Your Ultimate Guide to Securing a Westlake Car Loan: Drive Your Dreams, Even with Challenged Credit

Your Ultimate Guide to Securing a Westlake Car Loan: Drive Your Dreams, Even with Challenged Credit Carloan.Guidemechanic.com

Are you dreaming of a new set of wheels but facing hurdles with traditional lenders? For many, the path to car ownership can feel complicated, especially when past financial challenges or a limited credit history stand in the way. This is where specialized lenders like Westlake Financial Services step in, offering a vital bridge for those seeking auto financing.

Securing a Westlake Car Loan isn’t just about getting approved; it’s about understanding the process, knowing what to expect, and empowering yourself with the right information. As an expert in auto financing, I’ve seen firsthand how Westlake provides opportunities for individuals who might otherwise be turned away. This comprehensive guide will demystify the entire journey, helping you navigate the world of Westlake auto loans with confidence and clarity.

Your Ultimate Guide to Securing a Westlake Car Loan: Drive Your Dreams, Even with Challenged Credit

What Exactly is Westlake Financial Services?

Westlake Financial Services is a prominent player in the auto financing industry, specializing in what’s often referred to as "subprime" lending. This means they primarily work with individuals who have less-than-perfect credit scores, limited credit history, or unique financial situations that traditional banks might deem too risky. They understand that life happens, and a credit score doesn’t always tell the whole story.

Based on my experience in the automotive finance sector, Westlake serves a crucial segment of the market. They partner with thousands of dealerships across the United States, providing them with the tools and resources to offer financing solutions to a wider range of customers. Their business model is built on assessing a broader set of criteria beyond just a FICO score, looking at the complete financial picture of an applicant.

Their focus isn’t just on providing loans; it’s also about helping customers establish or rebuild their credit. By making consistent, on-time payments on a Westlake Car Loan, you can significantly improve your credit profile over time, opening doors to better financial opportunities in the future. This makes them a valuable option for many looking to get back on track.

Understanding Westlake Car Loans: The Core Offering

When you consider a Westlake Car Loan, you’re looking at a financing product designed with flexibility in mind. Unlike prime lenders who cater almost exclusively to those with excellent credit, Westlake structures its loans to accommodate varying degrees of risk. This often translates into tailored terms that reflect an applicant’s specific financial situation.

Their primary offering is direct-to-dealer financing. This means you won’t typically apply directly to Westlake as a consumer. Instead, you’ll work with a dealership that is part of Westlake’s extensive network. The dealership acts as the intermediary, submitting your application to Westlake and other potential lenders.

Pro tips from us: Always communicate openly with your dealer about your financial situation. They can better match you with a lender like Westlake if they have all the necessary information. This partnership approach ensures that the financing process is streamlined and efficient for both you and the dealer.

Who Is a Westlake Car Loan For? The Ideal Candidate Profile

So, who exactly benefits most from a Westlake Car Loan? The ideal candidate for Westlake Financial Services typically falls into one of several categories, all revolving around challenging credit circumstances. They are designed for individuals who might have faced financial setbacks but are now stable and ready to commit to a car payment.

Firstly, individuals with bad credit are a primary focus. This could be due to past bankruptcies, repossessions, defaults, or a history of late payments. Westlake understands that these events don’t necessarily define your current ability to pay. They look for signs of recovery and current financial stability.

Secondly, those with no credit history are also strong candidates. Young adults just starting out, or recent immigrants, often haven’t had the chance to build a credit score. Westlake provides a starting point, recognizing that everyone needs a chance to establish credit. A Westlake Car Loan can be that first major step.

Finally, individuals with limited credit – perhaps only a few credit cards or a single small loan – can also find success. Their credit profile might not be robust enough for prime lenders, but Westlake is willing to consider their potential. They examine current income, employment stability, and debt-to-income ratio closely.

The Application Process: A Step-by-Step Walkthrough

Securing a Westlake Car Loan primarily begins at the dealership. It’s a straightforward process, but being prepared can significantly smooth out the experience. Understanding each step ensures you approach it with confidence and clarity.

-

Find a Participating Dealership: Westlake partners with thousands of dealerships nationwide. Your first step is to find a dealership in your area that works with Westlake Financial. You can often inquire directly with the dealership or check Westlake’s website for a dealer locator.

-

Choose Your Vehicle: Once at the dealership, you’ll select a vehicle that fits your needs and budget. The type, age, and mileage of the car can influence your loan approval and terms, especially for subprime lending. Dealers will guide you toward vehicles that are more likely to be approved by lenders like Westlake.

-

Complete the Credit Application: The dealership will have you fill out a credit application. This form gathers essential personal and financial information. Be thorough and accurate; any discrepancies can cause delays or even rejection.

-

Provide Required Documentation: This is a critical step. Common documents requested include:

- Proof of income (recent pay stubs, bank statements, or tax returns).

- Proof of residence (utility bill, lease agreement).

- Proof of identity (driver’s license, state ID).

- Proof of insurance (you’ll need full coverage before driving off the lot).

