Your Ultimate Guide to Easy To Get Car Loans: Drive Away with Confidence

Your Ultimate Guide to Easy To Get Car Loans: Drive Away with Confidence Carloan.Guidemechanic.com

Buying a car is a significant milestone for many, offering freedom, convenience, and a boost to daily life. However, the path to vehicle ownership often involves navigating the complex world of car loans. For many, the idea of securing "easy to get car loans" feels like a distant dream, especially if credit isn’t perfect or the process seems overwhelming.

As an expert blogger and professional SEO content writer, I understand the questions and anxieties that arise when seeking car financing. Based on my experience in the automotive and financial sectors, finding an easy car loan isn’t about magic; it’s about understanding the process, preparing thoroughly, and knowing where to look. This comprehensive guide is designed to demystify car loans, providing you with actionable insights and strategies to make your car financing journey as smooth and straightforward as possible.

Your Ultimate Guide to Easy To Get Car Loans: Drive Away with Confidence

We’ll dive deep into what truly constitutes an "easy" car loan, explore the factors lenders prioritize, and equip you with the knowledge to approach lenders with confidence. Our ultimate goal is to empower you to drive away in the car you need, with a financing plan that fits your life.

What Does "Easy To Get Car Loans" Really Mean? Dispelling the Myths

When people search for "easy to get car loans," they often envision a process with minimal paperwork, instant approval, and no hurdles, regardless of their financial history. While some lenders aim for efficiency, the term "easy" is relative in the world of finance. It doesn’t mean a free pass; it means a simplified, accessible process with a higher likelihood of approval for a wider range of applicants.

An easy car loan typically implies a few key characteristics. It suggests lenders are more flexible with their criteria, or that the applicant has taken steps to become an attractive borrower. It’s about reducing barriers, not eliminating responsible lending practices.

From our perspective, an easy car loan is one where you feel informed, prepared, and confident throughout the application. It’s about securing financing without undue stress or unexpected complications. We’ll show you how to achieve that.

Key Factors Lenders Consider for Car Loan Approval

Understanding what lenders look for is the first step toward making your car loan application "easier." Every financial institution assesses risk, and your application is a snapshot of your ability to repay. By addressing these factors proactively, you significantly boost your chances of approval.

Your Credit Score: The Foundation of Trust

Your credit score is arguably the most critical factor. It’s a numerical representation of your creditworthiness, reflecting your payment history, outstanding debts, and credit utilization. A higher score indicates a lower risk to lenders.

Lenders use this score to quickly gauge your reliability. While high scores open doors to the best rates, lower scores don’t necessarily mean outright denial. It often means different loan terms or specific types of lenders.

For those seeking easy car loans, understanding and, if necessary, improving your credit score is paramount. This can involve simple steps like paying bills on time or correcting errors on your credit report.

Income and Employment Stability: Can You Afford It?

Lenders need assurance that you have a steady income stream to cover your monthly car payments. They look for consistent employment history, typically for at least six months to a year at the same job. This demonstrates financial stability.

Your income level also plays a role in determining how much you can borrow. Lenders want to see that your car payment won’t consume too large a portion of your monthly earnings, leaving you unable to meet other financial obligations. Stable employment signals reliability.

Debt-to-Income Ratio (DTI): A Clear Financial Picture

Your debt-to-income (DTI) ratio is a crucial metric. It compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income available to manage new debt, like a car loan.

Lenders prefer a DTI ratio below 40% for new loans, though this can vary. A high DTI suggests you might be overextended, making a new car loan a higher risk. Pro tips from us: reducing other debts before applying can dramatically improve your DTI.

Down Payment: Showing Your Commitment

Making a substantial down payment signals several positive things to lenders. Firstly, it reduces the amount you need to borrow, thereby lowering the lender’s risk. Secondly, it demonstrates your financial commitment to the purchase.

A larger down payment often translates to lower monthly payments and potentially better interest rates. For those with less-than-perfect credit, a significant down payment can be a game-changer, making an "easy car loan" much more attainable. Even 10-20% can make a difference.

Vehicle Type and Age: The Asset’s Value

The type and age of the car you wish to purchase also influence loan approval. Newer, more reliable vehicles often qualify for better loan terms because they hold their value longer and are less likely to incur expensive repairs that could hinder your ability to pay.

Older vehicles or those with high mileage might be harder to finance or come with higher interest rates. This is because their resale value depreciates faster, and they present a higher risk of mechanical failure. Lenders consider the car as collateral.

Strategies to Make Your Car Loan Application "Easier"

While some factors are beyond immediate control, many proactive steps can significantly ease your car loan journey. These strategies are designed to present you as the most attractive borrower possible, increasing your chances of approval and securing favorable terms.

1. Check Your Credit Report and Improve It

Before applying for any loan, obtain a free copy of your credit report from all three major bureaus (Experian, Equifax, TransUnion). Review it meticulously for errors or discrepancies. Disputing and correcting these can instantly boost your score.

