Your Ultimate Guide to Mastering Your Car Purchase with a Car Loan Calculator Malaysia

Your Ultimate Guide to Mastering Your Car Purchase with a Car Loan Calculator Malaysia Carloan.Guidemechanic.com

The dream of owning a car is a significant milestone for many Malaysians. Whether it’s the sleek new model you’ve been eyeing or a reliable pre-owned vehicle, the journey often begins with understanding how you’ll finance it. This is where a powerful tool, the Car Loan Calculator Malaysia, becomes your indispensable companion. It’s more than just a simple calculation; it’s your window into financial clarity, helping you navigate the complexities of automotive financing with confidence.

In this comprehensive guide, we’ll delve deep into everything you need to know about car loans in Malaysia, how these calculators work, and crucial insights to empower your purchasing decision. Our goal is to equip you with the knowledge to make an informed choice, ensuring your car ownership journey starts on the right financial foot.

Your Ultimate Guide to Mastering Your Car Purchase with a Car Loan Calculator Malaysia

Understanding Car Loans in Malaysia: The Hire Purchase Landscape

Before we dive into the calculator, let’s clarify what a car loan typically entails in Malaysia. The vast majority of car financing here falls under the "Hire Purchase" (HP) agreement, governed by the Hire-Purchase Act 1967. This isn’t a direct loan where you own the car immediately. Instead, the bank or financial institution purchases the car, and you "hire" it from them, paying monthly installments. Ownership only transfers to you once the final payment is made.

This distinction is important because it influences how interest is calculated and how the agreement is structured. Understanding these fundamentals is the first step towards effectively using a Car Loan Calculator Malaysia.

The Core Components of a Car Loan Calculator: Deconstructing Your Payments

A car loan calculator isn’t magic; it’s a sophisticated tool that processes several key financial inputs to give you a clear picture of your potential monthly payments and total costs. Let’s break down these essential components.

1. The Car Price: Your Starting Point

This is the agreed-upon price of the vehicle you intend to purchase. Whether it’s a brand new car from a showroom or a used vehicle from a dealership, this figure forms the basis of your financing. Remember to include any sales tax or registration fees that might be rolled into the total vehicle cost.

A higher car price naturally translates to a larger loan amount and subsequently, higher monthly installments, assuming all other factors remain constant. It’s the foundational number for all subsequent calculations.

2. The Down Payment: Your Initial Investment

The down payment is the initial sum of money you pay upfront for the car. In Malaysia, financial institutions typically require a minimum down payment, often around 10% of the car’s price. However, you are always encouraged to pay more if your financial situation allows.

Based on my experience, making a larger down payment significantly reduces the principal loan amount. This not only lowers your monthly installments but also decreases the total interest you’ll pay over the loan tenure. It’s a smart financial move that can save you a substantial amount in the long run. Think of it as investing more of your own money upfront to borrow less.

3. The Loan Amount: What You Actually Borrow

This is the difference between the car price and your down payment. It’s the exact sum that the bank or financial institution will lend you. For example, if a car costs RM100,000 and you pay a RM10,000 down payment, your loan amount will be RM90,000.

The loan amount is crucial because it directly influences your monthly repayments and the total interest accrued. A smaller loan amount, achieved through a larger down payment, is always financially advantageous.

4. The Interest Rate: The Cost of Borrowing

The interest rate is arguably the most critical factor influencing the total cost of your car loan. In Malaysia, car loans (Hire Purchase) predominantly use a flat interest rate method. This means the interest is calculated on the original principal loan amount for the entire duration of the loan, regardless of how much principal you’ve already repaid.

This differs from a "reducing balance" method common in home loans, where interest is calculated on the remaining balance. Therefore, a Malaysia car loan interest rate of, say, 3% p.a. on a flat rate basis will result in a higher total interest paid compared to a 3% p.a. reducing balance rate. Factors influencing your interest rate include your credit score, income stability, the type of car (new vs. used), and the prevailing market conditions.

5. The Loan Tenure: How Long You’ll Pay

Loan tenure, or repayment period, refers to the length of time you have to repay your loan, typically expressed in years (e.g., 5 years, 7 years, 9 years). In Malaysia, the maximum car loan tenure is generally 9 years.

A longer loan tenure means lower monthly installments, making the car more "affordable" on a month-to-month basis. However, pro tips from us: a longer tenure also means you’ll pay significantly more in total interest over the life of the loan. Conversely, a shorter tenure leads to higher monthly payments but a much lower total interest cost. It’s a trade-off between monthly affordability and total cost.

How a Car Loan Calculator Malaysia Works: A Step-by-Step Guide

Using a car loan repayment calculator is straightforward, yet incredibly powerful. Most online calculators will ask for the following inputs:

- Car Price: Enter the full price of the vehicle.

