Your Ultimate Guide to New Car Loan Pre-Approval: Drive Away with Confidence and Savings

Your Ultimate Guide to New Car Loan Pre-Approval: Drive Away with Confidence and Savings Carloan.Guidemechanic.com

Buying a new car is an exciting milestone, often filled with dreams of cruising down the open road in your perfect vehicle. However, the excitement can quickly turn into stress when you step onto the dealership lot and face the complex world of financing. This is where new car loan pre-approval becomes your ultimate secret weapon, transforming you from a hopeful buyer into a powerful, informed negotiator.

In this comprehensive guide, we’ll dive deep into everything you need to know about getting pre-approved for a new car loan. We’ll explain its immense benefits, walk you through the process, highlight common pitfalls to avoid, and equip you with the knowledge to secure the best possible financing for your next set of wheels. Our goal is to empower you to drive away not just with a new car, but with an incredible deal and complete peace of mind.

Your Ultimate Guide to New Car Loan Pre-Approval: Drive Away with Confidence and Savings

What Exactly is New Car Loan Pre-Approval?

At its core, new car loan pre-approval is a conditional commitment from a lender (like a bank, credit union, or online financier) to lend you a specific amount of money at a certain interest rate, even before you’ve picked out your car. It’s a formal assessment of your creditworthiness and financial health, providing you with a concrete offer that you can take to the dealership.

This isn’t just a casual estimate; it’s a firm offer, albeit with conditions. The lender evaluates your credit score, income, debt-to-income ratio, and other financial factors to determine how much they are willing to lend you. Once pre-approved, you’ll receive a letter or certificate outlining the loan amount, interest rate, and term (length of the loan).

It’s crucial to understand that pre-approval differs significantly from pre-qualification. Pre-qualification is a preliminary check, a soft inquiry that gives you an estimate without a firm offer. Pre-approval, on the other hand, involves a more thorough review and often a "hard inquiry" on your credit report, leading to a much more reliable loan offer.

Why is New Car Loan Pre-Approval Your Secret Weapon? Unlocking Unbeatable Advantages

Securing a new car loan pre-approval before you even visit a dealership offers a multitude of advantages that can save you time, money, and stress. Based on my experience in the automotive and finance industries, this single step is one of the most impactful decisions a car buyer can make.

1. Become a Cash Buyer, Not Just a Borrower

Imagine walking into a dealership with a pre-approval letter in hand. You’re no longer just someone looking for a loan; you effectively become a cash buyer in the eyes of the salesperson. You already have your financing sorted, which means the dealership’s primary focus shifts to selling you a car, rather than simultaneously selling you a car and financing.

This subtle shift in dynamic is incredibly powerful. You can negotiate the car’s price more aggressively because financing isn’t part of the bargaining chip.

2. Set a Clear, Realistic Budget

One of the biggest benefits of new car loan pre-approval is gaining a precise understanding of your budget. Your pre-approval letter clearly states the maximum amount you can borrow. This empowers you to shop within your financial limits, preventing you from falling in love with a car you simply can’t afford.

Knowing your spending ceiling upfront helps you focus your search on vehicles that fit your approved loan amount, making the car selection process far more efficient and less frustrating. You’ll avoid the disappointment of being turned down for a car you thought was within reach.

3. Streamline the Car Buying Process

Nobody enjoys spending hours at the dealership, waiting for finance managers to crunch numbers and present loan options. With a new car loan pre-approval, you significantly cut down on this waiting time. You already have a strong offer, allowing you to bypass much of the back-and-forth typically associated with dealership financing.

This means less time filling out paperwork at the dealership and more time enjoying your new ride. Pro tips from us: The less time you spend in the finance office, the less likely you are to be upsold on expensive add-ons you don’t need.

4. Compare Offers and Secure the Best Rates

When you get pre-approved, you’re not obligated to accept the first offer. This process encourages you to shop around and compare rates from various lenders. By doing so, you can identify the most competitive interest rate and favorable terms available to you.

Once you have a solid pre-approval offer, you can even use it as leverage. The dealership’s finance department might try to beat your pre-approved rate to earn your business, potentially saving you even more money over the life of the loan.

5. Avoid High-Pressure Sales Tactics

Dealerships often make a significant portion of their profit from financing arrangements. Without a pre-approval, you’re walking into their territory with little defense against their financing options, which may not always be in your best interest. They might present you with higher interest rates or unfavorable terms.

Your pre-approval acts as a shield, allowing you to confidently decline less favorable offers from the dealership. You control the financing narrative, ensuring you get a deal that aligns with your financial goals, not just the dealership’s profit margins.

The Step-by-Step Process to Getting New Car Loan Pre-Approved

Getting new car loan pre-approval might seem daunting, but it’s a straightforward process when broken down. Follow these steps to set yourself up for success and secure a great financing deal.

