Your Ultimate Guide to Car Loans San Diego: Navigating Auto Financing with Confidence

Your Ultimate Guide to Car Loans San Diego: Navigating Auto Financing with Confidence Carloan.Guidemechanic.com

San Diego, with its stunning coastline, vibrant culture, and sprawling neighborhoods, often requires a reliable vehicle to fully experience all it offers. Whether you’re commuting to La Jolla, exploring Balboa Park, or heading out to the backcountry, a car is more than just transportation—it’s a gateway to the San Diego lifestyle. However, securing the right auto financing can feel like navigating the Pacific without a compass.

This comprehensive guide is designed to demystify Car Loans San Diego, providing you with the expert knowledge and practical strategies needed to secure the best possible deal. We’ll delve deep into every aspect of auto financing, from understanding different loan types to mastering the application process, ensuring you drive away with confidence.

Your Ultimate Guide to Car Loans San Diego: Navigating Auto Financing with Confidence

Understanding the San Diego Auto Loan Landscape

San Diego’s unique blend of urban living and outdoor adventure means diverse transportation needs. For many, public transit options are limited, making a personal vehicle a necessity rather than a luxury. This high demand for cars naturally fuels a competitive market for auto financing San Diego.

Navigating this market successfully means being prepared. It’s not just about finding a car you love; it’s about finding a financing solution that fits your budget and financial goals. A well-structured car loan can be an excellent financial tool, while a poorly chosen one can become a significant burden.

Why San Diego Car Buying is Unique

The San Diego car market has its own rhythm. Dealerships compete fiercely, and credit unions have a strong presence, often offering attractive rates. The sheer volume of cars bought and sold daily means there are numerous options for both vehicles and financing. However, this also means it’s crucial to stand out as a well-informed buyer.

Based on my experience, many San Diegans rush into financing without understanding the nuances. This often leads to higher interest rates or unfavorable loan terms. Taking the time to educate yourself before stepping foot on a dealership lot or applying online will give you a significant advantage.

Types of Car Loans Available in San Diego

Before you start comparing rates, it’s essential to understand the different kinds of San Diego car loans available. Each type serves a specific purpose and comes with its own set of considerations. Knowing which one aligns with your needs is the first step toward smart financing.

New Car Loans San Diego

When you purchase a brand-new vehicle, you’ll typically seek a new car loan. These loans usually come with lower interest rates compared to used car loans because new cars are considered less of a risk to lenders. They hold their value better initially and often come with manufacturer warranties.

Lenders see new cars as more secure collateral. This often translates into more favorable terms for borrowers with good credit. However, depreciation is a significant factor with new cars, so ensure your loan term doesn’t outlast the car’s most valuable years.

Used Car Loans San Diego

Used car loans are incredibly popular in San Diego, offering a more budget-friendly entry into vehicle ownership. While interest rates might be slightly higher than new car loans due to perceived higher risk and age of the vehicle, they are still very accessible. The key here is the car’s condition and mileage.

Lenders evaluate used cars carefully. They consider the vehicle’s age, mileage, and condition, as these factors directly impact its resale value and thus the collateral for the loan. A well-maintained, relatively new used car will generally qualify for better rates than an older, high-mileage vehicle. Always get a pre-purchase inspection!

Refinancing Car Loans San Diego

Have you already secured a car loan but now feel the terms aren’t ideal? Refinance car loan San Diego options allow you to replace your existing car loan with a new one, often with a lower interest rate, a shorter or longer term, or different monthly payments. This can be a smart move if your credit score has improved since you first took out the loan, or if interest rates have dropped.

Pro tips from us: Refinancing can significantly reduce your total interest paid over the life of the loan. It can also free up cash flow if you extend the term, though this will likely mean paying more interest overall. Always calculate the total cost savings before committing to a refinance.

Leasing vs. Buying: A Quick Look

While not strictly a loan, leasing is another popular way to acquire a vehicle in San Diego. When you lease, you’re essentially paying for the right to use a car for a set period, usually 2-4 years, rather than owning it. This often results in lower monthly payments compared to buying.

