Your Ultimate Guide to Navigating Car Money Loans: Drive Smarter, Not Harder

Your Ultimate Guide to Navigating Car Money Loans: Drive Smarter, Not Harder Carloan.Guidemechanic.com

Buying a car is a significant milestone for many, offering unparalleled freedom and convenience. However, the reality for most people is that purchasing a vehicle outright requires a substantial financial outlay. This is where a car money loan comes into play, transforming an aspirational purchase into an achievable goal. Understanding the intricacies of an auto loan is crucial for making informed decisions that align with your financial well-being.

This comprehensive guide will demystify everything you need to know about car money loans, from the application process to smart management strategies. Our goal is to equip you with the knowledge to secure the best possible financing, ensuring you drive away happy and financially secure. Let’s dive in and navigate the world of vehicle finance together.

Your Ultimate Guide to Navigating Car Money Loans: Drive Smarter, Not Harder

What Exactly is a Car Money Loan?

At its core, a car money loan is a sum of money borrowed from a financial institution or lender specifically for the purpose of purchasing a vehicle. This type of loan is typically a secured loan, meaning the car itself acts as collateral. Should you fail to make your payments, the lender has the right to repossess the vehicle to recover their losses.

The concept is straightforward: a lender provides you with the funds to buy a car, and you agree to repay that amount, plus interest, over a predetermined period. This repayment is usually structured into fixed monthly installments. The interest charged is essentially the cost of borrowing the money, and it’s a key factor influencing your total expenditure.

Understanding the mechanics of a car loan is fundamental. It involves three primary parties: the borrower (you), the lender (bank, credit union, dealership finance department), and the vehicle itself, which serves as security for the loan. The terms of this agreement – including the loan amount, interest rate, and repayment schedule – are all outlined in a legally binding contract.

Why Do People Opt for a Car Money Loan?

While it might seem ideal to pay for a car in cash, the practicalities of modern life often make a car money loan the most viable option. There are several compelling reasons why individuals choose to finance their vehicle purchase.

Firstly, accessibility to a vehicle is paramount for many. A car provides transportation for work, family responsibilities, and personal leisure. For most, having tens of thousands of dollars readily available to buy a car outright isn’t realistic. A loan makes vehicle ownership attainable, allowing you to get on the road when you need to.

Secondly, opting for an auto loan can be a strategic way to preserve your cash for other important financial goals or emergencies. Tying up a significant portion of your savings in a depreciating asset like a car might not always be the wisest financial move. Financing allows you to maintain liquidity, keeping your emergency fund intact and available for unforeseen circumstances.

Another significant benefit, often overlooked, is the opportunity to build or improve your credit history. Successfully managing and repaying a car loan demonstrates financial responsibility to credit bureaus. This positive payment history can significantly boost your credit score over time, opening doors to better rates on future loans, mortgages, and credit cards. It’s a stepping stone to a stronger financial profile.

Finally, the convenience offered by various lending options makes the process relatively smooth. From online applications to in-dealership financing, lenders have streamlined the process, making it easier than ever to secure the funds needed for your new ride. This convenience, combined with the other benefits, makes vehicle finance a popular choice.

The Car Money Loan Application Process: A Step-by-Step Guide

Securing a car money loan doesn’t have to be a daunting task. By breaking down the process into manageable steps, you can approach it with confidence and clarity. Based on my experience, a structured approach is always best.

Step 1: Assess Your Financial Health

Before you even start looking at cars, it’s critical to understand your own financial standing. This foundational step will dictate what kind of loan you can qualify for and at what terms.

Your credit score is a major determinant of your interest rate. Lenders use it to gauge your creditworthiness – essentially, how likely you are to repay the loan. A higher score typically leads to lower interest rates, saving you a substantial amount over the life of the loan. Obtain your credit report from all three major bureaus (Equifax, Experian, TransUnion) and review it for accuracy. Correcting any errors can significantly improve your score.

Beyond your credit score, lenders also look at your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income to cover new loan payments, making you a less risky borrower. Aim for a DTI of 36% or less, though some lenders may approve higher.

Finally, budgeting realistically is paramount. Determine how much you can comfortably afford to pay each month for a car loan, including insurance, fuel, and maintenance. Don’t just consider the monthly payment; think about the total cost of ownership. Overextending yourself financially can lead to stress and potential default.

