Your Ultimate Guide to Car Loans: Drive Away with Confidence and Smart Financial Choices

Your Ultimate Guide to Car Loans: Drive Away with Confidence and Smart Financial Choices Carloan.Guidemechanic.com

The open road, the scent of a new car, the feeling of independence – owning a vehicle is a dream for many. Yet, for most, that dream requires a significant financial step: securing a car loan. Navigating the world of auto financing can feel like a complex journey in itself, filled with jargon, interest rates, and approval processes. But it doesn’t have to be daunting.

As an expert in personal finance and a seasoned observer of the auto industry, I’ve seen firsthand how a well-understood car loan can pave the way to vehicle ownership, while a misunderstood one can lead to unnecessary stress and expense. This comprehensive guide is designed to demystify car loans, providing you with the knowledge and confidence to make informed decisions. We’ll explore everything from understanding the basics to securing the best rates and managing your loan effectively. Get ready to transform your car buying experience from confusing to clear.

Your Ultimate Guide to Car Loans: Drive Away with Confidence and Smart Financial Choices

What Exactly is a Car Loan? Unpacking the Basics of Vehicle Financing

At its core, a car loan, also known as an auto loan, is a sum of money borrowed from a financial institution or lender to purchase a vehicle. This borrowed money is then repaid over a predetermined period, typically with added interest. It’s essentially a secured loan, meaning the car itself acts as collateral. Should you fail to make your payments, the lender has the right to repossess the vehicle.

Understanding the fundamental components of a car loan is crucial. The principal is the actual amount of money you borrow to buy the car. The interest is the cost of borrowing that money, expressed as a percentage. Finally, the loan term refers to the length of time you have to repay the loan, usually measured in months (e.g., 36, 48, 60, or 72 months). Each monthly payment you make consists of a portion of the principal and a portion of the interest.

Based on my experience, many people focus solely on the monthly payment without truly grasping how the interest rate and loan term dramatically impact the total cost of the vehicle. A lower monthly payment might seem appealing, but if it’s spread over a longer term, you could end up paying significantly more in interest over the life of the loan. Always look at the big picture.

Exploring the Diverse World of Car Loan Options

Not all car loans are created equal. The type of loan you pursue will often depend on the vehicle you’re buying, your financial situation, and where you choose to borrow. Knowing these distinctions can help you find the most suitable financing solution.

New Car Loans

These loans are specifically for brand-new vehicles purchased from a dealership. They often come with the lowest interest rates due to the car’s higher value and the assumption that a new car has fewer immediate mechanical issues. Lenders see less risk in financing a new vehicle.

Used Car Loans

When you buy a pre-owned vehicle, you’ll apply for a used car loan. While still secured by the vehicle, these typically have slightly higher interest rates than new car loans. This is because used cars can have unpredictable maintenance needs and depreciate faster, representing a slightly higher risk for lenders. The age and mileage of the used car can also influence the interest rate you’re offered.

Refinancing Car Loans

Refinancing involves replacing your existing car loan with a new one, often with different terms. People typically refinance to secure a lower interest rate, reduce their monthly payments, or change the loan term. This can be a smart move if your credit score has improved since you first took out the loan, or if interest rates have dropped.

Private Party Car Loans

Buying a car directly from an individual rather than a dealership is known as a private party sale. Financing these purchases can be a bit trickier, as traditional auto lenders are sometimes hesitant to finance vehicles without a dealership’s inspection and warranty. However, some banks and credit unions do offer specific private party auto loans, though the rates might be slightly higher.

Dealership Financing vs. Bank/Credit Union Loans

When you’re at the dealership, they’ll often offer to arrange financing for you. This is known as dealership financing. While convenient, it’s crucial to understand that dealerships often act as intermediaries, working with a network of lenders. They might mark up the interest rate to earn a commission.

Pro tips from us: Always shop around for your car loan before stepping onto the dealership lot. Get pre-approved by your bank or a credit union. This gives you a benchmark interest rate and empowers you to negotiate with the dealership from a position of strength, treating your financing as a cash offer. You can then compare the dealership’s offer against your pre-approval to ensure you’re getting the best deal.

Decoding Car Loan Interest Rates: What You Need to Know

The interest rate is arguably the most critical factor influencing the total cost of your car loan. A seemingly small difference in percentage points can translate into hundreds, even thousands, of dollars over the loan term. Understanding what drives these rates is paramount.

