to shop for cars with confidence, knowing exactly what you can afford.

2. A Vast Network of Participating Dealerships:

Capital One boasts a substantial network of thousands of participating dealerships across the United States. This extensive reach means that once you’re pre-qualified, you have a wide array of options when it comes to selecting a vehicle and finalizing your purchase. You’re not limited to a handful of dealers; instead, you have the flexibility to choose from a diverse inventory.

This broad network simplifies the car buying process, as many dealerships are already set up to work directly with Capital One. It streamlines the paperwork and ensures a smoother transaction from start to finish.

3. Financing Options for Diverse Credit Tiers:

Capital One understands that not everyone has a perfect credit score. They are known for offering financing solutions to individuals with various credit histories, ranging from excellent to fair and even some challenging credit situations. This inclusive approach makes them an accessible option for a wider audience.

While specific terms will always depend on your individual credit profile, their willingness to work with different credit scores provides crucial opportunities for many aspiring car owners. It means a past financial misstep doesn’t necessarily close the door on your dream car.

4. Transparency and Clarity in Loan Terms:

One of the biggest anxieties in car financing is hidden fees or confusing terms. Capital One aims to provide a straightforward and transparent lending experience. Their pre-qualification process, in particular, offers a clear breakdown of potential rates and payments, allowing you to budget effectively.

Based on my professional observations, this upfront clarity helps buyers make informed decisions, minimizing surprises later on. They strive to make the complex world of auto financing more understandable for the average consumer.

Demystifying Capital One’s Auto Navigator: Your Path to Pre-Qualification

The Capital One Auto Navigator is more than just a tool; it’s a strategic advantage in the car buying process. Understanding how it works can significantly enhance your experience and put you in a stronger negotiating position.

What is Auto Navigator and How Does It Work?

Auto Navigator is an online platform that allows you to get pre-qualified for an auto loan from Capital One. You input some basic financial information, and in minutes, it provides you with personalized loan offers. This isn’t a full loan approval, but rather an offer of terms you could qualify for.

The beauty of this system lies in its ability to show you real-time rates and payment estimates on specific vehicles from participating dealerships. You can browse cars within your approved budget and see how different terms affect your monthly payment.

The "Soft Inquiry" Advantage:

Crucially, using Auto Navigator for pre-qualification only involves a "soft inquiry" on your credit report. A soft inquiry does not negatively impact your credit score. This is a significant benefit, as it allows you to explore your financing options without the worry of multiple hard inquiries dinging your credit.

It means you can shop for financing with peace of mind, knowing your credit score remains intact until you decide to move forward with a full application. This empowers you to truly compare offers without commitment.

Steps to Using Auto Navigator:

- Visit the Capital One Auto Navigator Website: Start by navigating to their dedicated online platform.

- Provide Basic Information: You’ll be asked for details such as your desired loan amount, income, housing costs, and Social Security Number. This information helps them assess your financial standing.

- Receive Personalized Offers: Almost instantly, Capital One will present you with estimated loan terms, including interest rates and monthly payments.

- Shop for Your Car: With your pre-qualification in hand, you can then browse vehicles from participating dealerships directly through the Auto Navigator portal, seeing how your specific terms apply to each car.

- Print Your Offer: Once you find a car you like, you can print your pre-qualification offer to take with you to the dealership.

Pro tip from us: Even if you have a specific car in mind, use the Auto Navigator to explore various options. It helps solidify your budget and gives you leverage during negotiations.

The Application Process: From Pre-Qualification to Driving Away

Understanding the full application process, especially after utilizing Auto Navigator, is key to a smooth car buying experience. It bridges the gap between estimated terms and a finalized loan.

Pre-Qualification vs. Full Application:

It’s vital to differentiate between pre-qualification and a full loan application. Pre-qualification is an estimate, a conditional offer based on a soft credit pull. A full application, which happens at the dealership, involves a "hard inquiry" on your credit report.

This hard inquiry is a formal request for your credit history and may temporarily lower your credit score by a few points. However, multiple hard inquiries for auto loans within a short period (typically 14-45 days, depending on the credit bureau) are usually treated as a single inquiry, so don’t be afraid to compare offers.

Required Documents for a Capital One Car Loan:

When you visit the dealership to finalize your Capital One car loan, be prepared to provide several documents. While the exact list can vary slightly, common requirements include:

- Proof of Identity: Government-issued photo ID (driver’s license, state ID).

- Proof of Income: Recent pay stubs, tax returns, or bank statements.

- Proof of Residency: Utility bill, lease agreement, or mortgage statement.

- Social Security Number: For credit verification.

- Vehicle Information: Details of the car you intend to purchase (VIN, make, model, year, mileage).

- Down Payment: If applicable, proof of funds for your down payment.

Having these documents ready will significantly speed up the approval process at the dealership.

Navigating the Dealership with Capital One Pre-Qualification:

When you arrive at a participating dealership with your Capital One pre-qualification, inform the sales associate that you’re pre-qualified with Capital One Auto Navigator. They are typically familiar with the process. You can then show them your offer.