Beyond corrections, focus on habits that improve credit. Pay all bills on time, keep credit card balances low, and avoid opening new credit accounts right before applying for a car loan. Even small improvements can make a big difference. This diligence is key to easy car loan access.

2. Save for a Down Payment

As discussed, a down payment is a powerful tool. Start saving as early as possible. Even a modest down payment of 5-10% can make your application stronger, especially if your credit score isn’t stellar.

A larger down payment reduces your loan-to-value (LTV) ratio, which is attractive to lenders. It also means you’ll pay less interest over the life of the loan. This is a common-sense approach that makes the loan feel much easier.

3. Get Pre-Approved Before You Shop

One of the best pro tips from us is to get pre-approved for a car loan. This involves applying for financing with a bank, credit union, or online lender before you even set foot in a dealership. Pre-approval gives you a clear understanding of:

- The maximum amount you can borrow.

- Your estimated interest rate.

- The terms of the loan.

Armed with this information, you become a cash buyer at the dealership, giving you significant leverage in negotiations. It also eliminates the stress of financing at the last minute.

4. Know Your Budget and Stick to It

Before you start car shopping, determine how much you can realistically afford each month for a car payment, insurance, fuel, and maintenance. Don’t just focus on the loan amount. Overstretching your budget is a common mistake.

Having a clear budget in mind prevents you from falling in love with a car you can’t truly afford. This financial discipline makes the entire process easier and more responsible.

5. Consider a Co-Signer (With Caution)

If you have poor credit or limited credit history, a co-signer with good credit can significantly improve your chances of approval. A co-signer essentially guarantees the loan, promising to make payments if you default.

While this can make a loan much "easier to get," it’s a serious commitment for the co-signer. Their credit will be affected if you miss payments. Ensure both parties fully understand the responsibilities involved before taking this step.

6. Explore Different Lender Types

Don’t limit yourself to just dealership financing. Explore various lender types:

- Banks: Often offer competitive rates for well-qualified borrowers.

- Credit Unions: Known for personalized service and often lower rates, especially for members.

- Online Lenders: Provide quick applications and approvals, often catering to a wider range of credit scores.

- Dealership Financing: Convenient, but compare their offers with your pre-approval.

Shopping around for the best loan terms is crucial. Each lender has different criteria, and finding the right fit can make all the difference in securing an easy car loan.

Navigating "Easy Car Loans" with Less-Than-Perfect Credit

Even if your credit score isn’t ideal, securing a car loan is still possible. Many lenders specialize in helping individuals with challenging credit histories. The key is to understand your options and manage expectations.

Understanding Subprime Loans

Subprime auto loans are specifically designed for borrowers with low credit scores (typically below 620 FICO). While these loans are "easier to get" in terms of approval, they generally come with higher interest rates and less favorable terms to compensate for the increased risk to the lender.

It’s crucial to understand the total cost of a subprime loan. While the monthly payment might seem manageable, the overall interest paid can be significantly higher. Use these loans as an opportunity to rebuild credit.

Special Finance Dealerships

Many dealerships have "special finance" departments that work with a network of lenders catering to subprime borrowers. They are often equipped to find solutions for those with bad credit, no credit, or even bankruptcies.

While convenient, always compare their offers. Based on my experience, dealership financing can sometimes have higher rates than what you might find with an independent online lender or credit union specializing in bad credit auto loans.

Secured Loans and Building Credit

In some cases, lenders might offer a secured car loan where the car itself acts as collateral. This is standard for most car loans, but for those with poor credit, it might be the only option. Some lenders might also offer programs designed to help you build credit with responsible payments.

The goal should be to get approved, make timely payments, and then potentially refinance to a better rate once your credit score improves. This turns an initial "easy to get" but higher-rate loan into a stepping stone.

Common mistakes to avoid are: falling for "guaranteed approval" scams, which often hide exorbitant rates and fees. Always read the fine print.

The Application Process: Step-by-Step for a Smooth Experience

Once you’ve done your homework and chosen a lender, the application process itself is fairly straightforward. Being prepared will make it feel easy and efficient.

1. Gather Your Documents

Lenders will typically require a range of documents to verify your identity, income, and residence. Having these ready will expedite the process.

Commonly requested documents include:

- Government-issued photo ID (driver’s license)

- Proof of income (pay stubs, tax returns, bank statements)

- Proof of residence (utility bill, lease agreement)

- Social Security number

- Vehicle information (if you’ve already chosen a car)

2. Fill Out the Application Accurately

Whether online or in person, complete the application truthfully and thoroughly. Inaccurate information can lead to delays or even denial. If you have questions, don’t hesitate to ask the lender for clarification.

