Your Ultimate Guide to Getting a Car Loan from Bank of America: Navigate the Road to Your New Ride

Your Ultimate Guide to Getting a Car Loan from Bank of America: Navigate the Road to Your New Ride Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used vehicle is an exciting prospect, but the financing aspect can often feel daunting. For many, a reliable and established financial institution is the preferred choice, and Bank of America stands out as a prominent player in the auto loan market. Getting a car loan from Bank of America can be a streamlined and beneficial experience if you approach it with the right knowledge and preparation.

This comprehensive guide is designed to be your go-to resource, breaking down every facet of securing an auto loan through Bank of America. We’ll explore everything from understanding their offerings to navigating the application process, ensuring you’re well-equipped to make informed decisions and drive away with confidence. Our goal is to provide you with insights that not only clarify the process but also help you secure the best possible terms for your vehicle financing.

Your Ultimate Guide to Getting a Car Loan from Bank of America: Navigate the Road to Your New Ride

Why Consider Bank of America for Your Auto Loan?

When it comes to auto financing, Bank of America is a name that resonates with trust and extensive reach. Their long-standing presence in the financial sector brings a level of stability and experience that many borrowers value highly. Opting for a BoA car loan means aligning yourself with a lender known for its comprehensive services and competitive offerings.

One significant advantage is their extensive network and digital capabilities. Whether you prefer to apply online, through their mobile app, or in person at one of their many branches, Bank of America offers flexibility. This accessibility ensures that you can manage your loan application and subsequent payments with ease, fitting seamlessly into your busy schedule.

Furthermore, existing Bank of America customers, especially those enrolled in their Preferred Rewards program, may find additional benefits. These can include interest rate discounts, making an already competitive offer even more attractive. This is a powerful incentive for individuals who already have a banking relationship with the institution.

Understanding Bank of America’s Car Loan Offerings

Bank of America provides a variety of auto loan products designed to meet different purchasing scenarios. Understanding these options is the first step in tailoring a loan that fits your specific needs. Each type of loan has distinct characteristics and requirements, which we will delve into here.

New Car Loans

For those eyeing a brand-new vehicle rolling off the dealership lot, Bank of America offers specific new car loans. These loans are typically for vehicles no older than the current model year or one year prior, with low mileage. The appeal of a new car loan often lies in potentially lower interest rates compared to used car loans, given the depreciating value of a new vehicle is less immediately impactful.

When applying for a new car loan, Bank of America assesses various factors, including your creditworthiness and the vehicle’s value. They finance a wide range of new makes and models, making it a popular choice for buyers who want the latest features and warranty protection. The terms for new car loans can also be more flexible, often extending to longer repayment periods.

Used Car Loans

If a pre-owned vehicle is more your speed, Bank of America also offers robust used car loan options. These loans are designed for vehicles that have been previously owned, typically up to seven or eight model years old, with certain mileage restrictions. Used car loans can be an excellent way to get a quality vehicle at a more affordable price point.

The interest rates on used car loans might be slightly higher than those for new cars, reflecting the greater depreciation risk associated with older vehicles. However, Bank of America remains competitive, and your personal credit profile plays a huge role in determining your final rate. It’s crucial to ensure the used vehicle you choose meets their specific criteria for age and mileage to qualify.

Refinancing Car Loans

Perhaps you already have a car loan but are looking for a better deal. Bank of America’s refinancing car loan option could be your solution. Refinancing involves taking out a new loan to pay off your existing auto loan, ideally at a lower interest rate or with more favorable terms. This can significantly reduce your monthly payments or the total interest paid over the life of the loan.

Based on my experience, many people consider refinancing when their credit score has improved since they first took out their original loan, or when market interest rates have dropped. Pro tips from us: Always compare the new loan’s total cost, including any fees, against the savings you’d gain from a lower interest rate. This ensures refinancing is genuinely beneficial for your financial situation.

Private Party Sales Loans

One unique offering from Bank of America is their ability to finance vehicles purchased from a private seller, not just dealerships. This can be incredibly advantageous if you’ve found a great deal on a car through an individual seller. Many lenders shy away from private party loans due to increased risk, making BoA’s offering quite valuable.

For a private party sale loan, Bank of America will typically require an inspection of the vehicle and proof of clear title. The process ensures both the buyer and the bank are protected. This option significantly broadens your car-buying horizons, allowing you to explore a wider market beyond traditional dealerships.

Essential Pre-Application Steps: Paving Your Way to Approval

Before you even think about submitting a car loan application, a few crucial preparatory steps can dramatically increase your chances of approval and secure better terms with Bank of America. Think of this as laying a solid foundation for your financial success. Skipping these steps is a common mistake that can lead to disappointment or less favorable loan conditions.