- Down Payment: Input the amount you intend to pay upfront.

- Interest Rate: Enter the annual flat interest rate quoted by the bank.

- Loan Tenure: Select the number of years you plan to repay the loan.

Once you input these details, the calculator instantly computes your estimated monthly car payment Malaysia and the total interest you will pay over the entire loan period.

Let’s illustrate with an example:

- Car Price: RM80,000

- Down Payment: RM8,000 (10%)

- Loan Amount: RM72,000

- Interest Rate: 3.00% p.a. (flat rate)

- Loan Tenure: 7 years (84 months)

Using a hire purchase calculator Malaysia, the monthly installment would be calculated as follows:

- Total Interest: Loan Amount x Interest Rate x Loan Tenure in Years

RM72,000 x 0.03 x 7 = RM15,120 - Total Repayable Amount: Loan Amount + Total Interest

RM72,000 + RM15,120 = RM87,120 - Monthly Payment: Total Repayable Amount / Loan Tenure in Months

RM87,120 / 84 months = RM1,037.14 (approximately)

This calculation shows you not just the monthly commitment but also the significant amount of interest you’ll be paying. It allows you to adjust variables like down payment or tenure to see their immediate impact on your budget.

Beyond the Monthly Payment: Hidden Costs and Considerations

While the Car Loan Calculator Malaysia gives you a clear picture of your loan repayments, owning a car involves more than just your monthly installment. Neglecting these additional costs is a common mistake to avoid.

Here are other expenses you must factor into your budget:

- Road Tax & Insurance: These are annual mandatory costs. Insurance premiums vary based on car value, engine capacity, age, and your No-Claim Discount (NCD). Road tax depends on engine capacity. These can be substantial, especially for newer or higher-end vehicles.

- Maintenance Costs: Regular servicing, oil changes, tire rotations, and unexpected repairs are part and parcel of car ownership. Newer cars might have warranty-covered services, but older vehicles will require more attention.

- Fuel Costs: Depending on your daily commute and driving habits, fuel can be a significant recurring expense. Consider your average mileage and current fuel prices.

- Parking & Tolls: If you commute through toll roads or frequently pay for parking, these add up over time.

- Accessories & Upgrades: Window tinting, dashcams, sound system upgrades – these are often desired but come with additional costs.

Pro tips from us: Always create a holistic budget that includes these "hidden" costs, not just your loan payment. This ensures you have a realistic understanding of your total monthly car ownership expenditure.

Factors Affecting Your Car Loan Eligibility and Interest Rate

Getting approved for a car loan and securing a favorable interest rate isn’t solely about the car’s price. Several personal financial factors play a crucial role. Understanding these will help you prepare for your application for a new car loan Malaysia or a used car loan Malaysia.

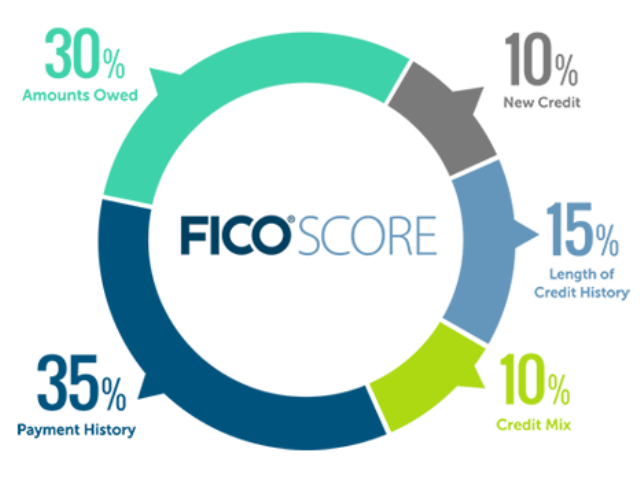

- Credit Score (CCRIS/CTOS): Your credit history is paramount. Banks assess your ability to manage debt based on your past repayment behavior. A good credit score (reflected in reports like CCRIS from Bank Negara Malaysia and CTOS) indicates low risk, potentially leading to better interest rates and easier approval.

- Income Stability: Lenders look for consistent and sufficient income to ensure you can meet your monthly obligations. Salaried employees with stable employment generally have an advantage. Freelancers or business owners might need to provide more extensive proof of income over a longer period.

- Debt-to-Income Ratio (DSR): This ratio compares your total monthly debt payments to your gross monthly income. Banks have specific DSR thresholds. If your DSR is too high, it signals that you might be over-leveraged, reducing your chances of approval.

- Employment Type & Duration: Permanent employees with a long tenure at a company are often seen as more stable borrowers than those in contract roles or new to their jobs.

