Your Ultimate Guide to Securing a Car Loan: A Step-by-Step Journey to Approval

Your Ultimate Guide to Securing a Car Loan: A Step-by-Step Journey to Approval Carloan.Guidemechanic.com

Buying a new car is an exciting milestone, but the path to driving it off the lot often involves navigating the world of car loans. For many, applying for a car loan can feel daunting, filled with jargon and complex processes. However, understanding "how do you apply for a car loan" is not just about filling out forms; it’s about empowering yourself with knowledge to make smart financial decisions, secure the best terms, and ultimately, get approved with confidence.

As an expert blogger and professional SEO content writer, I’ve seen firsthand how clarity and preparation can transform a potentially stressful experience into a smooth, successful one. This comprehensive guide is designed to be your trusted companion, breaking down every aspect of the car loan application process into easy-to-understand steps. We’ll dive deep into what lenders look for, how to optimize your application, and common pitfalls to avoid, ensuring you’re well-equipped to secure the financing you need.

Your Ultimate Guide to Securing a Car Loan: A Step-by-Step Journey to Approval

Why Understanding the Car Loan Process is Crucial for Every Buyer

Securing a car loan isn’t merely a transaction; it’s a significant financial commitment that can impact your budget for years to come. Many people rush into the process, only to find themselves with higher interest rates, unfavorable terms, or even outright rejection. This often stems from a lack of understanding about what lenders genuinely prioritize.

Based on my experience, proactive learning about the car loan application process is your best defense against bad deals. It empowers you to negotiate effectively, recognize predatory lending practices, and ultimately, save hundreds or even thousands of dollars over the life of your loan. Knowing the ins and outs allows you to approach lenders from a position of strength, not desperation.

Before You Apply: Essential Preparations for Car Loan Success

The secret to a successful car loan application often lies in the groundwork you lay before you even speak to a lender. These preparatory steps are fundamental to not only getting approved but also securing the most favorable terms possible.

A. Know Your Credit Score & Report Inside Out

Your credit score is arguably the most influential factor in your car loan application. Lenders use it as a snapshot of your financial responsibility, predicting your likelihood of repaying the loan. A higher credit score signals lower risk, leading to better interest rates and easier approval.

Understanding your credit score means more than just knowing a number. It involves reviewing your full credit report from all three major bureaus (Experian, Equion, and TransUnion) for accuracy. You are entitled to a free report from each bureau once every 12 months via AnnualCreditReport.com. Any discrepancies, such as incorrect late payments or fraudulent accounts, can negatively impact your score and must be disputed promptly. Correcting these errors before applying can significantly boost your chances of approval and reduce your interest rates.

B. Determine Your Realistic Budget

Before falling in love with a specific car, establish a clear and realistic budget. This isn’t just about the monthly car payment; it encompasses the total cost of car ownership. Consider insurance premiums, fuel costs, maintenance, registration fees, and any potential repair costs. A common mistake is to focus solely on the monthly payment without considering the broader financial picture.

Your debt-to-income (DTI) ratio is also crucial here. Lenders assess how much of your gross monthly income goes towards debt payments. A lower DTI ratio (typically below 40%) indicates that you have sufficient income to handle additional debt, making you a more attractive borrower. Calculate your current DTI and ensure a new car payment won’t push you into an unfavorable range.

C. Research and Compare Loan Options

The days of simply walking into a dealership and accepting their financing offer are long gone. Today, you have a plethora of options for securing a car loan, and exploring them is paramount.

- Banks: Traditional banks often offer competitive rates, especially if you’re an existing customer with a strong relationship.

- Credit Unions: These member-owned institutions are known for offering some of the lowest interest rates due to their non-profit status. They often have more flexible lending criteria than large banks.

- Online Lenders: Companies like LightStream or Capital One Auto Finance provide quick online applications and pre-approvals, making it easy to compare offers from the comfort of your home.

- Dealership Financing: While convenient, dealership financing often involves them acting as a middleman, potentially marking up interest rates. It’s crucial to compare their offer against others you’ve secured.

Pro tips from us: Always get pre-approved by at least two to three external lenders (banks, credit unions, online) before visiting a dealership. This provides you with leverage and a baseline to compare against any offers the dealer presents. Not doing so is a common mistake that can cost you significantly.

D. Gather All Necessary Documents

Having your documents organized and ready will streamline the application process and prevent delays. While specific requirements can vary slightly by lender, a standard list typically includes:

- Proof of Identity: A valid driver’s license or state-issued ID.

- Proof of Income: Recent pay stubs (typically 1-3 months), W-2 forms, tax returns (especially for self-employed individuals), or bank statements.

- Proof of Residence: Utility bills, a lease agreement, or mortgage statements with your current address.

- Social Security Number: For credit checks.

- Vehicle Information (if already chosen): Make, model, year, VIN, and sale price.

- Proof of Insurance: You’ll need to show proof of full coverage insurance before driving the car off the lot.