Factors Influencing Your Interest Rate

Several key elements determine the interest rate you’ll be offered:

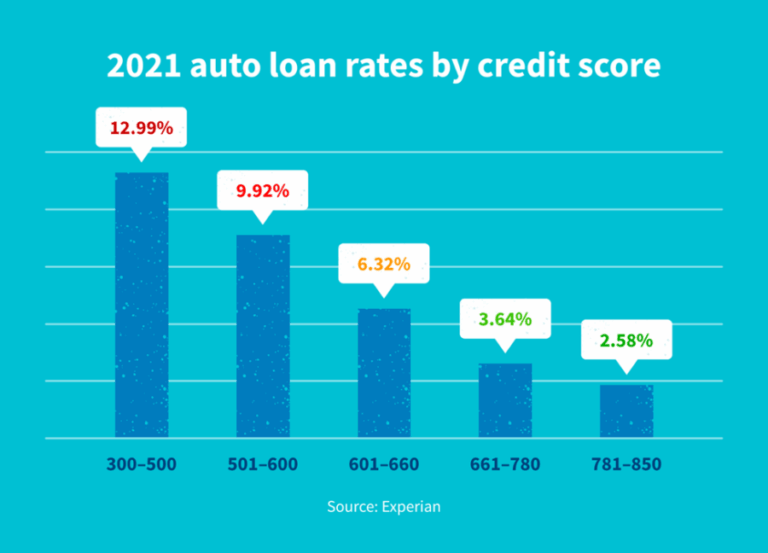

- Your Credit Score: This is perhaps the most significant factor. Lenders use your credit score to assess your creditworthiness and the likelihood of you repaying the loan. A higher score (generally 700+) indicates lower risk and typically qualifies you for the best rates.

- Loan Term: Shorter loan terms usually come with lower interest rates because the lender’s money is tied up for less time, reducing their risk. Conversely, longer terms often have higher rates.

- Down Payment Amount: A larger down payment reduces the amount you need to borrow, lowering the lender’s risk. This can often translate into a more favorable interest rate.

- Vehicle Type and Age: As mentioned, new cars generally command lower rates than used cars. Certain luxury or high-performance vehicles might also have different rate structures.

- Economic Conditions: Broader economic factors, such as the prime rate set by central banks, influence all lending rates, including auto loans. When the economy is strong and rates are low, car loans can be more affordable.

Fixed vs. Variable Rates

Most car loans come with a fixed interest rate, meaning the rate remains the same throughout the entire loan term. This provides predictability, as your monthly payment for principal and interest will not change.

Variable interest rates are less common for car loans. With these, the rate can fluctuate over time based on a specific market index. While they might start lower, they carry the risk of increasing, leading to higher monthly payments. For the stability and predictability it offers, a fixed-rate loan is almost always the preferred choice for car financing.

The Annual Percentage Rate (APR)

When comparing loan offers, always look at the Annual Percentage Rate (APR). The APR is a broader measure of the cost of borrowing money, reflecting not just the interest rate but also other fees and charges associated with the loan (like origination fees, though less common with auto loans). It provides a more accurate picture of the total annual cost of your loan. A lower APR means a cheaper loan overall.

Common mistakes to avoid are focusing solely on the monthly payment or just the quoted interest rate. Always ask for the APR to get a complete picture of the loan’s true cost. Comparing APRs across different lenders is the most effective way to find the best deal.

The Car Loan Application Process: A Step-by-Step Guide to Approval

Securing a car loan doesn’t have to be a mystery. By following a structured approach, you can navigate the application process smoothly and increase your chances of approval on favorable terms.

Step 1: Assess Your Budget and Affordability

Before you even think about looking at cars, determine how much you can truly afford to spend each month, not just on the car payment, but on the total cost of ownership. This includes insurance, fuel, maintenance, and potential repairs. A general rule of thumb is that your total car expenses shouldn’t exceed 10-15% of your net income.

Based on my experience, rushing this step is a common pitfall. Many people fall in love with a car that’s beyond their means, only to face financial strain later. Be realistic about your financial situation.

Step 2: Check and Improve Your Credit Score

Your credit score is your financial report card. Obtain a copy of your credit report from one of the three major credit bureaus (Experian, Equifax, TransUnion) and check for any errors. If your score is lower than you’d like, take steps to improve it, such as paying down existing debts or making all payments on time. A few points increase can significantly impact the interest rate you’re offered. provides in-depth strategies for boosting your creditworthiness.

Step 3: Get Pre-Approval from Multiple Lenders

This is a powerful step. Seek pre-approval from banks, credit unions, and online lenders before you visit a dealership. Pre-approval involves a soft credit inquiry (which doesn’t impact your score) and gives you an idea of the loan amount and interest rate you qualify for. This turns you into a "cash buyer" at the dealership, giving you leverage in negotiations.

Step 4: Gather Necessary Documents

Once you’re ready to apply, lenders will require specific documents. These typically include:

- Proof of identity (driver’s license)

- Proof of residence (utility bill)

- Proof of income (pay stubs, tax returns, bank statements)

- Social Security number

- Vehicle information (if you’ve chosen a car)

Having these ready streamlines the application process.

Step 5: Compare Loan Offers Thoroughly

Never accept the first loan offer you receive. Use your pre-approvals to compare interest rates (APR), loan terms, and any associated fees from various lenders. A small difference in APR can save you hundreds, even thousands, over the life of the loan. Don’t be afraid to use one offer to negotiate with another lender.

Step 6: Read the Fine Print

Before signing anything, meticulously review the loan agreement. Understand every clause, especially regarding prepayment penalties (less common now, but still exist), late payment fees, and what happens if you miss a payment. Ensure the interest rate and term match what you were promised.

Step 7: Finalize the Loan and Drive Away!