- Vehicle Type: While not a personal factor, the type of car also influences the loan. New cars typically attract lower interest rates compared to used cars due to lower perceived risk and depreciation. Luxury or imported cars might also have different lending criteria.

Understanding these factors is key to improving your loan eligibility Malaysia and securing the most competitive Malaysia car loan interest rate.

Choosing the Best Car Loan in Malaysia: Tips and Strategies

Finding the best car loan Malaysia requires a bit of research and negotiation. Don’t just settle for the first offer you receive.

- Shop Around for Rates: Different banks and financial institutions offer varying interest rates and packages. Don’t limit yourself to the bank your car dealer recommends. Compare offers from at least three different lenders.

- Understand the Fine Print: Always read the terms and conditions carefully. Look out for any hidden fees, early settlement penalties, or specific clauses that might impact you later.

- Consider Your Down Payment: As discussed, a higher down payment can significantly reduce your total interest paid. If possible, save up for a larger initial payment.

- Negotiate with Dealers: Car dealers often have partnerships with specific banks and may offer competitive rates or promotional packages. However, always cross-check these offers with what you can get directly from other banks.

- Check Your Credit Score: Before applying, obtain your CCRIS report from Bank Negara Malaysia or a CTOS report. This allows you to identify any discrepancies and address them, improving your standing with lenders. For more detailed insights, you might want to check out our article on .

Advantages of Using a Car Loan Calculator Malaysia

The benefits of utilizing a Car Loan Calculator Malaysia extend far beyond just knowing your monthly payment.

- Financial Planning & Budgeting: It helps you understand the true financial commitment before you even step into a showroom. This allows for realistic budgeting and ensures your car purchase aligns with your overall financial goals.

- Comparing Offers Effectively: With multiple loan offers, the calculator allows you to input each bank’s specific interest rate and tenure to compare the actual monthly payments and total costs side-by-side. This empowers you to pick the most economical option.

- Scenario Planning: Want to see the impact of a larger down payment? Or a shorter loan tenure? The calculator lets you play around with different scenarios, helping you find the sweet spot between affordability and cost-efficiency.

- Avoiding Financial Surprises: By revealing the total interest payable, the calculator prevents you from being caught off guard by the overall cost of borrowing. It fosters transparency in your decision-making.

- Empowerment: Ultimately, using this tool empowers you with knowledge, turning what can seem like a complex financial decision into a manageable and transparent process.

Common Mistakes to Avoid When Taking a Car Loan

Even with all the tools at your disposal, certain pitfalls can derail your car buying experience. Based on my experience, these are some common mistakes to avoid:

- Not Using a Calculator: Relying solely on the dealer’s verbal quotes or rough estimates can lead to misunderstandings and financial strain. Always verify figures with your own car loan repayment calculator.

- Focusing Only on Monthly Payments: It’s easy to get fixated on a low monthly car payment Malaysia. However, a low monthly payment often comes with a longer tenure and significantly higher total interest paid. Always consider the total cost of the loan.

- Ignoring Total Cost of Ownership: As discussed earlier, neglecting insurance, road tax, maintenance, and fuel costs can lead to financial distress. Your budget must encompass all these elements. You can find more information on this in our article on .

- Not Checking Your Credit Score: Applying for a loan without knowing your credit standing can lead to rejections or unfavorable rates. Be proactive in understanding and improving your credit health.

- Skipping the Fine Print: Loan agreements are legal documents. Glossing over the terms and conditions can lead to unexpected penalties or obligations down the line. Take your time and understand every clause.

The Future of Car Loans in Malaysia: A Brief Outlook

The landscape of automotive financing in Malaysia is continually evolving. We’re seeing increasing digitalization, with more banks offering online application processes and digital calculators. There’s also a growing awareness among consumers regarding responsible borrowing. As technology advances, we might see more personalized loan products, AI-driven credit assessments, and potentially, greater transparency in interest rate structures.

Ultimately, the core principles of smart borrowing and utilizing tools like the Car Loan Calculator Malaysia will remain crucial. Staying informed about market trends and financial regulations, such as those provided by , will always benefit prospective car owners.

Conclusion: Drive Smart, Finance Smarter

The journey to car ownership in Malaysia is exciting, but it demands careful financial planning. The Car Loan Calculator Malaysia is not just a tool; it’s your financial compass, guiding you through the intricacies of hire purchase agreements. By understanding its components, knowing how to use it effectively, and considering all associated costs, you empower yourself to make intelligent decisions.

Don’t let the allure of a new car overshadow the importance of sound financial planning. Use this knowledge to your advantage, compare diligently, budget comprehensively, and ensure your car loan is a stepping stone to financial freedom, not a burden. Start planning your car purchase today with confidence and clarity!