Your Ultimate Guide to Securing a Personal Car Loan: Drive Away with Confidence

Your Ultimate Guide to Securing a Personal Car Loan: Drive Away with Confidence Carloan.Guidemechanic.com

Buying a car is an exciting milestone for many, but the journey to getting the right financing can often feel like navigating a complex maze. For most people, a personal car loan is the bridge that connects them to their dream vehicle. But how do you secure one successfully? How do you ensure you get the best terms, avoid common pitfalls, and ultimately drive away with confidence?

This comprehensive guide is designed to demystify the process of how to get a personal car loan. We’ll break down every step, from initial preparation to final approval, providing you with the knowledge and strategies you need to make informed decisions. Our goal is to equip you with the insights that will not only get your personal car loan approved but also ensure it’s the best fit for your financial situation.

Your Ultimate Guide to Securing a Personal Car Loan: Drive Away with Confidence

Understanding the Landscape of Personal Car Loans

Before diving into the application process, it’s crucial to understand what a personal car loan truly entails and the various avenues available for obtaining one. This foundational knowledge will empower you to choose the right path for your specific needs.

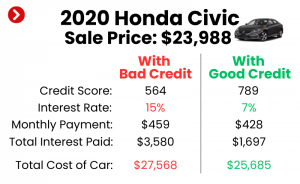

A personal car loan is a specific type of installment loan designed to finance the purchase of a vehicle. Unlike a general personal loan, which can be used for anything, a car loan is typically "secured" by the vehicle itself. This means the car serves as collateral; if you fail to make payments, the lender has the right to repossess the vehicle. This security often results in lower interest rates compared to unsecured personal loans, as it reduces the risk for the lender.

The Different Faces of Lenders

When seeking a personal car loan, you’ll encounter a variety of lenders, each with their own advantages and disadvantages. Knowing these options will help you shop around effectively.

- Banks: Traditional banks are a popular choice, offering competitive rates, a wide range of loan products, and often personalized service if you’re an existing customer. They typically require good to excellent credit for the best terms.

- Credit Unions: These member-owned financial institutions are renowned for their customer-centric approach and often offer some of the most competitive interest rates. Becoming a member is usually straightforward, and they can sometimes be more flexible with borrowers who have less-than-perfect credit.

- Dealership Financing: Many car dealerships offer financing options directly through their partnerships with various banks and financial institutions. This can be convenient, allowing for a one-stop-shop experience. However, it’s essential to be vigilant, as dealership financing might not always present the absolute best rates upfront, and you might need to negotiate.

- Online Lenders: The digital age has brought forth a plethora of online-only lenders specializing in car loans. These platforms often offer quick application processes, fast approvals, and can be a good option for those seeking convenience or specific loan types. They can also cater to a broader spectrum of credit scores.

Based on my experience, exploring multiple lender types is key. Don’t limit yourself to just the dealership’s offer. Comparing offers from banks, credit unions, and online lenders before you even set foot on a car lot can save you a significant amount of money over the life of the loan.

The Foundation: Preparing for Your Car Loan Application

Success in securing a favorable personal car loan hinges heavily on preparation. Think of it like building a house; a strong foundation ensures stability and longevity. Neglecting these preliminary steps can lead to higher interest rates, less favorable terms, or even rejection.

Check Your Credit Score and Report

Your credit score is arguably the most critical factor lenders consider. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. A higher score signals less risk to lenders, translating into better interest rates and loan terms.

Pro tips from us: Start by obtaining your credit score and a full copy of your credit report well in advance of applying for a personal car loan. You can get free copies of your credit report from each of the three major bureaus (Experian, Equifax, TransUnion) once a year at AnnualCreditReport.com. Scrutinize these reports for any errors, such as accounts that aren’t yours, incorrect payment statuses, or outdated information. Disputing and correcting these errors can significantly boost your score.

Determine Your Budget: Beyond the Monthly Payment

While the monthly payment is important, your budget for a car extends far beyond that figure. It’s crucial to consider the total cost of car ownership. This includes not only the loan principal and interest but also insurance, fuel, maintenance, registration fees, and potential repair costs.