The dealership will work with Capital One to verify your information and finalize the loan. This often involves submitting a full application and reviewing the precise terms and conditions. While your pre-qualification provides a strong estimate, the final offer might vary slightly based on the specific vehicle and additional dealer fees.

Who Can Get a Capital One Car Loan? Eligibility and Credit Considerations

Capital One aims to be inclusive, but like all lenders, they have specific eligibility criteria. Understanding these requirements will help you assess your likelihood of approval.

Credit Score Considerations:

Capital One is known for working with a broad range of credit scores.

- Excellent Credit (720+): If you have excellent credit, you’re likely to receive the most competitive interest rates and favorable terms. Your financial history demonstrates a low risk to lenders.

- Good Credit (660-719): With good credit, you’re still in a strong position to secure attractive rates. Capital One often offers solid options for this tier.

- Fair/Average Credit (600-659): This is where Capital One truly shines for many. While rates may be higher than for those with excellent credit, they are often a viable option when other prime lenders might decline.

- Challenged Credit (Below 600): While approval is not guaranteed and rates will be significantly higher, Capital One may offer options for individuals with past credit challenges. They assess your overall financial picture, not just one score.

Based on my experience, having a stable income and a reasonable debt-to-income ratio can significantly bolster your application, even with a lower credit score.

Income Requirements:

While Capital One doesn’t publish a specific minimum income requirement, they will assess your ability to repay the loan. They look for a stable source of income that demonstrates you can comfortably afford the monthly payments, considering your existing debts. Generally, a higher, more stable income strengthens your application.

Age and Residency:

Applicants must be at least 18 years old (or the age of majority in their state) and a legal resident of the United States. These are standard requirements across most financial institutions.

Types of Car Loans Offered by Capital One

Capital One provides financing solutions for various car buying scenarios, catering to different needs and preferences.

1. New Car Loans:

If you’re eyeing a brand-new vehicle straight from the manufacturer, Capital One offers competitive financing for new cars. These loans typically come with lower interest rates compared to used car loans, as new vehicles are considered less risky due to their pristine condition and warranty coverage.

2. Used Car Loans:

For those looking for a pre-owned vehicle, Capital One also provides used car loans. The terms for used car loans can vary based on the age, mileage, and condition of the vehicle. Generally, interest rates might be slightly higher than new car loans, reflecting the increased risk associated with an older vehicle.

3. Refinancing Car Loans:

Did you secure a car loan with less-than-ideal terms in the past? Capital One offers refinancing options. Refinancing involves taking out a new loan to pay off your existing car loan, often with a lower interest rate, a different loan term, or a reduced monthly payment.

Pro tips from us: Refinancing can be a smart move if your credit score has improved since you first bought your car, or if interest rates have dropped. It can save you a significant amount over the life of the loan.

Factors Affecting Your Capital One Car Loan Rate

Understanding what influences your interest rate is crucial for securing the best possible terms. Several key factors come into play when Capital One determines your loan offer.

1. Your Credit Score:

This is arguably the most significant factor. A higher credit score signals lower risk to lenders, translating into lower interest rates. Conversely, a lower score will typically result in a higher rate. It’s a direct reflection of your borrowing history.

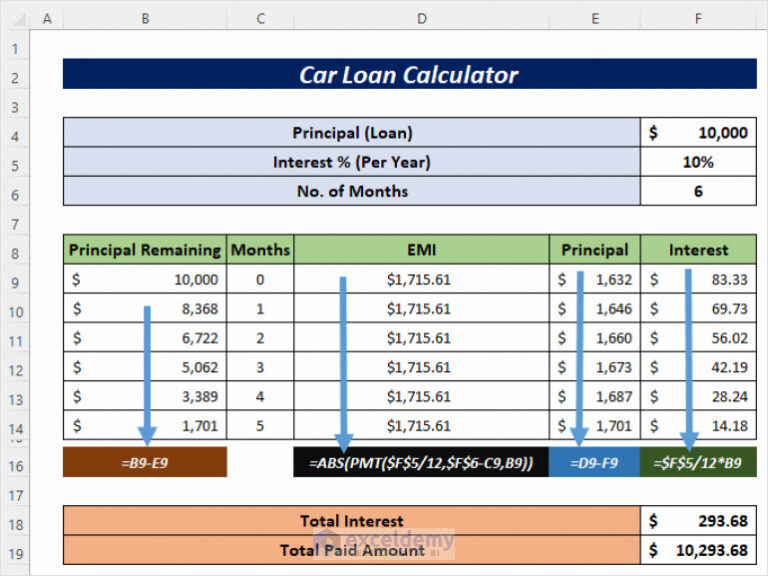

2. Loan Term (Length of the Loan):

The length of your loan, often expressed in months (e.g., 36, 48, 60, 72 months), directly impacts your interest rate. Shorter loan terms usually come with lower interest rates but higher monthly payments. Longer terms mean lower monthly payments but often result in a higher overall interest paid and a slightly higher interest rate.

3. Down Payment Amount:

Making a substantial down payment reduces the amount you need to borrow, which can lower your interest rate. A larger down payment also signals financial responsibility and reduces the lender’s risk, as you have more equity in the vehicle from the start.

