Your Ultimate Guide to Mastering Your Car Purchase with a Car Loan Price Calculator

Your Ultimate Guide to Mastering Your Car Purchase with a Car Loan Price Calculator Carloan.Guidemechanic.com

Buying a car is an exciting milestone, whether it’s your first set of wheels or an upgrade to your dream vehicle. However, the excitement can quickly turn to anxiety when faced with the complexities of car financing. Understanding how much you can truly afford and what your monthly payments will look like is crucial for a stress-free purchase. This is precisely where a powerful tool, the Car Loan Price Calculator, becomes your indispensable ally.

As an expert blogger and professional in the automotive finance space, I’ve seen countless individuals make informed decisions, and unfortunately, some costly mistakes. My goal with this comprehensive guide is to equip you with everything you need to know about using a car loan calculator effectively. We’ll dive deep into its functionalities, reveal advanced strategies, and share crucial tips to ensure you drive away with confidence, not buyer’s remorse.

Your Ultimate Guide to Mastering Your Car Purchase with a Car Loan Price Calculator

Why a Car Loan Price Calculator is Your Best Friend in the Buying Journey

Before you even step foot in a dealership, your auto loan calculator should be your first stop. It’s more than just a simple math tool; it’s a strategic planner that empowers you to take control of your car buying experience. Think of it as your personal financial consultant for your next vehicle.

Budgeting Power: Setting Realistic Expectations

One of the most significant benefits of using a car finance calculator is its ability to help you establish a realistic budget. It allows you to input various scenarios and immediately see the impact on your potential monthly payments. This clarity prevents you from falling in love with a car that’s ultimately out of your financial reach.

Based on my experience, many buyers overestimate what they can comfortably afford each month. A calculator brings you back to reality, ensuring your car payment doesn’t strain your overall financial health. It’s about finding that sweet spot where desire meets affordability.

Comparing Offers: Making Apples-to-Apples Assessments

When you start shopping for loans, you’ll encounter different interest rates, terms, and lender fees. Trying to compare these manually can be confusing and lead to miscalculations. A car loan price calculator simplifies this process immensely.

You can plug in details from multiple loan offers and quickly see which one provides the best overall value. This feature is invaluable for making informed decisions and ensuring you secure the most favorable terms available. It truly levels the playing field between you and the lenders.

Understanding Total Cost: Beyond the Monthly Payment

Focusing solely on the monthly payment is a common pitfall. While important, it doesn’t tell the whole story. An effective car loan calculator will often show you the total amount you’ll pay over the life of the loan, including all interest charges.

This comprehensive view helps you understand the true cost of borrowing. Sometimes, a lower monthly payment over a longer term can mean paying significantly more in interest overall. This insight is critical for long-term financial planning.

Avoiding Surprises: Preparing for All Contingencies

Unexpected costs can derail a car purchase. Using a calculator allows you to factor in potential variables like different down payment amounts or varying interest rates based on your credit score. This preparation reduces the likelihood of unwelcome surprises later on.

By experimenting with different scenarios, you build a robust financial plan for your car. This proactive approach ensures you’re ready for whatever the financing process throws your way. It’s about being prepared, not just hopeful.

How a Car Loan Price Calculator Works: The Core Elements

To harness the full power of a car loan calculator, you need to understand the key variables it uses. Each piece of information plays a vital role in determining your final monthly payment and the total cost of the loan.

Purchase Price: The Starting Point

This is the negotiated price of the car you intend to buy. It’s crucial to use the actual selling price, not just the sticker price, as negotiations can significantly alter this figure. Remember, every dollar off the purchase price reduces your loan amount.

A lower purchase price directly translates to a smaller loan, which in turn means lower monthly payments and less interest paid over time. This highlights the importance of effective negotiation at the dealership.

Down Payment: Your Upfront Investment

The down payment is the amount of cash you pay upfront towards the car’s purchase price. A larger down payment reduces the amount you need to borrow, which is always a smart financial move. It immediately decreases your monthly payments.

Furthermore, a substantial down payment can sometimes qualify you for better interest rates, as it signals less risk to the lender. It’s a powerful tool in your financial arsenal, significantly impacting the loan’s overall cost.

Trade-In Value: Leveraging Your Current Vehicle

If you’re trading in your old car, its value acts similarly to a down payment. This amount is subtracted from the purchase price of your new vehicle, reducing the loan principal. Be sure to get an accurate estimate of your trade-in value before visiting the dealership.