A common mistake to avoid is focusing solely on the lowest possible monthly payment without considering the total loan amount and interest paid over the loan term. Use online calculators to estimate various payment scenarios and understand how different interest rates and loan lengths impact your total outlay. Ensure your budget comfortably accommodates all these expenses without straining your finances.

Save for a Down Payment

A down payment is the initial sum of money you pay towards the purchase of a car, reducing the amount you need to borrow. While not always strictly required, making a significant down payment offers numerous benefits.

Firstly, it reduces your monthly payments and the total interest paid over the life of the personal car loan. Secondly, it immediately gives you equity in the vehicle, which can prevent you from being "upside down" on your loan (owing more than the car is worth). Lenders also view a larger down payment favorably, as it demonstrates your financial commitment and reduces their risk, potentially leading to better loan terms. Aim for at least 10-20% of the car’s purchase price, if possible.

The Pre-Approval Advantage: Your Secret Weapon

Once your financial house is in order, the next strategic step in how to get a personal car loan is seeking pre-approval. This often overlooked step can transform your car buying experience from stressful to empowering.

Pre-approval is when a lender reviews your financial information and tentatively agrees to lend you a specific amount of money at a certain interest rate, pending a final vehicle selection and verification. It’s a conditional offer, but it comes with immense benefits.

Why Pre-Approval Puts You in the Driver’s Seat

- Negotiating Power: Walking into a dealership with a pre-approval letter is like having cash in hand. It signals to the dealer that you’re a serious buyer with financing already secured. This puts you in a much stronger position to negotiate the car’s price, as you won’t be reliant on their financing options.

- Know Your Limits: Pre-approval clearly defines how much you can afford, preventing you from falling in love with a car outside your budget. This helps you stick to your financial plan.

- Streamlined Process: With pre-approval, much of the paperwork is already done. This can significantly speed up the purchasing process at the dealership, allowing you to focus on the car itself.

- Comparison Shopping: You can use your pre-approval offer as a benchmark. If the dealership offers a better rate, great! If not, you have a solid offer to fall back on.

To get pre-approved for a personal car loan, you’ll typically need to provide similar documentation as for a full application: proof of income, identification, and a consent for a credit check. We strongly recommend applying to a few different lenders (banks, credit unions, online) within a short window (typically 14-45 days) to minimize the impact on your credit score. This allows you to compare offers and choose the best one.

Navigating the Application Process: Step-by-Step

With your preparation complete and potentially a pre-approval in hand, you’re ready to tackle the formal application for your personal car loan. This stage requires attention to detail and a clear understanding of what you’re agreeing to.

Gathering Essential Documents

Lenders need specific documents to verify your identity, income, and ability to repay the loan. Having these ready will expedite the application process.

Typically, you’ll need:

- Government-issued ID: Driver’s license or passport.

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2s, or tax returns if self-employed.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Social Security Number.

- Vehicle Information: If you’ve already chosen a car, details like the VIN, make, model, and mileage will be required.

- Proof of Car Insurance: Lenders will almost always require you to have comprehensive and collision insurance before finalizing the loan.

Choosing the Right Lender (If Not Already Pre-Approved)

If you haven’t secured pre-approval, or if you’re looking for a better offer than your pre-approval, this is the time to evaluate lenders more deeply. Consider the interest rates, loan terms (how long you have to pay it back), and any fees associated with the personal car loan.

Look beyond just the lowest interest rate; some lenders might offer slightly higher rates but have more flexible repayment options or better customer service. Check online reviews and ask friends or family for recommendations. For specific advice on choosing between different financial institutions, you might find helpful.

Understanding Loan Terms: APR, Term Length, and Payments

Before signing anything, it’s paramount to fully understand the terms of your personal car loan. The Annual Percentage Rate (APR) is particularly important, as it represents the total cost of borrowing, including the interest rate and certain fees, expressed as a yearly percentage. This is the best figure to compare across different loan offers.

The loan term, or length, also significantly impacts your monthly payments and the total interest paid. A longer term means lower monthly payments but more interest paid over time. A shorter term means higher monthly payments but less overall interest. Find a balance that fits your budget comfortably without extending the loan unnecessarily.