Check Your Credit Score

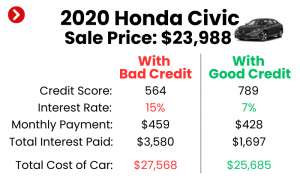

Your credit score is arguably the most critical factor in securing any loan, and a BoA car loan is no exception. Lenders use your credit score to assess your creditworthiness and your likelihood of repaying the loan. A higher score typically translates to lower interest rates and more flexible terms.

It’s vital to obtain your credit report from all three major bureaus (Experian, Equifax, and TransUnion) well in advance. Review them for any errors or discrepancies that could negatively impact your score. If you find any, dispute them immediately. Understanding your score allows you to set realistic expectations and potentially take steps to improve it before applying. For a deeper dive into understanding your credit score, you can visit a trusted resource like Experian’s Credit Score Guide.

Understand Your Budget

Before you fall in love with a car you can’t truly afford, take a hard look at your finances. Your budget should encompass more than just the monthly loan payment. Consider insurance costs, fuel, maintenance, registration fees, and any potential repairs. A common mistake to avoid is focusing solely on the monthly payment without considering the total cost of ownership.

Determine how much you can comfortably afford to pay each month without straining your finances. This involves calculating your income versus your fixed and variable expenses. Having a clear budget will guide your vehicle selection and prevent you from overextending yourself financially.

Gather Required Documents

Being prepared with all necessary documentation streamlines the application process. Bank of America, like other lenders, will require specific documents to verify your identity, income, and residency. Having these ready prevents delays and demonstrates your readiness as a serious applicant.

Common documents include a valid government-issued ID (driver’s license or passport), proof of income (pay stubs, tax returns, or bank statements), proof of residency (utility bill or lease agreement), and potentially information about the vehicle you intend to purchase. For a comprehensive list, it’s always wise to check Bank of America’s official website or speak with a loan officer.

Research Vehicles

Having a general idea of the type of car you want is beneficial before applying for a loan. This isn’t just about personal preference; it also helps you understand typical price ranges and allows you to better estimate your loan amount. Bank of America will need details about the vehicle if you’re approved, so knowing what you’re looking for helps the process.

Researching vehicles also involves understanding their market value. Websites like Kelley Blue Book (KBB) or Edmunds can provide estimated values for new and used cars. This knowledge empowers you to negotiate effectively with sellers and ensures you’re not overpaying for your chosen vehicle.

The Bank of America Pre-Approval Process: A Smart First Move

Securing a pre-approval for a Bank of America auto loan is arguably the most powerful step you can take in your car-buying journey. It’s a strategic move that offers numerous advantages, transforming you from a mere shopper into a confident buyer. Understanding this process is key to leveraging its benefits.

What is Pre-Approval?

Pre-approval is when a lender, like Bank of America, reviews your financial information and tentatively agrees to lend you a certain amount of money for a car, at a specific interest rate and term, before you’ve even picked out the vehicle. It’s not a final loan offer but a strong indication of what you qualify for.

This process involves a soft credit inquiry, which doesn’t impact your credit score. If you proceed with the actual loan application, a hard inquiry will be made. The pre-approval letter typically has an expiration date, giving you a window to find your perfect car.

Benefits of Pre-Approval

The advantages of pre-approval are significant. Firstly, it gives you a clear understanding of your budget. You’ll know exactly how much you can afford, preventing you from looking at cars outside your price range. This saves time and avoids potential disappointment.

Secondly, a pre-approval letter gives you immense negotiating power at the dealership. You walk in as a cash buyer, having already secured your financing. This allows you to focus solely on negotiating the car’s price, rather than getting entangled in discussions about financing terms. Dealers are often more willing to offer their best price when they know your financing is already in place.

How to Get Pre-Approved with Bank of America

Getting a car loan from Bank of America pre-approval is a straightforward process. You can typically apply online through their dedicated auto loan portal, or you can visit a Bank of America branch to speak with a loan specialist. The online application is often the quickest and most convenient method.

You’ll need to provide personal information such as your name, address, Social Security number, and employment details. You’ll also be asked about your income and any existing debts. The more accurate and complete information you provide, the smoother the pre-approval process will be.

The Application Process for a Bank of America Car Loan

Once you’ve done your homework, understand your budget, and ideally, have a pre-approval in hand, it’s time for the formal car loan application. This is where your financial journey with Bank of America solidifies. The process is designed to be efficient, whether you choose to apply digitally or in person.

