Your Ultimate Guide to Securing a $15,000 Car Loan: Approval Strategies & Smart Tips

Your Ultimate Guide to Securing a $15,000 Car Loan: Approval Strategies & Smart Tips Carloan.Guidemechanic.com

The dream of owning a reliable vehicle is a common aspiration for many. Whether you’re looking for a dependable used car or an entry-level new model, a $15,000 car loan often represents the perfect financial bridge to get you behind the wheel. However, navigating the world of auto financing can feel overwhelming, with countless terms, conditions, and factors influencing your approval.

This comprehensive guide is designed to demystify the process of securing a $15,000 car loan. We’ll delve deep into everything you need to know, from understanding what lenders look for to mastering the application process and even managing your loan post-approval. Our ultimate goal is to equip you with the knowledge and strategies to not only get your loan approved but to do so on the best possible terms, ensuring you drive away with confidence and peace of mind.

Your Ultimate Guide to Securing a $15,000 Car Loan: Approval Strategies & Smart Tips

Understanding the $15,000 Car Loan Landscape

A $15,000 car loan is a very common amount that many individuals seek when purchasing a vehicle. This figure often represents a sweet spot, allowing buyers to access a wide range of reliable used cars, including popular sedans, small SUVs, or even some well-maintained luxury models from a few years ago. It can also cover the cost of certain brand-new, entry-level vehicles, providing an accessible pathway to new car ownership.

Based on my experience in the auto finance industry, securing a $15,000 car loan can be a significant step towards financial responsibility. It’s a manageable amount for many budgets, yet substantial enough to purchase a quality vehicle that will serve your needs for years to come. The commitment involved is serious, and understanding what this amount entails is the first step toward a successful borrowing journey.

When considering a $15,000 car loan, it’s crucial to think about more than just the principal amount. You’ll need to factor in interest rates, loan terms, and potential fees, all of which will impact your total repayment. This initial understanding sets the foundation for a well-informed decision and helps you manage expectations throughout the application process.

Key Factors Lenders Consider for Your $15,000 Car Loan

Lenders are primarily looking for reassurance that you can consistently repay your $15,000 car loan without difficulty. They assess several critical factors to determine your creditworthiness and the level of risk associated with lending you money. Understanding these elements is crucial for preparing a strong application.

Your Credit Score: The Cornerstone of Approval

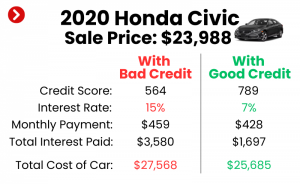

Your credit score is arguably the most influential factor in securing any loan, including a $15,000 car loan. This three-digit number, generated by credit bureaus, is a quick summary of your financial history and your ability to manage debt responsibly. A higher score generally indicates a lower risk to lenders.

For a $15,000 car loan, a good credit score (typically 670 and above) can unlock the most favorable interest rates and terms. This means lower monthly payments and less interest paid over the life of the loan. Conversely, a lower credit score might lead to higher interest rates or require additional conditions for approval, such as a larger down payment or a co-signer.

Common mistakes to avoid are applying for a loan without first knowing your credit score. This can lead to surprises and potentially multiple "hard inquiries" on your credit report, which can temporarily lower your score further. Always check your credit score beforehand to understand where you stand.

Income and Employment Stability: Proving Your Repayment Capacity

Lenders need to be confident that you have a steady and sufficient income to cover your monthly loan payments, alongside your existing financial obligations. They will typically ask for proof of income, such as recent pay stubs, tax returns, or bank statements, to verify your earnings. Employment stability is also a key indicator; a long history with the same employer often signals greater reliability.

Another critical metric lenders use is your Debt-to-Income (DTI) ratio. This ratio compares your total monthly debt payments (including your prospective car loan payment) to your gross monthly income. A lower DTI ratio indicates that you have more disposable income available to manage new debt, making you a more attractive borrower. Generally, lenders prefer a DTI ratio below 40-50%.

Ensuring your income is clearly documented and stable can significantly boost your chances of getting that $15,000 car loan approved. Any gaps in employment or inconsistent income might raise red flags, requiring you to provide additional explanations or documentation.

The Power of a Down Payment

While not always mandatory, making a down payment on your $15,000 car loan is highly beneficial. A down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the loan term. It also demonstrates your financial commitment to the purchase, signaling to lenders that you are a serious and responsible borrower.