Having these documents readily available demonstrates your preparedness and seriousness as a borrower, making the application process much smoother for both you and the lender.

The Step-by-Step Car Loan Application Process

Once your groundwork is complete, you’re ready to embark on the actual car loan application journey. Following these steps will guide you efficiently towards approval.

Step 1: Get Pre-Approved (Highly Recommended)

Pre-approval is an invaluable first step. It means a lender has reviewed your financial information and tentatively agreed to lend you a specific amount at a particular interest rate, contingent on the final verification of your details and the chosen vehicle. This usually involves a "soft" credit inquiry, which doesn’t harm your credit score.

Based on my experience, pre-approval is a game-changer because it transforms you into a cash buyer at the dealership. You walk in knowing exactly how much you can spend, empowering you to negotiate on the car’s price rather than getting fixated on the monthly payment. This drastically reduces stress and makes the car buying process much more transparent and enjoyable.

Step 2: Find Your Ideal Vehicle

With a pre-approval in hand, you now have a clear spending limit, which makes car shopping much more focused. Research vehicles that fit your budget, lifestyle, and needs. Consider factors like reliability, fuel efficiency, safety ratings, and resale value.

Whether you opt for a new or used car, ensure the vehicle’s price aligns with your pre-approved loan amount. If you’re buying a used car, a pre-purchase inspection by an independent mechanic is a wise investment to avoid costly surprises down the road.

Step 3: Complete the Full Loan Application

Once you’ve settled on a vehicle, you’ll complete the official loan application. This form will ask for detailed personal and financial information, including your employment history, residential history, income, and existing debts. This is where all those documents you gathered earlier come into play.

Be meticulous when filling out the application. Any inconsistencies or missing information can cause delays or even lead to rejection. The lender will then perform a "hard" credit inquiry, which will temporarily ding your credit score by a few points. However, multiple hard inquiries for the same type of loan within a short period (typically 14-45 days, depending on the scoring model) are usually grouped as a single inquiry, so rate shopping for a car loan won’t significantly harm your credit.

Step 4: Review Loan Offers

After submitting your application, lenders will evaluate your creditworthiness and present you with loan offers. This is where your pre-approval comparison becomes critical. Don’t just look at the monthly payment; scrutinize the Annual Percentage Rate (APR), the total loan term, and any associated fees.

The APR is the true cost of borrowing, encompassing the interest rate and certain fees. A lower APR means less money paid over the life of the loan. A longer loan term (e.g., 72 or 84 months) might offer lower monthly payments but will result in paying significantly more interest overall. Carefully compare each offer’s APR, total cost of the loan, and monthly payment to determine the best fit for your financial situation.

Step 5: Finalize the Loan and Purchase

Once you’ve chosen the best loan offer, you’ll proceed to finalize the paperwork. This involves signing the loan agreement and any other necessary documents with the lender or dealership. Make sure you read every line of the contract before signing. Don’t hesitate to ask questions if anything is unclear.

Ensure all the terms discussed are accurately reflected in the final agreement, including the vehicle price, interest rate, loan term, and any down payment or trade-in value. Once signed, the funds are disbursed, and you can officially take ownership of your new car!

Factors That Influence Car Loan Approval & Interest Rates

Understanding the elements that sway a lender’s decision is key to improving your chances of approval and securing favorable terms. It’s a complex interplay of several factors, each playing a crucial role.

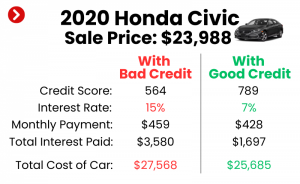

Credit Score: As mentioned, your credit score is paramount. Scores above 700 are generally considered "good" and qualify for prime rates, while scores above 760 are "excellent" and unlock the best available rates. Lower scores might still get approved, but often with higher interest rates to offset the perceived risk.

Income Stability and Amount: Lenders want assurance that you have a consistent and sufficient income to make your monthly payments. A stable job history, typically two years or more with the same employer, is a strong positive indicator. The higher your income relative to your debt obligations, the better your chances.

Debt-to-Income (DTI) Ratio: This ratio measures how much of your gross monthly income is consumed by debt payments. A low DTI ratio (ideally under 40%) signals that you’re not overextended financially and have room for a new car payment.

Down Payment Amount: A substantial down payment reduces the amount you need to borrow, thereby lowering the lender’s risk. It also demonstrates your financial commitment and can lead to better loan terms and lower monthly payments. Aim for at least 10-20% of the car’s value, if possible.

Loan Term: The length of your loan affects both your monthly payment and the total interest paid. Shorter terms (e.g., 36 or 48 months) typically have higher monthly payments but less total interest. Longer terms (e.g., 60, 72, or 84 months) offer lower monthly payments but accrue more interest over time. Lenders may view very long terms as higher risk due to vehicle depreciation.

Vehicle Age and Type: Lenders are often more willing to finance newer vehicles with lower mileage because they hold their value better. Older, high-mileage cars might be harder to finance or come with higher interest rates due to increased depreciation and potential reliability issues.