1. Assess Your Credit Health

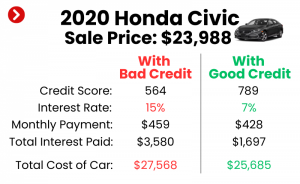

Before applying anywhere, it’s vital to know where you stand financially. Your credit score is the single most important factor lenders consider when determining your interest rate and loan amount. A higher credit score generally translates to lower interest rates.

Obtain a copy of your credit report from all three major bureaus (Experian, Equifax, and TransUnion) and review them carefully. Look for any errors or inaccuracies that could be dragging down your score. If you find any, dispute them immediately. For a detailed walkthrough on how to do this and improve your score, check out (Internal Link Placeholder: Link to an article about credit score improvement).

2. Determine Your Realistic Budget

While pre-approval gives you a maximum loan amount, you still need to decide how much you are comfortable spending monthly. Factor in not just the car payment, but also insurance, fuel, maintenance, and registration fees. Remember, the total cost of ownership extends far beyond the sticker price.

Consider your down payment as well. A larger down payment reduces the amount you need to borrow, which can lead to lower monthly payments and less interest paid over the life of the loan. It also shows lenders you are a less risky borrower.

3. Gather Your Essential Documents

Lenders will require certain documents to verify your identity, income, and residency. Having these ready beforehand will expedite the application process. Common documents include:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2s, or tax returns (if self-employed).

- Proof of Residency: Utility bill, lease agreement, or mortgage statement.

- Social Security Number: For credit checks.

- Employment Information: Name and contact for your employer.

Having these documents organized and readily available will make the application seamless.

4. Shop Around for Lenders

This is a critical step many people overlook. Don’t just apply to one bank! Different lenders have varying criteria, interest rates, and loan products. To find the best new car loan pre-approval offer, you should apply to several types of institutions:

- Banks: Large national banks and smaller local banks.

- Credit Unions: Often offer competitive rates and personalized service, especially for members.

- Online Lenders: Many reputable online platforms specialize in auto loans and can offer quick decisions and competitive rates.

Pro tips from us: Multiple loan applications for the same type of loan within a short window (typically 14-45 days, depending on the credit scoring model) are usually grouped as a single hard inquiry on your credit report. This means you can shop for the best rate without significantly harming your credit score.

5. Submit Your Application

Once you’ve identified potential lenders, complete their pre-approval applications. This typically involves providing your personal and financial information. Be honest and accurate with all the details.

As mentioned earlier, pre-approval usually involves a "hard inquiry" on your credit report. This might cause a slight, temporary dip in your credit score, but the benefits of securing a great rate far outweigh this minor impact.

6. Review Offers and Choose Wisely

After submitting your applications, you’ll start receiving pre-approval offers. Carefully review each offer, paying close attention to:

- Interest Rate (APR): This is the most crucial factor, determining how much extra you’ll pay over the loan term.

- Loan Amount: Ensure it meets your budget.

- Loan Term: The length of the loan (e.g., 36, 48, 60, or 72 months). Longer terms mean lower monthly payments but more interest paid overall.

- Any Fees: Look for origination fees or other charges.

Choose the offer that best aligns with your financial situation and minimizes your overall cost.

Key Factors Lenders Consider for New Car Loan Pre-Approval

Lenders aren’t just looking at a single number; they assess several aspects of your financial profile to determine your eligibility and the terms of your new car loan pre-approval. Understanding these factors can help you strengthen your application.

Credit Score and History

Your credit score (FICO or VantageScore) is a snapshot of your creditworthiness. Lenders use it to gauge your reliability in repaying debts. A score of 660 and above is generally considered good for auto loans, with scores above 720 typically qualifying for the best rates. Your credit history, including past payments, bankruptcies, and delinquencies, also plays a significant role.

Debt-to-Income (DTI) Ratio

This ratio compares your total monthly debt payments (including your potential new car payment) to your gross monthly income. Lenders prefer a lower DTI, as it indicates you have enough disposable income to comfortably manage new debt. A DTI of 36% or lower is often ideal, though some lenders may approve higher ratios depending on other factors.

Income Stability and Employment History

Lenders want to see a steady and reliable source of income. This demonstrates your ability to make consistent loan payments. They will look at your employment history, preferring applicants with stable jobs and a consistent income over several years. Being self-employed may require additional documentation like tax returns to prove income.

Down Payment Amount

While not always mandatory, a substantial down payment reduces the risk for the lender. It also shows your commitment to the purchase and immediately creates equity in the vehicle. The more you put down, the less you need to borrow, potentially leading to better interest rates and easier approval.

Loan Term and Amount

The length of the loan and the total amount you wish to borrow also influence a lender’s decision. Shorter loan terms are generally viewed more favorably because the risk of default decreases over time. Lenders also assess whether the loan amount is appropriate for your income level.