Buying, on the other hand, means you own the car outright once the loan is paid off. You build equity and have no mileage restrictions. The choice between leasing and buying depends on your lifestyle, financial goals, and how long you typically keep a car. Consider the long-term implications for your finances carefully.

Where to Get a Car Loan in San Diego

When searching for Car Loans San Diego, you have several avenues to explore. Each option has distinct advantages and disadvantages, and comparing them is crucial for securing the best deal. Don’t limit yourself to the first offer you receive.

Dealership Financing

Most car dealerships in San Diego offer financing directly through their finance departments. They act as intermediaries, working with various banks, credit unions, and captive lenders (financing arms of car manufacturers like Toyota Financial Services or Honda Financial Services). This can be incredibly convenient, as you can handle the car purchase and financing all in one place.

The convenience, however, doesn’t always translate to the best rates. While dealerships might offer promotional APRs on new cars, it’s common for them to mark up interest rates to earn a profit. Common mistakes to avoid are signing without comparing outside offers. Always come prepared with a pre-approval from another lender.

Banks and Credit Unions

Traditional banks and local credit unions are excellent sources for auto financing San Diego. They often offer competitive interest rates, especially to their existing customers. Credit unions, in particular, are known for having some of the lowest rates because they are member-owned non-profits.

Building a relationship with a local institution like Mission Federal Credit Union or San Diego County Credit Union can yield significant benefits. They often prioritize their members and may be more flexible with loan terms. Pro tips from us: Check with your current bank or credit union first; you might already be pre-approved for a favorable rate.

Online Lenders

The digital age has brought forth a plethora of online lenders specializing in auto loans. Companies like Capital One Auto Finance, LightStream, and others offer a streamlined application process, often with quick approval decisions. These platforms allow you to compare multiple offers from various lenders without leaving your home.

Online lenders are particularly useful for comparison shopping. You can easily apply to several lenders within minutes, getting a range of offers to weigh against each other and against dealership financing. This empowers you to walk into a dealership with a solid understanding of what a competitive rate looks like.

Key Factors Affecting Your Car Loan in San Diego

Several critical elements influence the terms and interest rate of your San Diego car loan. Understanding these factors will help you prepare and position yourself for the most favorable financing possible. Knowledge truly is power in this scenario.

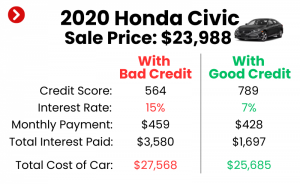

Credit Score

Your credit score is arguably the most crucial factor lenders consider. It’s a numerical representation of your creditworthiness, reflecting your payment history, debt levels, and credit utilization. A higher credit score (generally above 670 for FICO) signals less risk to lenders, leading to lower interest rates and better loan terms.

Based on my experience, improving your credit score even by a few points can save you hundreds, if not thousands, of dollars over the life of a car loan. If your score isn’t where you want it, consider taking steps to improve it before applying for a loan. For more details on this, you might find our article "Tips for Improving Your Credit Score for a Car Loan" helpful.

Down Payment

The amount of money you put down upfront significantly impacts your loan. A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the loan term. It also reduces the risk for the lender.

Common mistakes to avoid are putting little to no money down, especially on a new car. A substantial down payment helps offset immediate depreciation, reducing the chances of becoming "upside down" on your loan (owing more than the car is worth). Aim for at least 10-20% if possible.

Loan Term (Duration)

The loan term, or duration, is the length of time you have to repay the loan. Common terms range from 36 to 84 months. A shorter loan term means higher monthly payments but less total interest paid. Conversely, a longer term results in lower monthly payments but significantly more interest over time.

While a longer term might seem appealing due to lower monthly payments, it’s important to consider the total cost. Pro tips from us: Always calculate the total interest paid for different loan terms. Sometimes, paying a little more each month on a shorter term can save you a substantial amount in the long run.

Interest Rate (APR)

The Annual Percentage Rate (APR) is the true cost of borrowing money. It includes the interest rate plus any additional fees charged by the lender. A lower APR means less money spent on interest over the life of the loan. This is where comparison shopping for car loan rates San Diego becomes vital.