Furthermore, a down payment helps improve your loan-to-value (LTV) ratio. The LTV ratio compares the loan amount to the car’s value. A lower LTV (meaning you’re borrowing less compared to the car’s worth) makes the loan less risky for the lender, as they have more equity in the vehicle if you default. Even a small down payment, such as 5-10% of the $15,000 purchase price, can make a significant difference in your approval odds and loan terms.

Loan-to-Value (LTV) Ratio: What It Is and Why It Matters

As mentioned, the Loan-to-Value (LTV) ratio is a crucial factor. It’s calculated by dividing the loan amount by the vehicle’s market value. For example, if you borrow $15,000 for a car valued at $15,000, your LTV is 100%. If you put down $3,000, borrowing $12,000 for the same $15,000 car, your LTV drops to 80%.

Lenders prefer a lower LTV because it means they have more collateral in the event of a default. A high LTV, especially above 100% (which can happen if you roll negative equity from a trade-in into the new loan), signals a higher risk. A healthy down payment directly contributes to a lower LTV, making your $15,000 car loan application more appealing.

Preparing for Your $15,000 Car Loan Application

Thorough preparation is the bedrock of a successful car loan application. By taking these proactive steps, you can significantly enhance your chances of approval and secure more favorable terms for your $15,000 car loan.

Check Your Credit Report and Score

Before you even think about applying for a $15,000 car loan, your first step should always be to review your credit report and score. You can obtain a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once every 12 months through AnnualCreditReport.com. This official site is a trusted resource for accessing your reports.

Carefully examine your reports for any inaccuracies or errors. Identity theft or clerical mistakes can negatively impact your score, so it’s vital to dispute any discrepancies immediately. Correcting errors can sometimes significantly boost your score. If your score is lower than you’d like, focus on actionable steps: pay down high-interest credit card debt, ensure all your bill payments are made on time, and avoid opening new lines of credit just before applying for your car loan.

Determine Your Realistic Budget

While you’re seeking a $15,000 car loan, the car’s purchase price is just one part of the equation. Pro tips from us: Don’t just focus on the car’s price; think about the total cost of ownership. This includes insurance premiums, fuel costs, maintenance, registration fees, and potential repair expenses. These ongoing costs can add up quickly and impact your ability to comfortably afford the monthly loan payments.

Calculate what you can realistically afford for a monthly car payment. Use online car loan calculators to estimate payments based on different interest rates and loan terms. Remember to factor in your existing monthly expenses and income. Overstretching your budget for a car loan can lead to financial strain down the road.

Gather Necessary Documents

Being prepared with all the required documentation streamlines the application process and shows lenders you are organized and serious. While specific requirements can vary slightly between lenders, here’s a general list of documents you’ll likely need:

- Proof of Identity: A valid driver’s license, state ID, or passport.

- Proof of Income: Recent pay stubs (typically 1-3 months), W-2 forms, or tax returns if self-employed.

- Proof of Residence: Utility bills, lease agreements, or mortgage statements showing your current address.

- Social Security Number: For credit checks.

- Bank Statements: To verify your financial stability and ability to make a down payment.

Having these documents readily available will prevent delays and make your application much smoother.

Consider a Down Payment: How Much is Enough?

We’ve already touched upon the benefits of a down payment, but it bears repeating: it’s one of the most effective ways to improve your chances of approval and get better loan terms. Even a modest down payment can make a difference. For a $15,000 car loan, aiming for at least 5-10% ($750 – $1,500) is a good starting point.

A larger down payment not only reduces your principal loan amount but also decreases the interest you’ll pay over time and can help you avoid being "upside down" on your loan (owing more than the car is worth). If you can manage 20% or more, you’ll be in an even stronger position to negotiate excellent rates and terms.

Where to Get Your $15,000 Car Loan

Knowing where to apply for your $15,000 car loan is just as important as preparing your application. Different lenders offer varying rates, terms, and customer experiences. Exploring multiple options allows you to find the best fit for your financial situation.

Dealership Financing: Convenience at Your Fingertips

Many car dealerships offer on-site financing, which can be incredibly convenient. You can test drive, negotiate, and secure a loan all in one place. Dealerships work with a network of lenders and can sometimes offer promotional interest rates, especially on new vehicles. This "one-stop shop" approach is appealing for its simplicity.