Step 2: Determine Your Needs & Research Lenders

Once you know what you can afford, it’s time to narrow down your vehicle choice and explore your lending options. This proactive research can save you money and headaches down the line.

Decide whether a new car loan or a used car loan is right for you. New cars typically come with lower interest rates but depreciate quickly. Used cars are more affordable but might have higher interest rates and potential maintenance costs. Your loan amount will directly correlate with the vehicle’s price, so having a clear target in mind is essential.

Next, research different lender types. You have several options:

- Banks: Often offer competitive rates and a wide range of loan products.

- Credit Unions: Known for member-friendly rates and personalized service, often offering better deals than traditional banks.

- Dealerships: Provide convenience by offering in-house financing or working with multiple lenders. However, their rates might not always be the most competitive.

- Online Lenders: Can offer quick approvals and competitive rates, especially for those with good credit.

Comparing offers from various lenders is a pro tip from us. Don’t just settle for the first offer you receive; shop around to ensure you’re getting the best possible terms for your vehicle finance.

Step 3: Gather Necessary Documents

Getting your paperwork in order beforehand streamlines the application process. Lenders require specific documents to verify your identity, income, and residence.

You will typically need:

- Proof of Identity: Government-issued ID (driver’s license, passport).

- Proof of Income: Pay stubs, W-2s, tax returns, or bank statements if self-employed.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Proof of Insurance: You’ll need to show you can insure the vehicle before the loan is finalized.

- Vehicle Information: If you’ve already chosen a car, details like the VIN, make, model, and mileage will be required.

Having these documents ready will prevent delays and show the lender you are a serious and organized applicant for a car money loan.

Step 4: Apply for Pre-Approval

One of the most valuable steps in the car loan process is applying for pre-approval. This crucial step empowers you as a buyer.

Pre-approval means a lender has reviewed your financial information and provisionally agreed to lend you a certain amount of money, at a specific interest rate, before you’ve even picked out a car. It gives you a clear budget and allows you to walk into a dealership with the confidence of a cash buyer. This leverage can be incredibly useful during negotiations.

It’s important to understand the difference between a soft inquiry and a hard inquiry. Pre-approvals often start with a soft inquiry, which doesn’t affect your credit score. Once you formally apply for the loan, a hard inquiry will be made, which might slightly ding your score for a short period. However, multiple hard inquiries for car loans within a short timeframe (typically 14-45 days) are often grouped as a single inquiry by credit bureaus, so shopping around for rates won’t hurt your score significantly if done efficiently.

Step 5: Compare Offers & Choose Wisely

With pre-approval offers in hand, it’s time to critically evaluate each one. This is where attention to detail pays off.

Don’t just look at the monthly payment. Focus on the Annual Percentage Rate (APR), which represents the true annual cost of borrowing, including interest and any fees. It’s a more accurate measure than just the interest rate alone. A lower APR means less money spent over the life of the loan.

Consider the loan term (length of the loan). Shorter terms typically mean higher monthly payments but less interest paid overall. Longer terms result in lower monthly payments but accumulate more interest over time, making the car more expensive in the long run. Find a balance that fits your budget and financial goals.

Pro tips from us: Always scrutinize the fine print for hidden fees. Look for origination fees, documentation fees, or prepayment penalties. These can add to your total cost. A transparent lender will clearly outline all costs associated with your car money loan.

Step 6: Finalize the Loan & Purchase Your Car

Once you’ve selected the best car loan offer, the final steps involve understanding and signing the contract, then taking ownership of your vehicle.

Carefully read the entire loan contract before signing. Ensure all the terms discussed are accurately reflected, including the loan amount, APR, monthly payment, and loan term. If anything is unclear, ask questions until you fully understand every clause. This is a legally binding agreement, so thoroughness is key.

Finally, remember that insurance requirements are mandatory. Lenders will typically require you to have comprehensive and collision coverage on your financed vehicle to protect their collateral. Ensure you have the appropriate coverage in place before driving off the lot.

Key Factors Influencing Your Car Money Loan Terms and Rates

Several variables play a significant role in determining the terms and interest rates you’re offered for a car money loan. Understanding these factors can help you position yourself for the best possible deal.