Your credit score, the loan term, the down payment, and the specific lender all influence your APR. Even a percentage point difference in APR can translate to hundreds or thousands of dollars saved, making it the most important number to negotiate and compare.

Debt-to-Income Ratio (DTI)

Lenders also look at your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates that you have more disposable income available to comfortably make your car loan payments, making you a less risky borrower.

Typically, lenders prefer a DTI ratio of 43% or lower. If your DTI is high, consider paying down other debts or increasing your income before applying for a car loan to improve your chances of approval and better terms.

Vehicle Age and Mileage

Especially for used car loans San Diego, the age and mileage of the vehicle play a crucial role. Older cars with high mileage are seen as higher risk by lenders because they are more prone to mechanical issues and have lower resale values. This can lead to higher interest rates or shorter loan terms.

Some lenders might even have restrictions on the maximum age or mileage they’ll finance. Be aware that an older vehicle might also incur higher maintenance costs, which should be factored into your overall budget.

Applying for a Car Loan in San Diego: A Step-by-Step Guide

Securing a Car Loans San Diego doesn’t have to be a daunting task. By following a structured approach, you can streamline the process, reduce stress, and significantly increase your chances of getting approved for the best possible terms.

Step 1: Check Your Credit Score and Report

Before you even think about looking at cars, pull your credit report from all three major bureaus (Experian, Equifax, and TransUnion) and check your credit score. You can get free annual reports from AnnualCreditReport.com. Review them carefully for any inaccuracies or errors.

Based on my experience, errors on credit reports are surprisingly common and can negatively impact your score. Disputing and correcting these errors before applying for a loan can potentially boost your score and save you money on interest.

Step 2: Determine Your Budget

Don’t just think about the monthly car payment. Consider the total cost of car ownership, which includes insurance, fuel, maintenance, and potential repairs. San Diego has relatively high gas prices and insurance rates, so factor these into your budget.

Pro tips from us: Use an online calculator to estimate your total monthly car expenses. This holistic approach ensures you can comfortably afford your vehicle without financial strain. You might also find our article "Understanding Car Insurance in California" helpful in budgeting for this aspect.

Step 3: Get Pre-Approved

One of the most powerful steps you can take is to get pre-approved for a loan before you visit any dealerships. Pre-approval means a lender has reviewed your financial information and tentatively agreed to lend you a specific amount at a certain interest rate. This gives you concrete buying power.

With a pre-approval in hand, you walk into the dealership as a cash buyer. You can focus on negotiating the car’s price, knowing your financing is already secured. This takes the pressure off discussing financing with the dealer and gives you a strong negotiating position.

Step 4: Shop for Your Car

Now that your financing is in order, you can confidently shop for your desired vehicle. Stick to your budget and the pre-approved loan amount. Test drive several cars and thoroughly inspect any used vehicles you’re considering.

Remember, the goal is to find the right car at the right price, not just the right loan. Since you’re pre-approved, you won’t feel pressured to accept the dealership’s financing offer if it’s not as competitive.

Step 5: Finalize the Loan

Once you’ve chosen your car and negotiated the purchase price, it’s time to finalize your loan. Compare your pre-approved offer with any financing options the dealership presents. Choose the one with the most favorable terms and the lowest APR.

Common mistakes to avoid are rushing through the paperwork. Read every single document carefully before signing. Understand all the terms, fees, and conditions. Don’t hesitate to ask questions if anything is unclear.

Special Considerations for Car Loans in San Diego

The diverse population and economic landscape of San Diego mean that not everyone fits neatly into a standard loan profile. Here are some specific situations and how to approach them effectively.

Bad Credit Car Loans San Diego

Having a less-than-perfect credit score doesn’t mean you can’t get a car loan in San Diego. It simply means you might need to adjust your expectations and strategies. Bad credit car loans San Diego are available, but they typically come with higher interest rates to compensate lenders for the increased risk.

Strategies for approval include making a larger down payment, finding a co-signer with good credit, or looking into subprime lenders who specialize in loans for individuals with lower credit scores. While the rates will be higher, making timely payments on a subprime loan can be an excellent way to rebuild your credit over time.

