Your Ultimate Guide to Getting a Car Loan Online: A Step-by-Step Journey to Approval

Your Ultimate Guide to Getting a Car Loan Online: A Step-by-Step Journey to Approval Carloan.Guidemechanic.com

In today’s fast-paced digital world, almost everything can be done online – and getting a car loan is no exception. Gone are the days of spending hours at a dealership, negotiating financing blind. Now, the power to secure your next vehicle’s funding is right at your fingertips.

But how exactly does one navigate the seemingly complex process of obtaining a car loan online? Is it truly easier, and what are the secrets to ensuring a smooth journey to approval? As an expert blogger and someone who has guided countless individuals through this very process, I can tell you it’s not only possible but often preferable. This comprehensive guide will demystify every step, ensuring you’re well-equipped to get a car loan online with confidence.

Your Ultimate Guide to Getting a Car Loan Online: A Step-by-Step Journey to Approval

We’ll cover everything from crucial pre-application preparations to understanding the fine print, all designed to give you the best chance of approval and a fantastic deal.

Why Choose an Online Car Loan? Convenience Meets Competitive Rates

The shift towards online financial services has transformed how we approach major purchases. When it comes to getting a car loan online, the benefits are compelling and numerous, offering a significant advantage over traditional methods.

Firstly, unparalleled convenience stands out. You can research, compare, and apply for an online car loan from the comfort of your home, anytime that suits you. No more rigid bank hours or pressure-filled dealership finance offices. This flexibility saves you valuable time and reduces stress.

Secondly, the online marketplace fosters fierce competition among lenders. This means you have access to a wider array of options, potentially leading to lower interest rates and more favorable terms. Comparing offers from multiple lenders is dramatically easier online, allowing you to secure the best possible deal for your financial situation.

Finally, the speed of the online process is remarkable. Many online lenders offer instant pre-approvals, giving you a clear picture of your borrowing power within minutes. This efficiency empowers you to shop for your car with a confirmed budget, turning a potentially daunting task into an exciting prospect.

Essential Preparations Before You Apply: Laying Your Foundation for Success

Securing an online auto loan isn’t just about filling out a form. It’s about strategic preparation that significantly boosts your approval chances and helps you land the best rates. Based on my experience, neglecting these initial steps is a common mistake that can lead to frustration and less favorable loan terms.

1. Understand Your Credit Score: Your Financial Report Card

Your credit score is arguably the most critical factor in your online car loan application. Lenders use it to assess your creditworthiness, directly influencing the interest rate you’ll be offered. A higher score typically means lower interest rates and better terms.

Before you even think about applying, pull your credit reports. You can get free copies from AnnualCreditReport.com, the only federally authorized source. Reviewing your reports allows you to identify any errors and understand your current credit standing.

Pro tip from us: If your score isn’t where you want it to be, take steps to improve it. Pay down existing debts, make all payments on time, and avoid opening new lines of credit just before applying for a car loan. Even a small bump in your score can translate into significant savings over the life of the loan.

2. Determine Your Budget: Beyond the Monthly Payment

Knowing what you can truly afford is paramount. This isn’t just about the monthly car payment; it involves a holistic view of car ownership costs. Consider insurance, fuel, maintenance, and potential registration fees alongside your loan payment.

Use online car loan calculators to estimate monthly payments based on different loan amounts, interest rates, and terms. This helps you understand how these variables impact your budget. Aim for a payment that fits comfortably within your existing financial commitments without stretching you thin.

Common mistakes to avoid are underestimating these additional costs. A car might look affordable on paper, but if you can’t cover the ongoing expenses, it quickly becomes a burden. Be realistic about your financial capacity.

3. Gather Necessary Documents: Be Ready to Go

Online lenders, like traditional ones, require documentation to verify your identity, income, and residency. Having these documents prepared and organized before you start the application process will streamline everything. It shows lenders you are serious and organized.

Here’s a typical list of documents you’ll likely need:

- Proof of Identity: Government-issued ID (driver’s license, passport).

- Proof of Income: Recent pay stubs (1-3 months), W-2s, tax returns (for self-employed individuals).

- Proof of Residency: Utility bill, lease agreement, or mortgage statement.

- Social Security Number: For credit checks.

- Vehicle Information: (If you’ve already chosen a car) VIN, make, model, year, mileage.

Having digital copies of these documents ready to upload can significantly speed up your application.

The Online Car Loan Application Process: Your Step-by-Step Guide

With your preparations complete, you’re ready to dive into the exciting part: finding and securing your online auto financing. This process is generally straightforward, but understanding each step will give you a clear advantage.