4. Vehicle Age and Mileage:

For used cars, the age and mileage of the vehicle play a role. Newer, lower-mileage used cars are often seen as less risky and may qualify for better rates than older, high-mileage vehicles. This is because older cars tend to depreciate faster and may incur more maintenance issues.

5. Debt-to-Income (DTI) Ratio:

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders use this to assess your ability to take on additional debt. A lower DTI ratio indicates you have more disposable income to cover your car loan payments, making you a more attractive borrower.

Pro Tips for Securing the Best Capital One Car Loan

Navigating the car loan landscape can be tricky, but with these expert tips, you can maximize your chances of getting the most favorable terms from Capital One.

1. Actively Improve Your Credit Score:

Before you even think about applying for a loan, take steps to boost your credit score. Pay down existing debts, make all payments on time, and avoid opening new credit lines. A higher score translates directly to better interest rates. For more detailed advice, check out our article on How to Improve Your Credit Score for a Car Loan.

2. Save for a Significant Down Payment:

Aim for at least a 10-20% down payment, if possible. Not only does this reduce your loan amount, but it also signals financial stability to lenders. It can significantly impact your interest rate and monthly payments.

3. Don’t Just Accept the First Offer:

Even with Capital One pre-qualification, compare offers. While the Auto Navigator gives you excellent terms, it’s wise to ensure you’re getting the best deal. Always review the final terms presented at the dealership carefully.

4. Understand the Total Cost, Not Just Monthly Payments:

A common mistake is to focus solely on the monthly payment. Always consider the total amount you’ll pay over the life of the loan, including interest. A lower monthly payment over a longer term can often mean paying much more overall.

5. Negotiate Smartly at the Dealership:

Your Capital One pre-qualification gives you leverage. Negotiate the car price separately from the financing. With your pre-qualified rate in hand, you can confidently discuss the vehicle’s price, knowing your financing is already largely secured.

Common Mistakes to Avoid When Getting a Capital One Car Loan

Even with the convenience of Capital One, certain missteps can lead to less-than-ideal outcomes. Based on my observations, here are common pitfalls to steer clear of.

1. Not Utilizing Pre-Qualification:

Failing to use the Auto Navigator for pre-qualification means you’re walking into a dealership blind. You lose out on knowing your potential rates and budgeting accurately, putting you at a disadvantage during negotiations. Always pre-qualify first.

2. Focusing Only on the Monthly Payment:

While an affordable monthly payment is important, obsessing over it can lead you to accept longer loan terms with higher overall interest. Always ask about the total cost of the loan and understand the interest rate.

3. Ignoring the Total Cost of Ownership:

Beyond the loan, consider insurance, maintenance, and fuel costs for the vehicle you’re considering. A car might seem affordable on paper, but its running costs could stretch your budget thin.

4. Skipping the Fine Print:

Always read your loan agreement thoroughly before signing. Understand all terms, conditions, fees, and penalties. If something is unclear, ask questions until you’re completely satisfied.

5. Buying More Car Than You Can Afford:

Just because you’re approved for a certain amount doesn’t mean you should spend it all. Stick to a budget that comfortably fits your financial situation, leaving room for unexpected expenses. Overspending on a car is a common regret.

Beyond the Loan: Managing Your Capital One Auto Loan

Once you’ve driven off the lot, your relationship with Capital One for your car loan doesn’t end. Effective management of your loan ensures a smooth repayment period.

Payment Options:

Capital One offers various convenient ways to make your monthly car loan payments:

- Online: Through your Capital One account on their website or mobile app.

- AutoPay: Set up automatic deductions from your bank account to ensure on-time payments. This is a pro tip for avoiding late fees and improving your credit history.

- Mail: Send a check or money order.

- Phone: Make a payment over the phone.

Customer Service:

Should you have any questions or encounter issues with your loan, Capital One provides customer service support. You can typically reach them via phone or through secure messaging within your online account.

Early Payoff Considerations:

Capital One auto loans generally do not have prepayment penalties. This means you can pay off your loan early without incurring extra fees, potentially saving you a significant amount in interest over the life of the loan. This is an excellent strategy if your financial situation improves. For more details on this, you might find our article on The Ultimate Guide to Car Loan Refinancing helpful.

Conclusion: Driving Towards a Smarter Car Purchase with Capital One

Securing a car loan doesn’t have to be a complex and intimidating ordeal. Capital One offers a robust and user-friendly platform that empowers consumers to approach car financing with confidence and clarity. Through its innovative Auto Navigator, wide dealership network, and commitment to transparency, Capital One has positioned itself as a strong choice for diverse car buyers.

By leveraging their pre-qualification process, understanding the factors that influence your rates, and avoiding common mistakes, you can significantly enhance your car buying journey. Remember, smart financing is just as important as choosing the right vehicle. With Capital One, you have a valuable partner to help you drive smart and finance even smarter.

Ready to take the first step towards your next vehicle? Explore your options with Capital One Auto Navigator today and unlock the door to your dream car. You can visit their official Auto Navigator page here: Capital One Auto Navigator.