First-Time Car Buyer Loans

For those just starting their credit journey, securing a first-time car buyer loan can be a challenge. Lenders prefer to see a history of responsible borrowing. However, many dealerships and credit unions in San Diego offer programs specifically designed for first-time buyers.

These programs might require a larger down payment or a co-signer, but they provide an opportunity to establish credit. Pro tips from us: Focus on affordable, reliable vehicles and commit to making every payment on time. This builds a strong credit history for future financial endeavors.

Military Car Loans San Diego

Given San Diego’s significant military presence, many lenders and dealerships offer special programs and benefits for service members. These military car loans San Diego often feature lower interest rates, flexible terms, and sometimes even reduced fees as a token of appreciation for their service.

If you are an active duty, veteran, or retired service member, always inquire about military discounts and specialized loan programs. Organizations like USAA and Navy Federal Credit Union are excellent resources, known for their competitive rates and understanding of military unique financial situations.

Pro Tips for Securing the Best Car Loan in San Diego

Navigating the world of auto financing requires a keen eye and a strategic approach. Here are some insider tips to help you get the most favorable Car Loans San Diego.

- Negotiate Everything, Not Just the Car Price: Remember, the interest rate, loan term, and any additional fees are all negotiable. Don’t assume the first offer is the final one.

- Don’t Focus Solely on the Monthly Payment: While an attractive monthly payment might seem good, it could be masking a long loan term or a high interest rate, leading to more money paid overall. Always look at the total cost of the loan.

- Read All Documents Carefully: This cannot be stressed enough. Never sign anything you haven’t fully read and understood. If you have questions, ask them until you are satisfied with the answers.

- Consider GAP Insurance: Guaranteed Asset Protection (GAP) insurance can be a wise investment, especially for new cars. If your car is totaled or stolen and you owe more than its actual cash value, GAP insurance covers the difference, preventing you from being upside down on your loan.

- Shop Around for Insurance Quotes: Before finalizing your car purchase, get insurance quotes for the specific vehicle you’re considering. Insurance costs can vary wildly and significantly impact your overall monthly expenses.

- Pro tip from us: Always get multiple loan quotes. Just like you wouldn’t buy the first car you see, don’t settle for the first loan offer. Comparing 3-5 different lenders can reveal significant savings.

Common Mistakes to Avoid When Getting a Car Loan in San Diego

Even with all the information available, borrowers still make common errors that can cost them dearly. Being aware of these pitfalls can help you steer clear of them.

- Not Checking Your Credit Score: Going into the process blind leaves you vulnerable. You won’t know if the rate offered is fair or if there are errors affecting your eligibility.

- Skipping Pre-Approval: Without pre-approval, you lose significant negotiation power at the dealership. You’re also more likely to accept whatever financing the dealer offers, which might not be the best deal.

- Focusing Only on Monthly Payments: This is a classic trap. Dealers can stretch out loan terms to make payments seem affordable, but you end up paying much more in interest over time.

- Ignoring the Total Cost: Beyond the monthly payment, factor in interest, fees, insurance, and maintenance. A "cheap" car with a high loan rate or expensive insurance isn’t truly cheap.

- Impulse Buying: Rushing into a car purchase without proper research or financial planning often leads to buyer’s remorse and unfavorable loan terms. Take your time.

- Not Reading the Fine Print: Buried clauses or unexpected fees can quickly turn a good deal into a bad one. Always scrutinize loan agreements before signing.

Conclusion

Securing the right Car Loans San Diego is a significant step toward enjoying everything this beautiful city has to offer. By understanding the types of loans available, knowing where to look for financing, and familiarizing yourself with the factors that influence your loan terms, you empower yourself to make informed decisions.

Remember, preparation is key. Check your credit, set a realistic budget, and get pre-approved before you ever step foot on a dealership lot. By avoiding common mistakes and utilizing our expert tips, you can navigate the auto financing landscape with confidence and drive away with a deal that truly benefits you. Start your journey today and experience the joy of the open road in America’s Finest City!