Step 1: Research and Compare Online Lenders

This is where the true power of getting a car loan online shines. The internet offers a vast landscape of lenders, each with unique offerings. Don’t just settle for the first one you find.

- Banks: Many traditional banks offer online car loan applications.

- Credit Unions: Often known for competitive rates and personalized service, many have robust online platforms.

- Online-Only Lenders: Companies specializing in digital lending can offer very streamlined processes and innovative products.

Compare interest rates (APR), loan terms, fees (origination, late payment), and customer reviews. Look for lenders with transparent processes and excellent customer support. Pro tips from us: Read the fine print on any advertised rates; sometimes, the lowest rates are reserved for those with impeccable credit.

Step 2: Get Pre-Approved (Highly Recommended)

Pre-approval is a game-changer when seeking a car loan online. It means a lender has reviewed your basic financial information and determined how much they are willing to lend you, along with an estimated interest rate.

The beauty of pre-approval is that it typically involves a "soft inquiry" on your credit, which doesn’t negatively impact your score. It provides you with a concrete budget, empowering you to negotiate with dealerships as a cash buyer. You’ll know exactly what you can afford, avoiding the pressure to overspend.

Based on my experience, walking into a dealership with a pre-approval letter gives you significant leverage. It shifts the focus from "Can I get a loan?" to "Which car do I want within my approved budget?"

Step 3: Complete the Full Application

Once you’ve chosen a lender and ideally received pre-approval, you’ll proceed with the full application. This usually involves providing more detailed information and uploading the documents you gathered earlier.

Accuracy is key here. Double-check all information before submitting to avoid delays. Be honest and transparent; lenders will verify your details. The online forms are typically user-friendly, guiding you through each section.

If you have questions, don’t hesitate to reach out to the lender’s customer service. Most online lenders offer chat, email, or phone support to assist applicants.

Step 4: Review and Accept the Offer

Congratulations! You’ve received a loan offer. This is a critical juncture where attention to detail is paramount. Don’t rush to sign.

Carefully review the loan agreement. Pay close attention to:

- Annual Percentage Rate (APR): This is the true cost of borrowing, including interest and some fees.

- Loan Term: How long you have to repay the loan (e.g., 36, 60, 72 months).

- Monthly Payment: Ensure it aligns with your budget.

- Total Cost of the Loan: Calculate how much you’ll pay back over the entire term.

- Any Fees: Origination fees, prepayment penalties, etc.

If anything is unclear, ask for clarification. Once you’re satisfied, you can usually accept the offer digitally. The funds will then be disbursed according to the lender’s process, often directly to the dealership or sometimes to you.

Key Factors Influencing Your Loan Approval & Rates

While the steps are clear, several underlying factors heavily influence whether your online car loan application is approved and what kind of interest rate you receive. Understanding these can help you optimize your chances.

1. Credit Score: The Foremost Indicator

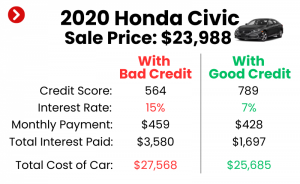

We’ve mentioned it before, but it bears repeating: your credit score is crucial. It’s a numerical representation of your creditworthiness. Lenders use it to predict the likelihood of you repaying the loan. A higher score (generally 700+) typically qualifies you for the lowest rates.

2. Debt-to-Income (DTI) Ratio: Your Financial Burden

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders want to see that you have enough disposable income to comfortably afford the new car payment. A lower DTI (ideally below 43%) indicates less financial risk.

3. Loan-to-Value (LTV) Ratio: The Car’s Worth

The LTV ratio compares the amount you’re borrowing to the car’s actual market value. If you’re borrowing more than the car is worth (high LTV), it’s riskier for the lender. This can happen if you roll negative equity from a trade-in into the new loan. A lower LTV, often achieved with a good down payment, is more attractive to lenders.

4. Down Payment Amount: Your Commitment

A substantial down payment reduces the amount you need to borrow, lowering your monthly payments and the total interest paid. It also signals to lenders that you are financially committed and less likely to default. Lenders prefer applicants who put some money down.

5. Loan Term: Duration of Your Repayment

The loan term is how long you have to repay the loan. Shorter terms typically mean higher monthly payments but lower total interest paid. Longer terms offer lower monthly payments but accumulate more interest over time. Lenders might view very long terms (e.g., 84 months) as riskier due to increased depreciation and potential for default.

6. Vehicle Age & Mileage: The Asset’s Risk

Lenders also consider the vehicle itself. Newer cars with lower mileage are generally less risky for lenders because they hold their value better and are less likely to require expensive repairs that could strain your budget. Older, high-mileage vehicles might have higher interest rates or be harder to finance.