Special Considerations for Your Car Loan Journey

Not everyone’s financial situation is the same, and sometimes, you need to navigate unique circumstances.

Applying for a Car Loan with Bad Credit

Having a less-than-perfect credit score doesn’t automatically disqualify you from getting a car loan, but it does require a more strategic approach. Lenders specializing in "subprime" loans exist for this very reason.

Strategies for bad credit include:

- A Larger Down Payment: This reduces the loan amount and the lender’s risk.

- A Co-signer: A co-signer with good credit can significantly improve your chances of approval and secure a better interest rate. However, remember they are equally responsible for the loan.

- Lower-Cost Vehicle: Opting for a more affordable, reliable used car will reduce the overall loan amount and make payments more manageable.

- Credit Building: If possible, take time to improve your credit score before applying. Even small improvements can make a difference.

- Shop Around: Don’t just accept the first offer. Compare subprime lenders, credit unions, and even some traditional banks that might have specific programs.

Be realistic about your expectations; interest rates will likely be higher with bad credit, but it’s a stepping stone to rebuilding your credit through responsible payments.

Refinancing Your Car Loan

Refinancing your car loan means taking out a new loan to pay off your existing one, often with more favorable terms. This can be a smart move if:

- Your Credit Score Has Improved: If you’ve diligently made payments and your credit score has increased since you first got the loan, you might qualify for a lower interest rate.

- Interest Rates Have Dropped: Market interest rates fluctuate. If rates are lower now than when you first financed, refinancing could save you money.

- You Want to Change Your Loan Term: You might want to shorten your term to pay off the loan faster or lengthen it to reduce monthly payments (though this often means more total interest).

- You’re Stuck with a Bad Deal: If you rushed into a loan with a high interest rate, refinancing offers a second chance to improve your terms.

Always compare potential savings against any refinancing fees to ensure it’s a financially sound decision.

Common Mistakes to Avoid During Your Car Loan Application

Navigating the car loan landscape can be tricky, and certain missteps are frequently observed. Avoiding these common mistakes will significantly improve your experience and outcomes.

- Not Checking Your Credit Report: As discussed, this is foundational. Failing to review your report means you’re walking into the process blind, potentially unaware of errors or areas for improvement.

- Only Considering One Lender: Relying solely on the dealership’s financing or just one bank means you miss out on potentially better offers. Always shop around!

- Focusing Solely on the Monthly Payment: While important, an artificially low monthly payment might come with an extended loan term and a much higher total cost due to increased interest.

- Ignoring the Total Cost of the Loan: Always calculate the total amount you’ll pay over the loan’s lifetime (principal + interest). A small difference in APR can translate to thousands of dollars.

- Falling for Unnecessary Add-ons: Dealerships often push extended warranties, GAP insurance, or other add-ons. While some might be beneficial, assess their true value and necessity before adding them to your loan, as they increase your total debt.

- Applying for Too Many Loans Simultaneously (Without Knowing the Rules): While multiple car loan inquiries within a short window are usually grouped, applying for different types of credit (e.g., a car loan, a credit card, and a mortgage) simultaneously can negatively impact your credit score.

From years of observing loan applications, these mistakes are easily avoidable with a bit of foresight and education.

Pro Tips for a Smooth Car Loan Approval

Beyond the steps and warnings, here are some actionable pro tips from our team to ensure your car loan application process is as smooth and successful as possible:

- Maintain Stable Employment: Lenders favor stability. Avoid job hopping right before or during your loan application.

- Pay Down Other Debts: Reducing your existing debt obligations will improve your debt-to-income ratio, making you a more attractive borrower.

- Avoid New Credit Applications: Don’t open new credit cards or take out other loans in the months leading up to your car loan application, as this can negatively impact your credit score.

- Have a Clear Financial Picture: Be transparent and honest on your application. Lenders will verify your information, and discrepancies can lead to rejection.

- Understand Your "Why": Be clear about why you need the car and why this specific car fits your needs. While not directly financial, it helps you remain focused and avoid impulsive decisions.

- Consider a Co-Applicant (If Applicable): If your credit isn’t stellar, applying with a financially strong co-applicant can significantly improve your chances and secure better terms.

By integrating these strategies into your approach, you’re not just applying for a car loan; you’re setting yourself up for financial success.

Conclusion: Drive Away with Confidence

Applying for a car loan doesn’t have to be a bewildering experience. By understanding "how do you apply for a car loan" in depth, from meticulous preparation to careful comparison and finalization, you empower yourself to navigate the process with confidence and clarity. Remember, knowledge is your most powerful tool in securing the best possible terms.

Start by checking your credit, setting a realistic budget, and comparing lenders. Get pre-approved to gain negotiation leverage, and meticulously review all offers. By avoiding common pitfalls and applying the pro tips outlined in this guide, you’ll not only increase your chances of approval but also save money and drive away in your new vehicle with peace of mind. Your journey to car ownership begins with an informed and strategic approach. Start preparing today, and enjoy the ride!