Websites like Kelley Blue Book or Edmunds can provide excellent estimates, giving you leverage in negotiations. Incorporating this value into your auto loan calculator provides a more accurate picture of your true borrowing needs.

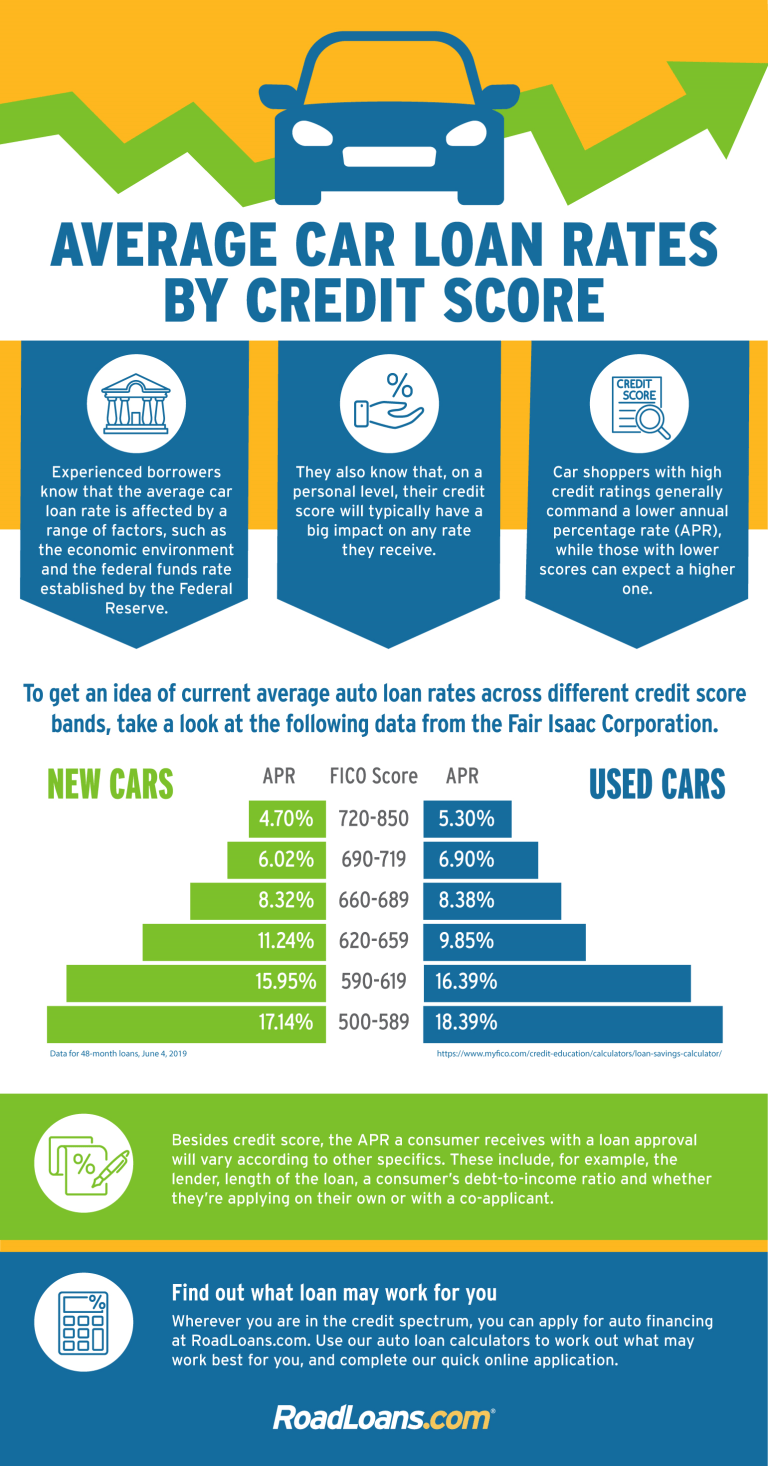

Interest Rate (APR): The Cost of Borrowing

The interest rate, often expressed as an Annual Percentage Rate (APR), is essentially the cost you pay to borrow money. It’s a percentage of the loan amount that lenders charge for their services. This is a critical factor influencing your monthly payment and the total amount you repay.

A lower APR means less interest paid over the life of the loan, saving you significant money. Your credit score is the primary determinant of the interest rate you’ll be offered, so monitoring it is always a good practice.