Common Mistakes to Avoid During Application

Based on my experience, several pitfalls can derail your application or lead to less favorable terms. One common mistake is applying to too many lenders within a short period, known as "shotgunning." Each application can result in a hard inquiry on your credit report, which can temporarily lower your score. While applying for pre-approval within a specific window is usually grouped as one inquiry, multiple applications outside this window can be detrimental.

Another mistake is not reading the fine print. Always scrutinize the loan agreement for hidden fees, prepayment penalties (though less common with car loans), and any clauses that you don’t fully understand. If something isn’t clear, ask for clarification. Don’t feel pressured to sign until you’re completely comfortable.

What Lenders Look For: The Approval Criteria Decoded

Lenders assess several factors to determine your eligibility and the risk associated with lending to you. Understanding these criteria will help you present yourself as an ideal borrower for a personal car loan.

Credit Score & History: The Primary Factor

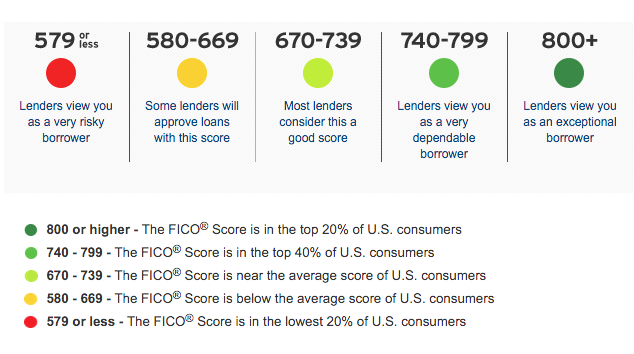

As mentioned, your credit score is a major determinant. Lenders use it to gauge your reliability in managing debt. A FICO score of 660 and above is generally considered good, making you eligible for better rates. Scores below this may still qualify for a personal car loan, but often with higher interest rates or stricter conditions. Your credit history, showing consistent on-time payments, diverse credit types, and a low credit utilization ratio, further strengthens your application.

Income & Employment Stability: Your Ability to Repay

Lenders want assurance that you have a steady income stream to comfortably cover your monthly car loan payments. They will typically ask for proof of employment and income, often looking for a consistent work history (e.g., at least 6 months to 2 years with the same employer). Stable employment indicates a reliable source of funds, making you a less risky borrower.

Debt-to-Income (DTI) Ratio: How Much Debt You Already Have

Your Debt-to-Income (DTI) ratio is another critical metric. It’s calculated by dividing your total monthly debt payments by your gross monthly income. Lenders prefer a DTI ratio of 36% or lower, though some may go up to 43-50%. A high DTI suggests that a significant portion of your income is already allocated to existing debts, potentially leaving less room for a new car loan payment.

Down Payment & Trade-in: Showing Commitment

A substantial down payment or a valuable trade-in reduces the amount you need to borrow, thereby lowering the lender’s risk. It demonstrates your financial commitment to the purchase and indicates that you are less likely to default on the personal car loan. The more equity you have in the vehicle from day one, the more attractive you appear to lenders.

Vehicle Information: Age, Mileage, Value

For a secured personal car loan, the vehicle itself plays a role. Lenders will assess the car’s make, model, year, mileage, and overall condition to determine its value. This is because the car serves as collateral. Older vehicles or those with very high mileage might be considered higher risk, as their resale value depreciates faster, and they may be more prone to mechanical issues. Some lenders have restrictions on the age or mileage of vehicles they will finance.

Special Considerations: Bad Credit and First-Time Buyers

Not everyone starts with a perfect credit score or a long history of borrowing. If you fall into these categories, don’t despair; securing a personal car loan is still possible, though it may require a different approach.

Getting a Car Loan with Bad Credit

Having bad credit can make securing a car loan more challenging, often resulting in higher interest rates. However, it’s not impossible.

- Strategies:

- Larger Down Payment: As discussed, a larger down payment reduces the loan amount and signals commitment.

- Co-signer: A co-signer with good credit can significantly improve your chances of approval and secure a better interest rate. The co-signer essentially guarantees the loan if you default.