However, convenience doesn’t always translate to the best rates. While dealerships can be competitive, it’s wise to compare their offers with other lenders. Common mistakes to avoid are only checking one lender, as you might miss out on better deals elsewhere.

Banks and Credit Unions: Often Competitive Rates

Traditional banks and credit unions are excellent sources for car loans. Banks typically have a wide reach and offer various loan products, while credit unions, being not-for-profit institutions, are often known for offering some of the most competitive interest rates and personalized service, especially to their members. Based on my experience, credit unions often offer some of the most favorable rates for a $15,000 car loan, making them a strong contender.

If you have an existing relationship with a bank or credit union, it’s always a good idea to start there. They may offer preferential rates or streamlined application processes for their loyal customers.

Online Lenders: Quick Approvals and Wide Options

The digital age has brought forth a plethora of online lenders specializing in auto loans. These platforms often provide quick pre-approvals, allowing you to compare multiple offers from various lenders without leaving your home. They can be particularly useful for individuals with a range of credit scores, including those with fair or challenging credit histories.

Online lenders offer transparency and efficiency, making it easier to shop around and find the best rates for your $15,000 car loan. However, always ensure you’re dealing with reputable and secure online platforms by checking reviews and looking for legitimate certifications.

The Power of Pre-Approval

Regardless of where you choose to apply, seeking pre-approval is a smart strategy. Pre-approval means a lender has conditionally agreed to lend you a specific amount (like $15,000) at a particular interest rate, based on a preliminary review of your credit and financial information.

The benefits of pre-approval are numerous:

- Know Your Budget: You’ll know exactly how much you can afford before you start car shopping, streamlining your search.

- Negotiate Like a Cash Buyer: With a pre-approval in hand, you can focus on negotiating the car’s price, rather than being swayed by dealer financing offers. This puts you in a stronger bargaining position.

- Avoid Multiple Hard Inquiries: Getting pre-approved from a few lenders within a short timeframe (usually 14-45 days, depending on the credit scoring model) will typically only count as a single hard inquiry on your credit report, minimizing the impact on your score. This allows you to shop for the best rates without penalty.

Strategies for Getting Your $15,000 Car Loan Approved (Even with Challenges)

Securing a $15,000 car loan is achievable for most people, but the approach you take can significantly impact your success and the terms you receive. Your credit score, in particular, will dictate some of your best strategies.

For Good Credit (670+ FICO Score)

If you boast a strong credit score, you’re in an excellent position. Your primary focus should be on securing the lowest possible interest rate and the most flexible terms. Lenders will compete for your business.

- Shop Around Aggressively: Don’t settle for the first offer. Get pre-approvals from multiple banks, credit unions, and online lenders.

- Negotiate Rates and Terms: Use competing offers as leverage to negotiate even better rates. Ask about any fees and whether they can be waived.

- Choose a Shorter Loan Term: While a longer term means lower monthly payments, a shorter term (e.g., 36-48 months for a $15,000 car loan) will significantly reduce the total interest you pay. If you can comfortably afford the higher monthly payment, it’s a smart financial move.

For Fair Credit (580-669 FICO Score)

With fair credit, getting approved for a $15,000 car loan is still very possible, but you might face slightly higher interest rates. The key here is to mitigate perceived risk for lenders.

- Emphasize a Down Payment: A substantial down payment becomes even more critical with fair credit. It lowers the loan amount and demonstrates your commitment, making you a more attractive borrower.

- Consider a Shorter Loan Term (If Affordable): While it means higher monthly payments, a shorter term can signal to lenders that you’re less of a long-term risk and might help you secure a slightly better rate.

- Highlight Stable Income/Employment: If you have a steady job history and a good income-to-debt ratio, emphasize this during your application.

- Shop Around Aggressively: Comparison shopping is paramount. Different lenders have different criteria, and one might offer you a significantly better rate than another.

For Bad Credit (Below 580 FICO Score)

Securing a $15,000 car loan with bad credit can be challenging, but it’s not impossible. You should expect higher interest rates, but there are strategies to improve your chances.

- Strong Down Payment is Critical: This is your most powerful tool. A significant down payment reduces the loan amount and the lender’s risk, making approval much more likely.