Loan Term: The Repayment Period

The loan term is the length of time, usually in months, over which you agree to repay the loan. Common terms range from 36 to 84 months. A shorter loan term means higher monthly payments but less interest paid overall.

Conversely, a longer loan term results in lower monthly payments but accrues more interest over time. It’s a delicate balance between affordability and the total cost of the loan that your car loan price calculator helps you navigate.

Sales Tax & Fees: The Hidden Extras

Don’t forget about sales tax, registration fees, and other administrative charges that are added to the car’s price. These can vary significantly by state and locality. While some calculators allow you to input these directly, others might require you to add them to the purchase price manually.

These additional costs can quickly add thousands of dollars to your total financed amount. Always account for them to avoid underestimating your true financial commitment.

Step-by-Step: Maximizing Your Car Loan Calculator Experience

Using a car loan calculator isn’t just about plugging in numbers once. It’s an iterative process that helps you refine your budget and strategy.

1. Gather Your Information

Before you start, collect all the necessary data:

- Estimated Car Price: Start with a target price range for the type of car you want.

- Anticipated Down Payment: How much cash can you comfortably put down?

- Estimated Trade-In Value: If applicable, get a rough estimate for your current vehicle.

- Potential Interest Rate: If you’ve been pre-qualified or know your credit score, you can estimate an APR. If not, use an average rate for your credit tier as a starting point.

- Desired Loan Term: Do you prefer shorter terms for less interest or longer terms for lower payments?

Having these figures ready will make the calculator experience much smoother and more productive.

2. Experiment with Variables

This is where the magic happens. Start by inputting your initial estimates. Then, begin to adjust each variable one at a time to see its impact.

- What if you increase your down payment by $1,000?

- What if you extend the loan term by 12 months?

- What if you find a car that’s $2,000 cheaper?

Each adjustment will instantly show you how your monthly payment changes.

3. Analyze the Results

Don’t just look at the monthly payment. Pay close attention to the total interest paid over the life of the loan. This often overlooked figure reveals the true cost of borrowing and helps you compare different scenarios more effectively.

Consider if the total cost aligns with your long-term financial goals. Sometimes, a slightly higher monthly payment for a shorter term can save you thousands in interest.

4. Run Multiple Scenarios

Never settle for just one calculation. Run scenarios for different car prices, varying down payments, and a range of interest rates (e.g., what if your credit score gets you a slightly better or worse rate?). This comprehensive approach prepares you for various outcomes during your car search and negotiation.

Pro tips from us: Create a small spreadsheet to track these different scenarios. It will make comparing options much easier when you’re ready to make a decision.

Beyond the Basics: Advanced Strategies and Pro Tips

Leveraging a car loan price calculator effectively means understanding the nuances that can significantly impact your financial outcome.

The Power of the Down Payment

We’ve touched on it, but let’s emphasize: a larger down payment is almost always beneficial. It reduces your principal, lowers your monthly payment, and often means you pay less in total interest. Based on my experience, a down payment of at least 20% can make a significant difference in securing better loan terms and avoiding being "upside down" on your loan (owing more than the car is worth).

Even if it means saving a little longer, the financial benefits often outweigh the wait.

Short vs. Long Loan Terms: What’s Best for You?

This is a common dilemma.

- Shorter terms (e.g., 36-48 months): Higher monthly payments, but you pay off the car faster and incur significantly less interest. You build equity quicker.

- Longer terms (e.g., 72-84 months): Lower monthly payments, making the car seem more "affordable" initially. However, you pay much more in interest over time, and the car’s value depreciates faster than you pay it off, increasing the risk of negative equity.

Use your car loan calculator to compare these scenarios side-by-side. See if you can comfortably afford the higher payment of a shorter term to save thousands in the long run.

Understanding the Impact of Interest Rates

Even a half-point difference in your APR can translate into hundreds or thousands of dollars over the life of a loan. This underscores the importance of shopping around for the best interest rate. Don’t just accept the first offer from the dealership.

Get pre-qualified with multiple lenders (banks, credit unions, online lenders) before you visit the dealership. This gives you negotiating power and ensures you secure the most competitive rate available to you.

Considering Additional Costs (Insurance, Maintenance)

While not directly part of the loan calculation, these are crucial components of your total car ownership cost. A higher car payment might leave less room in your budget for rising insurance premiums or unexpected maintenance.

Always factor these into your overall monthly budget alongside your car payment. A good rule of thumb is to allocate an additional 10-15% of your car payment for these ancillary costs.