Common Mistakes to Avoid During the New Car Loan Pre-Approval Process

While new car loan pre-approval is a powerful tool, certain missteps can hinder your chances or lead to a less favorable outcome. Common mistakes to avoid are:

Not Checking Your Credit Report

Failing to review your credit report before applying is a critical error. Errors can falsely lower your score, leading to higher interest rates or even rejection. Always check your reports and dispute inaccuracies. For more details on how to understand your credit report, refer to (Internal Link Placeholder: Link to an article about credit reports).

Only Applying to One Lender

As discussed, shopping around is key. Relying on a single lender, especially your primary bank, might mean missing out on significantly better interest rates from other institutions. Always compare offers.

Ignoring Your Budget

Getting pre-approved for a high amount doesn’t mean you should spend it all. Overstretching your budget can lead to financial strain down the road. Stick to a monthly payment you’re truly comfortable with, even if you’re approved for more.

Making Major Financial Changes

Avoid taking on new debt (like opening a new credit card), closing old credit accounts, or making significant career changes in the months leading up to and during your car loan application process. Such actions can negatively impact your credit score or perceived financial stability.

Falling for "Zero Down" Traps Without Understanding

While a "zero down" payment might sound appealing, it often means you’re borrowing the entire cost of the car, which can lead to higher monthly payments and more interest paid over time. It also means you have no equity in the car from day one, potentially putting you in an "upside-down" situation if the car depreciates quickly.

What Happens After You’re Pre-Approved?

Congratulations! You’ve successfully navigated the new car loan pre-approval process and have an offer in hand. Now, it’s time to put that power to good use.

Understanding Your Pre-Approval Offer

Your pre-approval letter will clearly state the maximum loan amount, the approved interest rate (APR), and the loan term. It might also list any specific conditions, such as the age or mileage limits for the vehicle you can purchase. Make sure you understand all the terms before heading to the dealership.

Using Your Pre-Approval at the Dealership

When you find the car you want, present your pre-approval letter to the dealership’s finance manager. This signals that you’re a serious buyer with financing already secured. You can now negotiate the vehicle’s price independently, without the added pressure of securing a loan.

Even with a pre-approval, it’s still wise to let the dealership’s finance department try to beat your rate. They often have access to various lenders and may be able to find an even better deal. If they can’t, you simply proceed with your pre-approved loan.

Pre-Approval vs. Pre-Qualification: Clarifying the Difference

These terms are often used interchangeably, but they represent distinct stages in the financing process. Understanding the difference is crucial for effective car shopping.

Pre-qualification is an initial, informal assessment. You provide some basic financial information, and the lender gives you an estimate of how much you might be able to borrow. This usually involves a "soft inquiry" on your credit report, which doesn’t affect your credit score. It’s a good way to get a general idea of your borrowing power without commitment.

New car loan pre-approval, on the other hand, is a more formal and thorough evaluation. It involves a "hard inquiry" on your credit report, a detailed review of your financial documents, and results in a conditional offer for a specific loan amount and interest rate. This is the stage that provides you with the leverage at the dealership.

Think of pre-qualification as "window shopping" for a loan, while pre-approval is like getting a binding purchase order.

Improving Your Chances of Getting Approved (and Securing Better Rates)

If you’re not entirely confident in your financial standing, there are proactive steps you can take to strengthen your application for a new car loan pre-approval and secure the most favorable terms.

Boost Your Credit Score

This is paramount. Pay all your bills on time, reduce outstanding credit card balances, and avoid opening new credit lines before applying. A higher credit score directly translates to lower interest rates and better loan offers. You can check your credit score and report for free annually from trusted sources like AnnualCreditReport.com (External Link: https://www.annualcreditreport.com/).

Reduce Your Debt-to-Income Ratio

Work on paying down existing debts, especially high-interest credit card balances. A lower DTI ratio signals to lenders that you have more financial capacity to take on a new car payment.

Save for a Larger Down Payment

The more you can put down upfront, the less you need to borrow. This reduces the lender’s risk and can lead to more attractive loan terms and easier approval. Aim for at least 10-20% of the car’s purchase price if possible.

Ensure Stable Employment

Lenders prefer applicants with a consistent work history. If you’ve recently changed jobs, be prepared to explain the transition and demonstrate income stability.

Conclusion: Drive Away Empowered with New Car Loan Pre-Approval

Embarking on the journey to purchase a new car can be one of life’s most exciting experiences. By understanding and utilizing the power of new car loan pre-approval, you transform a potentially stressful situation into an empowering one. You gain control over your financing, set clear budgets, save valuable time, and most importantly, secure the best possible deal.

Don’t leave your car financing to chance at the dealership. Take the proactive step, get pre-approved, and walk onto the lot with the confidence of a well-prepared buyer. Your perfect car, combined with the perfect loan, awaits. Start your pre-approval journey today and drive away with confidence and significant savings.