- Consider a Co-signer: A co-signer with good credit can significantly improve your approval odds and help you get a lower interest rate. A co-signer essentially guarantees the loan, taking on responsibility if you default. However, understand the implications for both parties before going this route.

- Explore Dealership Special Finance Departments: Many dealerships have departments that specialize in helping customers with less-than-perfect credit secure auto loans.

- Focus on Improving Credit First: If you’re not in a rush, taking 3-6 months to improve your credit score by paying down debts and making on-time payments can save you thousands in interest over the life of the loan. For a deeper dive into improving your credit score, read our article on ‘Building Credit for Your First Car Loan’.

- Be Realistic About Interest Rates: Expect higher APRs. The goal is to get approved and then focus on making consistent payments to rebuild your credit for potential refinancing later.

Understanding Loan Terms: 36, 48, 60, 72 Months, and Beyond

The loan term, or the length of time you have to repay the loan, directly impacts your monthly payment and the total interest paid.

- Shorter Terms (e.g., 36-48 months): Lead to higher monthly payments but significantly less interest paid over the life of the loan. This is often the most financially savvy choice if you can afford the payments.

- Longer Terms (e.g., 60-72 months): Result in lower monthly payments, making the car more "affordable" on a month-to-month basis. However, you’ll pay substantially more in total interest, and the car’s value may depreciate faster than you pay off the loan, leading to negative equity.

Pro tips from us: Aim for the shortest loan term you can comfortably afford without straining your budget. Never sign a loan agreement you don’t fully understand; always read the fine print.

The Loan Application Process and What to Expect

Once you’ve done your preparation and chosen your potential lenders, the application process for your $15,000 car loan typically follows a standard path.

First, you’ll fill out a loan application form, either online or in person. This form will request personal information, employment details, income specifics, and your financial history. Be thorough and honest, as any discrepancies can lead to delays or denial.

Next, you’ll submit your gathered documentation, such as proof of identity, income, and residence. This is where your prior preparation pays off, allowing for a smooth submission. The lender will then perform a "hard inquiry" on your credit report to assess your creditworthiness.

This leads to the underwriting process, where the lender evaluates all the information provided to determine your eligibility and the terms of your loan offer. This can take anywhere from a few hours to a few business days, depending on the lender and the complexity of your application.

If approved, you’ll receive a loan offer outlining the principal amount, interest rate (APR), loan term, and total cost of the loan. It’s crucial to review this offer carefully. If denied, don’t despair. Ask the lender for the specific reasons for denial; this information is valuable for improving future applications or exploring alternative solutions.

Post-Approval: Managing Your $15,000 Car Loan

Securing your $15,000 car loan is a significant achievement, but the journey doesn’t end there. Responsible loan management is crucial for maintaining good credit and achieving financial stability.

The most important aspect of managing your loan is making on-time payments. Consistent, timely payments are the cornerstone of building a positive credit history and will positively impact your credit score. This can open doors to better financial products and lower interest rates on future loans.

Consider setting up automatic payments from your bank account. This ensures you never miss a due date, preventing late fees and negative marks on your credit report. Many lenders even offer a small interest rate discount for setting up auto-pay.

Finally, keep an eye on refinancing opportunities. If your credit score significantly improves after a year or two of diligent payments, or if market interest rates drop, you might be able to refinance your $15,000 car loan at a lower interest rate. This can save you a substantial amount of money over the remaining loan term. Learn more about managing debt and improving your financial health in our guide to ‘Smart Financial Planning’.

Conclusion: Driving Away with Confidence

Securing a $15,000 car loan doesn’t have to be a daunting task. By understanding the key factors lenders consider, meticulously preparing your application, and exploring various financing options, you significantly increase your chances of approval on favorable terms. Remember, knowledge is power in the world of auto finance.

From checking your credit score to gathering documents and comparing loan offers, each step plays a vital role in your success. Whether you have excellent credit or are working to rebuild it, a strategic approach will guide you towards a positive outcome.

Armed with the insights from this comprehensive guide, you are now well-equipped to navigate the loan process with confidence. Start your journey today, make informed decisions, and soon you’ll be driving away in your new or new-to-you vehicle, knowing you’ve secured your $15,000 car loan wisely and responsibly.