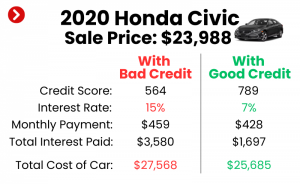

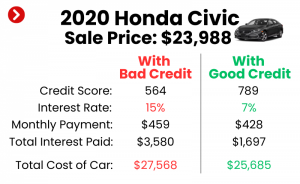

Your credit score is arguably the most impactful factor. A high credit score (generally 700+) signals to lenders that you are a reliable borrower, leading to the lowest interest rates. Conversely, a lower score will result in higher rates to compensate the lender for increased risk.

The size of your down payment also matters. A larger down payment reduces the amount you need to borrow, which can lead to a lower monthly payment and less interest paid over time. It also signals financial stability to lenders, potentially improving your loan terms.

The loan term, or repayment period, directly influences your monthly payment and the total interest paid. Shorter terms (e.g., 36 or 48 months) mean higher monthly payments but less interest. Longer terms (e.g., 60 or 72 months) offer lower monthly payments but result in more interest accumulating over the life of the auto loan.

The interest rate (APR) is the cost of borrowing the money, expressed as a percentage. This is heavily influenced by your credit score, the loan term, and the current economic environment. Always aim for the lowest APR possible.

Your debt-to-income (DTI) ratio indicates your ability to take on new debt. Lenders want to see that you have enough disposable income to comfortably make your car payments. A lower DTI generally means better loan prospects.

The vehicle’s age and type also play a role. New cars often qualify for lower interest rates and longer terms due to their higher value and perceived reliability. Used cars might have slightly higher rates due to their depreciating value and potential for more maintenance issues.

Finally, the lender type can influence rates. As mentioned, credit unions often have very competitive rates, while dealership financing can sometimes be higher, though they may offer promotional rates. Based on my experience, comparing offers from at least three different lender types (bank, credit union, online lender) is crucial to ensure you’re not leaving money on the table.

Common Car Money Loan Myths Debunked

The world of car money loans is rife with misconceptions. Dispelling these myths can empower you to make smarter financial decisions.

Myth 1: You need perfect credit to get a car loan. While excellent credit will secure the best rates, it’s absolutely not a prerequisite for obtaining a vehicle finance loan. Lenders offer loans to individuals across the credit spectrum, including those with fair or even poor credit. However, expect higher interest rates if your score is lower.

Myth 2: Dealerships always offer the best rates. This is a common fallacy. While dealerships provide convenience and sometimes special manufacturer incentives, they often act as intermediaries, marking up rates from their lending partners. Pro tip: Always get pre-approved from an independent lender (bank, credit union, online lender) before visiting the dealership. This way, you have a benchmark to compare against.

Myth 3: Longer terms always mean lower costs. While a longer loan term (e.g., 72 or 84 months) will result in a lower monthly payment, it almost always means you’ll pay significantly more in total interest over the life of the loan. This is because interest accrues over a longer period. You also risk owing more than the car is worth (being "upside down") as depreciation outpaces your payments.

Myth 4: Pre-approval isn’t necessary. As discussed earlier, pre-approval is a powerful tool. It gives you a clear budget, strengthens your negotiating position, and allows you to focus on finding the right car without the pressure of financing decisions at the dealership. Skipping this step means potentially accepting less favorable terms out of convenience.

Navigating Car Money Loans with Less-Than-Perfect Credit

Having a less-than-stellar credit score doesn’t mean you can’t get a car money loan, but it does mean you’ll need to be more strategic. Common mistakes to avoid are rushing into the first offer you receive or not understanding the terms.

First, understand your credit score and report thoroughly. Identify any inaccuracies and work to resolve them. Knowing your score allows you to set realistic expectations for interest rates.

Consider making a larger down payment. A substantial down payment reduces the risk for the lender, as they are financing a smaller portion of the vehicle’s value. This can make them more willing to approve your loan, even with a lower credit score, and might lead to a slightly better interest rate.

Another effective strategy is to look for a co-signer. A co-signer with good credit essentially guarantees the loan if you default. This added security significantly reduces the lender’s risk, making it easier for you to get approved and potentially secure a lower interest rate. Ensure both parties understand the full implications of co-signing.