Step-by-Step Guide to Applying

The application process typically begins online for most applicants. You’ll navigate to the auto loan section of the Bank of America website or use their mobile app. The application form will guide you through various sections, requesting detailed personal and financial information.

You’ll need to input your full legal name, contact information, date of birth, and Social Security number. Following this, you’ll provide employment details, including your employer’s name, your position, and your annual income. Bank of America will also ask for information about your assets and liabilities to get a complete picture of your financial health.

Finally, you’ll provide details about the vehicle you intend to purchase, including the make, model, year, and VIN (Vehicle Identification Number) if you have it. If you’re applying for a pre-approval, some of the vehicle-specific fields might be optional at this stage.

What Happens After Submission

After you submit your application, Bank of America’s underwriting team will review your information. They will perform a hard credit inquiry, which may temporarily ding your credit score by a few points. This is a standard procedure for formal loan applications.

You may receive an immediate decision if your application is straightforward and all information is readily verifiable. However, some applications may require further review, and a loan officer might contact you for additional documents or clarification. This could include recent pay stubs, bank statements, or even a copy of your vehicle’s purchase agreement.

Key Factors Influencing Your Bank of America Car Loan Approval & Rates

When getting a car loan from Bank of America, several critical factors come into play that directly impact whether your application is approved and, if so, what interest rate you’ll receive. Understanding these elements can help you optimize your financial standing before applying.

Credit Score: The Cornerstone of Approval

As mentioned, your credit score is paramount. Bank of America, like most lenders, uses this three-digit number to gauge your credit risk. Generally, a higher credit score (e.g., 700+) indicates a lower risk, making you eligible for their most competitive interest rates. Conversely, a lower score might lead to higher rates or even denial.

It reflects your history of borrowing and repaying debt. A consistent record of on-time payments, a low credit utilization ratio, and a diverse credit mix all contribute to a strong credit score. If your score isn’t where you want it to be, taking steps to improve it before applying can save you thousands over the life of the loan.

Debt-to-Income Ratio (DTI)

Your Debt-to-Income (DTI) ratio is another crucial metric Bank of America evaluates. It’s the percentage of your gross monthly income that goes towards paying your monthly debt payments. A low DTI indicates that you have plenty of income left after covering your debts, suggesting you can comfortably handle new loan payments.

For instance, if your gross monthly income is $5,000 and your total monthly debt payments (credit cards, student loans, mortgage) are $1,500, your DTI is 30% ($1,500 / $5,000). Lenders generally prefer a DTI of 36% or lower, though some may go higher depending on other factors. Common mistakes to avoid are applying for a loan when your DTI is already high, as this signals financial strain.

Income Stability and Employment History

Bank of America wants to see that you have a stable and reliable source of income to make your loan payments. This often means consistent employment history, ideally with the same employer for a significant period (e.g., two years or more). If you’re self-employed, you’ll likely need to provide more extensive financial documentation, such as tax returns, to prove income stability.

They are looking for reassurance that your ability to earn money is consistent and predictable. This minimizes their risk and increases your chances of car loan approval. Any significant gaps in employment or frequent job changes might raise red flags, necessitating further explanation.

Down Payment Amount

Making a substantial down payment can significantly influence your loan terms. A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over time. It also signals to Bank of America that you’re a serious and responsible borrower.

Furthermore, a healthy down payment provides an immediate equity cushion, reducing the risk of being "upside down" on your loan (owing more than the car is worth). While Bank of America doesn’t always require a down payment, pro tips from us suggest aiming for at least 10-20% of the vehicle’s price if possible, as it can lead to better rates and a smoother approval process.

Vehicle Age and Mileage

The age and mileage of the vehicle you intend to purchase also play a role, especially for used car loans. Bank of America, like other lenders, has criteria for the maximum age and mileage of a vehicle they are willing to finance. Older vehicles with high mileage are considered higher risk due to potential mechanical issues and faster depreciation.

These factors can impact both your approval and the interest rate offered. Newer vehicles, whether new or certified pre-owned, often qualify for more favorable terms. Always confirm Bank of America’s specific vehicle requirements before finalizing your car choice.

Loan Term

The length of your loan, or the loan term, also impacts your monthly payments and the total interest paid. Shorter terms (e.g., 36 or 48 months) result in higher monthly payments but less total interest. Longer terms (e.g., 60 or 72 months) offer lower monthly payments but accumulate more interest over time.

While a longer term might seem appealing due to lower monthly costs, it’s crucial to weigh the increased interest paid against your budget. Bank of America offers various terms, allowing you to choose one that balances affordability with overall cost.