Common Mistakes to Avoid When Getting an Online Car Loan

Even with the best intentions, applicants can stumble. From my experience, these are the pitfalls that often trip people up, leading to higher rates or even rejection. Avoiding them will significantly smooth your path to approval.

- Not Checking Your Credit Score: This is a fundamental oversight. You need to know where you stand to set realistic expectations and fix any errors.

- Skipping Pre-Approval: As discussed, pre-approval is a powerful tool. Not getting it means you’re negotiating blindly and potentially accepting whatever financing the dealership offers, which might not be the best deal.

- Only Applying to One Lender: Limiting yourself to a single option means you miss out on the competitive nature of online lending. Always compare offers from at least 3-5 different lenders.

- Not Reading the Fine Print: Every loan agreement has terms and conditions. Failure to read and understand them can lead to unexpected fees, penalties, or unfavorable clauses.

- Overlooking Additional Costs: Focusing solely on the monthly payment can be misleading. Remember to factor in insurance, maintenance, fuel, and registration costs into your overall budget.

- Applying for Too Many Loans at Once: While comparing is good, submitting multiple full applications (which trigger hard credit inquiries) within a short period can negatively impact your credit score. Stick to pre-approvals first, then finalize with your chosen few.

Special Situations: Bad Credit & No Credit Car Loans Online

What if your credit score isn’t perfect, or you’re just starting your credit journey? Don’t despair. Getting a car loan online is still possible, though the process might require a slightly different approach.

Can You Get a Car Loan Online with Bad Credit?

Yes, you can! Many online lenders specialize in bad credit car loans online. These are often called subprime lenders. While the interest rates will likely be higher to compensate for the increased risk, it’s a viable path to vehicle ownership and, importantly, a chance to rebuild your credit.

Tips for bad credit applicants:

- Increase Your Down Payment: A larger down payment reduces the loan amount and shows the lender you’re serious.

- Find a Co-signer: A co-signer with good credit can significantly improve your chances of approval and secure a better rate.

- Be Realistic: You might not get the car of your dreams or the lowest rate, but focus on getting a reliable vehicle that helps you build credit.

- Explore Specific Bad Credit Lenders: Search specifically for "bad credit auto loans online" to find lenders tailored to your situation.

Getting an Online Car Loan with No Credit

If you have no credit history, the challenge is similar to bad credit, as lenders have no data to assess your risk. However, it’s often viewed slightly more favorably than truly bad credit.

Strategies for no-credit applicants:

- Start Building Credit: Even small steps like a secured credit card or a small personal loan can establish a credit history.

- Co-signer: Again, a co-signer can be immensely helpful.

- Consider a Smaller, More Affordable Car: Less risk for the lender.

- Look for Lenders Specializing in First-Time Buyers: Some online platforms cater specifically to individuals with limited credit history.

Pro Tips for a Smooth Online Car Loan Experience

Beyond the steps and pitfalls, here are some invaluable insights to make your journey even smoother.

- Organize Documents Digitally: Create a dedicated folder on your computer for all your financial documents. This makes uploading a breeze and keeps everything organized.

- Be Honest and Transparent: Always provide accurate information. Lenders will verify it, and discrepancies can lead to delays or rejection.

- Don’t Be Afraid to Negotiate (Even Online): While rates are often fixed, some lenders might be open to discussing terms, especially if you have multiple pre-approvals.

- Consider Refinancing Later: If you get a higher interest rate due to credit issues, you can always work on improving your credit and refinance the loan later for a better rate.

- Monitor Your Credit Regularly: Keep an eye on your credit report even after approval. This helps you stay informed and catch any fraudulent activity early. (Internal Link: For more details on managing your credit, check out our guide on "Understanding Your Credit Score: A Comprehensive Guide".)

- Factor in Insurance Costs: Get insurance quotes before finalizing your car purchase. Insurance can be a significant ongoing expense, and it varies greatly based on the vehicle and your driving history. (Internal Link: Learn more about budgeting for your vehicle in our article, "Budgeting for Your New Car: Beyond the Monthly Payment".)

Conclusion: Empowering Your Car Buying Journey

Getting a car loan online is no longer a futuristic concept; it’s a practical, efficient, and often more advantageous way to finance your next vehicle. By understanding the process, preparing diligently, and avoiding common pitfalls, you empower yourself to secure the best possible terms.

The convenience, competitive rates, and speed offered by online lenders make them a compelling alternative to traditional financing. Remember, knowledge is power. Armed with the insights from this guide, you are now well-equipped to navigate the world of online auto financing with confidence.

So, take control of your car buying journey. Start your research, get pre-approved, and step into the dealership ready to make an informed decision. Your dream car, financed on your terms, is just a few clicks away.