- Subprime Lenders: These lenders specialize in working with borrowers who have lower credit scores, though their interest rates will be higher to compensate for the increased risk.

- Consider a Less Expensive Car: A lower loan amount generally means easier approval.

- Build Your Credit First: If possible, take some time to improve your credit score before applying. Even small improvements can make a difference.

- Realistic Expectations: Be prepared for higher interest rates and potentially less flexible terms. The goal is to get a loan you can comfortably afford, make timely payments, and use it as an opportunity to rebuild your credit.

Advice for First-Time Car Loan Applicants

First-time buyers often lack a substantial credit history, which can be a hurdle. Lenders have less data to assess your risk.

- Building Credit: Start by establishing a basic credit history before applying for a car loan. This could involve a secured credit card or being added as an authorized user on a trusted family member’s credit card.

- Smaller Loan: Consider starting with a more affordable, reliable used car. This reduces the loan amount and makes approval easier.

- Co-signer: Similar to bad credit situations, a co-signer can greatly assist first-time buyers in securing a personal car loan.

- Demonstrate Stability: Highlight any consistent employment history, proof of residence, and a stable income to show responsibility, even without a long credit history.

Post-Approval: What Happens Next?

Congratulations, your personal car loan has been approved! While the major hurdle is cleared, there are a few final steps to complete before you can drive off into the sunset.

Finalizing the Loan Agreement

Carefully review the final loan agreement. This document will detail the exact loan amount, interest rate (APR), loan term, monthly payment, and any fees. Ensure all the terms match what you discussed and agreed upon. This is your last chance to ask questions and clarify any uncertainties. Once signed, this is a legally binding contract.

Insurance Requirements

Lenders almost always require you to have comprehensive and collision insurance on your financed vehicle. This protects their investment (the car) in case of an accident, theft, or damage. You’ll typically need to provide proof of insurance before the loan can be finalized and the car released to you. Obtain quotes from several insurance providers to find the best coverage at the most competitive price.

Registration and Titling

Once the personal car loan is finalized and the car purchased, the dealership (or you, depending on state laws) will handle the vehicle’s registration with your state’s Department of Motor Vehicles (DMV) or equivalent agency. The title of the car, which proves ownership, will typically be held by the lender until the loan is fully paid off. You will receive a lien release once the loan is satisfied, and then a clear title.

Pro Tips for a Smooth Car Loan Journey

Securing a personal car loan can be straightforward with the right approach. Here are some final professional tips to ensure your experience is as smooth and advantageous as possible.

- Negotiate the Car Price Separately: Always negotiate the purchase price of the car first, before discussing financing. If you intertwine the two, you might get a good deal on the loan but overpay for the car, or vice versa. Keep these two transactions distinct.

- Consider Refinancing Options Later: If your credit score improves significantly after you’ve taken out your initial personal car loan, or if interest rates drop, you might be able to refinance your loan for a lower interest rate. This could save you a substantial amount of money over the remaining loan term. It’s always worth exploring.

- Read the Fine Print Thoroughly: We cannot emphasize this enough. Every single clause in your loan agreement matters. Understand fees, payment schedules, and what happens in case of late payments. Don’t let excitement overshadow due diligence.

- Don’t Be Afraid to Walk Away: If a deal doesn’t feel right, if the terms are not what you expected, or if you feel pressured, be prepared to walk away. There are always other cars and other lenders. Patience and a willingness to say no are powerful tools in car buying.

- Educate Yourself Continuously: The more you know about personal finance and car loans, the better decisions you’ll make. A great resource for general financial literacy is the Consumer Financial Protection Bureau (CFPB) at .

Drive Away with Confidence

Securing a personal car loan doesn’t have to be an intimidating process. By understanding the different types of lenders, meticulously preparing your finances, leveraging the power of pre-approval, and carefully navigating the application, you can position yourself for success. Remember to compare offers, read the fine print, and always prioritize what’s best for your financial health.

With this comprehensive guide, you now have the knowledge to approach your car loan journey with confidence and clarity. Go forth, secure that ideal personal car loan, and enjoy the open road in your new vehicle!