Once you’re satisfied with all the terms, sign the paperwork. The funds will be disbursed, and you’ll officially own your new vehicle. You’ll then receive your payment schedule and instructions on how to make your monthly installments. Congratulations, you’ve successfully navigated the car loan process!

Key Factors That Influence Your Car Loan Approval

Lenders assess several critical factors when deciding whether to approve your car loan application and what terms to offer. Understanding these can help you strengthen your position.

- Credit Score and History: As highlighted, this is paramount. Lenders look for a history of responsible borrowing and timely payments. A strong credit score signals reliability.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments (including the proposed car payment) to your gross monthly income. Lenders prefer a lower DTI, typically below 40%, indicating you have enough disposable income to handle the new payment.

- Employment History and Income Stability: A consistent work history and stable income demonstrate your ability to make regular payments. Lenders want to see that you have a reliable source of funds.

- Down Payment Amount: A substantial down payment reduces the loan amount, thereby lowering the lender’s risk. It shows your commitment and reduces the chances of owing more than the car is worth (being "upside down").

- Vehicle Age and Type: Lenders often view newer, lower-mileage vehicles as less risky due to their higher resale value and lower likelihood of immediate repair costs. Older vehicles, especially those with high mileage, can be harder to finance or come with higher rates.

- Loan Term: Shorter loan terms are generally viewed more favorably by lenders, as their money is exposed for a shorter period. While longer terms can lower monthly payments, they increase the total interest paid and the risk for the lender.

Pro tips from us: If any of these factors are weak, consider addressing them before applying. For instance, increasing your down payment or paying down other debts can significantly improve your approval odds and loan terms.

Navigating Car Loans with Less-Than-Perfect Credit

Having a low credit score doesn’t automatically close the door on car ownership. While it might present more challenges and potentially higher costs, securing a car loan with bad credit is absolutely possible. It simply requires a more strategic approach.

One common strategy is to save for a larger down payment. A significant down payment reduces the loan amount and the lender’s risk, making you a more attractive borrower despite your credit history. This upfront investment can often offset a lower credit score.

Another viable option is to consider a co-signer. A co-signer, typically someone with excellent credit, agrees to be equally responsible for the loan. Their strong credit profile can help you get approved and potentially secure a better interest rate. However, remember that if you miss payments, it impacts their credit too.

You might also look for a shorter loan term, if financially feasible. While this means higher monthly payments, it can sometimes result in a lower interest rate, as the lender’s risk is reduced. Additionally, focusing on improving your credit score before you apply can pay dividends. Even a few months of diligent bill payment can make a difference.

Common mistakes to avoid are falling prey to predatory lenders who promise "guaranteed approval" but offer exorbitant interest rates and unfavorable terms. Always compare offers, read every detail, and if possible, bring a trusted advisor with you. Credit unions are often more willing to work with members who have challenged credit histories than traditional banks. Remember, securing a bad credit car loan and making consistent, on-time payments can actually be a great way to rebuild your credit over time.

Smart Strategies for Managing Your Car Loan Effectively

Once you’ve secured your car loan, the journey isn’t over. Effective loan management can save you money, improve your financial health, and ensure a smooth path to ownership.

- Make Extra Payments When Possible: Even small additional payments can significantly reduce the total interest paid and shorten your loan term. Direct these extra funds towards the principal amount. Check your loan agreement for any prepayment penalties, though they are rare on auto loans.

- Consider Refinancing: If your credit score has improved, interest rates have dropped, or your financial situation has changed, explore refinancing options. A lower interest rate or a more favorable term could save you a substantial amount of money over the remaining life of the loan. Use online calculators to see if refinancing makes financial sense for you.

- Set Up Automatic Payments: Automating your monthly payments ensures you never miss a due date. This not only prevents late fees but also helps maintain a positive payment history, which is crucial for your credit score.

- Build an Emergency Fund: Life is unpredictable. Having an emergency fund specifically for unexpected car repairs or a temporary loss of income can prevent you from missing loan payments, protecting your credit and your vehicle.

- Know Your Payoff Date: Keep track of your loan’s progress. Knowing your payoff date helps you visualize the end of your financial obligation and can motivate you to make extra payments to reach that goal sooner.

Pro tips from us: Regularly review your monthly budget to identify opportunities for extra payments. Even an extra $25 or $50 each month can make a big difference in the long run. For a deeper dive into financial planning, explore resources like the for more tips on managing your vehicle financing responsibly.

Conclusion: Driving Towards Financial Freedom with Your Car Loan

Securing a car loan is a significant financial commitment, but armed with the right knowledge, it doesn’t have to be intimidating. From understanding the nuances of interest rates and loan terms to navigating the application process and managing your debt wisely, every step you take contributes to a more confident and financially sound vehicle ownership experience.

Remember, the goal isn’t just to get approved for a loan; it’s to secure the best possible terms that align with your budget and financial goals. By doing your homework, comparing offers, and managing your loan proactively, you can minimize costs, build your credit, and ultimately drive away with peace of mind. Your journey to car ownership should be exciting, not stressful. With this guide, you’re now equipped to make smart decisions and embark on that open road with confidence.