3. Understand Loan Offers and Compare

If approved, you might receive one or more loan offers. Carefully review each offer, paying close attention to:

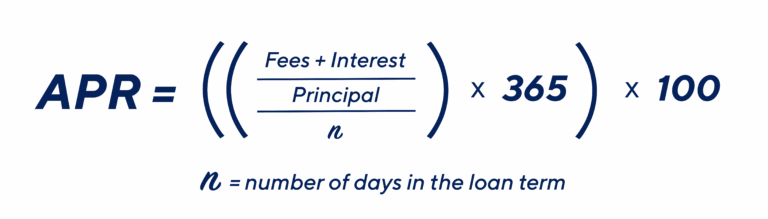

- Interest Rate (APR): This is the true cost of borrowing, including fees.

- Loan Term: The length of time you have to repay the loan (e.g., 36, 48, 60, 72 months).

- Monthly Payment: Ensure it fits comfortably within your budget.

- Total Cost of the Loan: The sum of all payments over the loan term.

Don’t just look at the monthly payment. A longer loan term might mean lower monthly payments but significantly more interest paid over time.

4. Read the Fine Print and Ask Questions

Before signing anything, read the entire loan agreement. Understand all terms, conditions, and any potential fees (e.g., late payment fees, prepayment penalties). If anything is unclear, ask. A reputable lender will be happy to explain.

This due diligence ensures there are no surprises down the road, making the actual financing experience truly easy.

Common Mistakes to Avoid When Seeking an Easy Car Loan

Even with the best intentions, borrowers can fall into common traps. Avoiding these pitfalls will save you money, stress, and make your car loan journey genuinely easier.

1. Applying to Too Many Lenders at Once

Each time you apply for a loan, it results in a "hard inquiry" on your credit report. While multiple inquiries for the same type of loan within a short period (typically 14-45 days, depending on the scoring model) are often grouped as one for scoring purposes, too many inquiries outside this window can negatively impact your credit score.

Instead, research lenders, get pre-approved by a few, and then compare offers. This targeted approach is more effective.

2. Not Reading the Terms and Conditions

As mentioned, skipping the fine print is a recipe for disaster. You might miss hidden fees, high interest rates, or unfavorable clauses. Always read the entire loan agreement before signing.

3. Focusing Only on the Monthly Payment

While a low monthly payment is appealing, it can be deceiving. Lenders might extend the loan term to lower the payment, but this often means you pay significantly more in interest over the life of the loan.

Always consider the total cost of the loan, not just the monthly installment. This holistic view ensures you’re getting a genuinely easy car loan, not just an easy-looking payment.

4. Buying More Car Than You Can Afford

It’s easy to get caught up in the excitement of a new car. However, purchasing a vehicle that strains your budget can lead to financial stress and difficulty making payments. Remember to factor in insurance, maintenance, and fuel costs.

A car loan should enhance your life, not burden it. Stick to your pre-determined budget.

5. Ignoring Your Credit Score

Many people jump into car shopping without understanding their credit standing. Your credit score dictates the rates you qualify for. Ignoring it means you’re walking into negotiations blind, potentially accepting higher rates than you deserve.

Pro tips from us: knowing your score is power. It allows you to target appropriate lenders and vehicles.

Pro Tips for Securing the Best Easy Car Loan

Beyond the foundational strategies, a few expert tips can further smooth your path to car ownership and ensure you get the most favorable terms possible.

Negotiate Everything

Don’t just accept the first offer, whether it’s for the car price or the loan terms. Everything is negotiable. If you have a pre-approval, use it as leverage to get a better rate from the dealership’s finance department.

Even a small reduction in the interest rate can save you hundreds, if not thousands, of dollars over the life of the loan. Negotiation is a key skill for truly easy car loans.

Consider Refinancing Later

If you initially secured a car loan with a higher interest rate due to a lower credit score, don’t despair. After 6-12 months of consistent, on-time payments, your credit score is likely to improve.

At that point, you can explore refinancing your car loan. Refinancing allows you to get a new loan with a lower interest rate, reducing your monthly payments and the total cost of the loan. This strategy turns an initially "less easy" loan into a manageable one.

Build Your Credit Actively

View your car loan as an opportunity to build or rebuild your credit history. Make every payment on time, every month. This consistent positive activity will reflect well on your credit report, opening doors to better financial opportunities in the future.

A good credit history is the ultimate key to effortlessly securing future loans, making every financing experience "easy."

Conclusion: Driving Towards Your Easy Car Loan

Securing an "easy to get car loan" isn’t about finding a shortcut; it’s about being informed, prepared, and strategic. By understanding what lenders look for, actively working to improve your financial profile, and diligently comparing your options, you can transform a potentially stressful process into a smooth and successful one.

From checking your credit and saving for a down payment to exploring various lenders and understanding the fine print, every step you take brings you closer to driving away in the car you need, with a loan that fits your life. Remember, the goal is not just approval, but approval on favorable terms that support your financial well-being.

Take control of your car financing journey. Apply the strategies outlined in this guide, and you’ll find that an easy car loan is not just a possibility, but a tangible reality. Your ideal car awaits, and with the right approach, the financing won’t be a hurdle, but a bridge to ownership.

For more trusted financial advice and tools, we recommend visiting the Consumer Financial Protection Bureau (CFPB) website at consumerfinance.gov.