What to Do If Your Loan is Approved (or Denied)

The moment of truth arrives when Bank of America delivers a decision on your auto financing application. Whether you receive an approval or a denial, knowing how to proceed is crucial. This section guides you through the next steps for both scenarios.

If Your Loan is Approved

Congratulations! If your Bank of America auto loan is approved, you’ll receive an offer outlining the loan amount, interest rate, repayment term, and monthly payment. It’s essential to meticulously review all these terms before signing anything. Don’t hesitate to ask questions if anything is unclear.

Once you accept the terms, Bank of America will guide you through the finalization process. This typically involves signing the loan agreement, and then funds will be disbursed directly to the dealership or seller. Make sure all conditions outlined in your pre-approval, if applicable, are reflected in the final agreement.

Pro tips from us: Even after approval, ensure you understand all associated fees, such as origination fees or late payment penalties. Knowledge is power, and being fully informed about your loan terms prevents any surprises down the road.

If Your Loan is Denied

A denial can be disheartening, but it’s not the end of your car-buying journey. The first step is to understand why your loan was denied. Bank of America is legally required to provide you with an Adverse Action Notice, which will state the specific reasons for the denial. Common reasons include a low credit score, high debt-to-income ratio, insufficient income, or an unstable employment history.

Once you know the reason, you can take corrective action. This might involve working to improve your credit score, paying down existing debt to lower your DTI, or saving for a larger down payment. Consider applying with a co-signer who has strong credit, as this can significantly boost your chances of approval. Alternatively, explore other lenders or credit unions that might have more flexible criteria, or consider buying a less expensive vehicle. Don’t give up; use the denial as a learning opportunity to strengthen your financial profile.

Managing Your Bank of America Car Loan

Once you’ve successfully secured your BoA car loan and are driving your new vehicle, the journey shifts to responsible loan management. Bank of America makes it convenient to manage your auto loan, ensuring you can stay on track with your payments and financial goals.

Online Account Management

Bank of America provides robust online and mobile banking platforms that allow you to manage your auto loan with ease. You can access your loan details, view payment history, and set up automatic payments through your online account. This digital convenience helps you stay organized and ensures you never miss a payment.

Setting up automatic payments directly from your Bank of America checking or savings account is highly recommended. It eliminates the risk of late payments, which can negatively impact your credit score and incur late fees. You can also view your remaining balance and payment schedule at any time.

Payment Options

Beyond automatic payments, Bank of America offers several flexible payment options. You can make one-time payments online, through their mobile app, over the phone, or even by mail. This flexibility caters to different preferences and ensures you always have a way to make your payments on time.

If you ever find yourself in a tight spot, it’s always best to communicate with Bank of America’s customer service as soon as possible. They may be able to discuss options or provide guidance, though it’s important to remember that payment deferrals or modifications are usually granted on a case-by-case basis and not guaranteed.

Early Payoff Considerations

Many borrowers consider paying off their car loan early to save on interest. Bank of America generally does not charge prepayment penalties on their auto loans, which is a significant advantage. This means you can make extra payments or pay off the entire balance without incurring additional fees.

Pro tips from us: If you plan to pay extra, ensure your payments are applied directly to the principal balance to maximize your interest savings. You can usually specify this when making an additional payment through their online portal or by contacting customer service. Paying off early can free up cash flow and accelerate your journey to financial freedom. If you’re thinking about managing multiple loans and optimizing your financial portfolio, our article on could be a great resource.

Customer Service and Support

Bank of America offers comprehensive customer service for their auto loan customers. Whether you have questions about your statement, need assistance with online banking, or want to discuss payment options, their support team is readily available. You can reach them via phone, secure message through your online account, or by visiting a local branch.

Having reliable customer support is a valuable asset, especially when dealing with financial products. It provides peace of mind knowing that help is just a call or click away should any issues arise during the life of your loan.

Conclusion: Driving Forward with Confidence

Navigating the path to getting a car loan from Bank of America doesn’t have to be a complex ordeal. By understanding the various loan options, diligently preparing your finances, leveraging the power of pre-approval, and managing your loan responsibly, you can make the entire process smooth and successful. This pillar content piece has aimed to provide you with an exhaustive roadmap, equipping you with the knowledge to make informed decisions every step of the way.

Remember, responsible auto financing is about more than just securing a loan; it’s about choosing the right partner and terms that align with your financial health. Bank of America offers a robust platform and competitive products, making them a strong contender for your car loan needs. With the insights shared in this guide, you are now well-prepared to confidently pursue your next vehicle purchase. Take these steps, prepare thoroughly, and drive away knowing you’ve made a smart financial choice.