Pre-Qualification vs. Pre-Approval

Understand the difference:

- Pre-qualification: A soft credit check that gives you an estimate of what you might qualify for. It doesn’t impact your credit score.

- Pre-approval: A hard credit check that gives you a firm offer of a loan amount and interest rate. This is the "money in hand" you can take to the dealership.

Aim for pre-approval from at least one external lender before negotiating with a dealership. This provides a baseline against which you can compare dealer financing offers.

Common Mistakes to Avoid When Using a Car Loan Calculator

Even with the best tools, missteps can happen. Being aware of these common errors can save you from financial headaches.

Forgetting Sales Tax and Fees

As mentioned, these can significantly inflate your total loan amount. Common mistakes to avoid are neglecting to add sales tax, registration fees, and document fees into your calculation. Many online calculators have a field for this, but if not, remember to manually add it to the car’s purchase price.

Always ask the dealer for an "out-the-door" price that includes all taxes and fees to get the most accurate figure for your calculator.

Ignoring the Total Cost of the Loan

Fixating solely on the monthly payment can lead to choosing a longer loan term with a lower monthly outlay, but a much higher total cost due to increased interest. This is a classic trap. Always look at the "Total Amount Repaid" figure provided by your car loan price calculator.

Prioritize minimizing the total cost of the loan, not just the monthly payment, if your budget allows.

Not Factoring in Other Car Expenses

Your car payment is just one piece of the puzzle. Insurance, fuel, maintenance, and potential repair costs all add up. A common mistake is to stretch your car payment to its maximum without considering these other essential expenses.

Based on my experience, buyers who consider these costs upfront are far less likely to feel financially strained down the road.

Only Focusing on the Monthly Payment

While important for budgeting, the monthly payment alone doesn’t reflect the overall value or cost-effectiveness of a loan. A low monthly payment might mean a longer loan term and a much higher total interest paid. This can lead to significant overspending in the long run.

Use the calculator to find a balance between an affordable monthly payment and a reasonable total loan cost.

Not Shopping Around for Rates

Relying on a single lender’s interest rate, especially the one offered by the dealership, is a common pitfall. Dealerships often mark up interest rates. Always use your car loan calculator to compare rates from at least 3-4 different lenders.

This proactive approach ensures you’re getting the best possible deal for your financial profile. For a deeper dive into understanding car loan interest rates, check out our article on .

Choosing the Right Car Loan Price Calculator

Not all auto loan calculators are created equal. When selecting one, consider these factors:

Accuracy and Reliability

Ensure the calculator comes from a reputable financial institution, an established automotive site, or a trusted consumer resource. These sources are more likely to provide accurate calculations and up-to-date information.

Avoid generic, unbranded calculators that might lack precision or omit crucial fields.

Ease of Use

A good calculator should be intuitive and user-friendly. You should be able to easily input your variables and understand the results without a steep learning curve. Look for clear labeling and straightforward navigation.

A cluttered or confusing interface can lead to errors and frustration.

Additional Features

Some calculators offer advanced features like amortization schedules (showing how much principal and interest you pay each month over the loan term), the ability to include sales tax and fees, or comparisons of different loan scenarios. These extra features can provide even greater insight.

The more comprehensive the calculator, the better equipped you’ll be to make an informed decision.

The Ultimate Goal: Financial Confidence and a Smart Purchase

Ultimately, the goal of using a car loan price calculator is to empower you. It transforms the often-intimidating process of car financing into a manageable, transparent exercise. By understanding the numbers before you commit, you gain confidence and the ability to negotiate from a position of strength.

You’ll know exactly what you can afford, what a good interest rate looks like for you, and how different loan terms impact your financial future. This knowledge is your best defense against overpaying and ensures you make a smart, sustainable purchase.

Conclusion

The journey to owning a new car should be exciting and rewarding, not stressful. By embracing the power of a Car Loan Price Calculator, you equip yourself with the financial foresight needed to make an informed and confident decision. It’s not just about finding a monthly payment; it’s about understanding the entire financial landscape of your car purchase.

So, before you fall in love with that shiny new vehicle, spend some quality time with an auto loan calculator. Experiment, analyze, and plan. Your wallet, and your peace of mind, will thank you for it. Start your calculations today and drive away with the car you love, on terms you understand and can comfortably afford. For general financial planning advice, a trusted resource like the Consumer Financial Protection Bureau can be incredibly helpful.