You might also need to explore subprime lenders. These lenders specialize in working with individuals who have poor credit. While they offer a solution, be prepared for significantly higher interest rates and potentially less flexible terms. Always compare offers carefully and understand all fees involved.

Ultimately, focus on improving your credit score over time. Making consistent, on-time payments on your car loan (once secured) is an excellent way to rebuild your credit. This can then open doors to refinancing opportunities later on, allowing you to secure a lower rate. For more detailed insights on improving your credit, you might find our article on Understanding Your Credit Score for Auto Loans helpful. (Internal Link 1)

Refinancing Your Car Money Loan: When and Why?

Refinancing your car money loan means replacing your existing loan with a new one, often with different terms and a new interest rate. It’s a strategic move that can save you money and improve your financial situation.

What is refinancing? Essentially, you apply for a new loan to pay off your current one. The new loan typically comes with a lower interest rate, a different monthly payment, or a revised loan term.

You should consider refinancing if:

- Interest rates have dropped since you originally took out your loan.

- Your credit score has significantly improved. A better score qualifies you for better rates.

- You want to lower your monthly payments by extending the loan term (though this means more interest overall).

- You want to reduce the total interest paid by shortening the loan term (though this means higher monthly payments).

- You want to remove a co-signer from the loan.

The benefits of refinancing can be substantial, including lower monthly payments, reduced total interest costs, or the ability to pay off your car faster. The process is similar to applying for an initial loan: you shop around for new lenders, compare offers, and once approved, the new lender pays off your old loan.

Pro Tips for Smart Car Money Loan Management

Once you’ve secured your car money loan, smart management is key to minimizing costs and maintaining good financial health.

Firstly, always budget realistically. Ensure your monthly car payment, along with insurance, fuel, and maintenance, fits comfortably within your overall budget. Don’t let your car payment strain your finances.

Consider making extra payments whenever possible. Even small additional payments can significantly reduce the total interest you pay and shorten your loan term. You can often apply extra payments directly to the principal balance, accelerating your payoff.

Set up automatic payments from your bank account. This ensures you never miss a payment, which protects your credit score and helps you avoid late fees. Many lenders even offer a slight interest rate discount for setting up auto-pay.

Understand your payoff date and monitor your loan balance regularly. Knowing exactly when your loan will be paid off can be motivating and helps you plan future financial goals.

Finally, always keep your car insurance current and adequate. Lenders require comprehensive and collision coverage. Lapsing on your insurance not only puts you at risk but can also trigger penalties from your lender or even force-placed insurance at a higher cost.

For more advice on vehicle purchasing, including negotiation tactics that can impact your loan amount, check out our guide on Tips for Negotiating Your Car Purchase. (Internal Link 2)

The Future of Car Money Loans: Trends to Watch

The landscape of car money loans is continuously evolving, driven by technological advancements and changing consumer preferences. Staying abreast of these trends can offer a glimpse into future opportunities.

Online lending platforms are rapidly gaining traction, offering streamlined application processes, quick approvals, and competitive rates. Their convenience and efficiency are appealing to a tech-savvy generation.

The rise of Electric Vehicles (EVs) is also influencing financing. As EVs become more mainstream, expect to see specialized EV financing options, potentially with favorable terms due to government incentives or lower operational costs.

We’re also seeing a trend towards personalized loan offers. Lenders are leveraging data analytics to provide highly tailored loan products based on individual credit profiles, spending habits, and even driving behavior, offering a more customized vehicle finance experience.

For more insights into personal finance and smart borrowing, a trusted external source like the Consumer Financial Protection Bureau (CFPB) offers valuable resources and guidance: Consumer Financial Protection Bureau – Auto Loans. (External Link)

Conclusion: Drive Away with Confidence

Navigating the world of car money loans can seem complex, but with the right knowledge, it becomes an empowering journey. From understanding the basics of an auto loan to strategically managing your payments, every step you take to educate yourself contributes to a more secure financial future.

Remember to always assess your financial health, compare offers from multiple lenders, and meticulously review all loan documents. By taking a proactive and informed approach, you can secure a car money loan that not only gets you behind the wheel of your desired vehicle but also aligns perfectly with your long-term financial goals. Drive smarter, not harder, and enjoy the open road ahead!