- References (sometimes required).

- Your down payment (if applicable).

-

Dealer Submits Application: The dealership will then submit your application to Westlake Financial Services, along with other potential lenders. Westlake uses its proprietary algorithms to assess your creditworthiness based on the information provided. They look beyond just your credit score, evaluating your income stability, employment history, and debt-to-income ratio.

-

Receive Loan Decision: Westlake typically provides a decision relatively quickly, often within minutes or hours. The dealer will then present you with the loan offer, outlining the approved amount, interest rate, and loan term.

Common mistakes to avoid are incomplete applications or failing to bring all necessary documents. This can significantly slow down the approval process. Always double-check what’s required before you head to the dealership. For more tips on preparing your documents, you might find our article on Getting Your Documents Ready for Auto Loan Approval helpful.

Factors Influencing Your Westlake Car Loan Approval

While Westlake is known for lending to those with challenged credit, approval isn’t guaranteed. Several key factors play a significant role in their decision-making process. Understanding these can help you strengthen your application and increase your chances of securing a Westlake Car Loan.

- Credit Score and History: Even if your credit score is low, Westlake will still review your credit report. They look for patterns, recent delinquencies, and any positive payment history you might have. A recent bankruptcy or repossession might not be an automatic disqualifier if you can show stability since then.

- Income and Employment Stability: This is paramount. Westlake needs assurance that you have a consistent and verifiable source of income to make your monthly payments. They typically look for stable employment, often preferring a minimum period of time at your current job. Proof of income is crucial here.

- Down Payment: A significant down payment can dramatically improve your chances of approval and secure better terms. It shows Westlake your commitment to the loan and reduces their risk. Even a modest down payment can make a difference, especially for those with less-than-perfect credit.

- Vehicle Choice: The car you choose matters. Westlake, like most lenders, has guidelines regarding the age, mileage, and value of the vehicle they will finance. Older, high-mileage vehicles are generally considered riskier. Choosing a reasonably priced, newer used car often leads to better approval odds.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. Westlake will assess your DTI to ensure you aren’t overextending yourself. A lower DTI indicates you have more disposable income to cover new loan payments, making you a more attractive borrower.

Based on my experience, highlighting your strengths in these areas during the application process can be incredibly beneficial. If you have a stable job and can offer a decent down payment, make sure those points are emphasized.

Navigating Interest Rates and Loan Terms

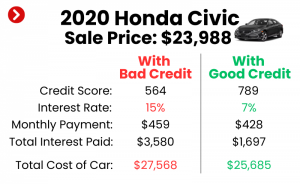

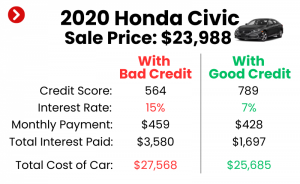

One of the most important aspects of any Westlake Car Loan is understanding the interest rate and loan terms. Because Westlake primarily works with subprime borrowers, their interest rates are generally higher than what prime lenders offer to those with excellent credit. This higher rate compensates for the increased risk they undertake.

Several factors will influence your specific interest rate:

- Your Credit Profile: The severity of your credit challenges will directly impact the rate. A slightly blemished credit history will likely get a better rate than someone with a recent bankruptcy.

- Down Payment Amount: As mentioned, a larger down payment reduces the loan amount and the lender’s risk, often leading to a slightly lower interest rate.

- Loan Term: Shorter loan terms (e.g., 36 or 48 months) typically come with lower interest rates but higher monthly payments. Longer terms (e.g., 60 or 72 months) have lower monthly payments but often accrue more interest over the life of the loan and may have slightly higher rates.

- Vehicle Characteristics: The age and mileage of the car can also play a role, with newer, lower-mileage vehicles sometimes qualifying for slightly better rates.

Pro tips from us: Always focus on the total cost of the loan, not just the monthly payment. A lower monthly payment over a longer term might seem appealing, but you could end up paying significantly more in interest over time. Ask your dealer for multiple term options to compare.

Improving Your Chances of Westlake Car Loan Approval

While Westlake is accessible, taking proactive steps can significantly bolster your application. Don’t leave your approval to chance; empower yourself with preparation.

-

Check Your Credit Report: Obtain free copies of your credit report from AnnualCreditReport.com. Review them for errors and dispute any inaccuracies. Even a small correction can positively impact your score. Understanding your current standing is the first step.

-

Save for a Down Payment: This is arguably the most impactful step you can take. A down payment, even a modest one (e.g., 10-20% of the vehicle price), reduces the amount you need to finance. It signals financial responsibility to the lender and lowers their risk, making you a more attractive borrower.

-

Know Your Budget: Before you even step into a dealership, determine how much you can realistically afford for a monthly car payment, including insurance and fuel. Stick to this budget to avoid financial strain later.

-

Consider a Co-signer: If your credit is particularly challenged, a co-signer with good credit can significantly increase your chances of approval and potentially secure a better interest rate. Ensure both parties understand the responsibilities involved, as the co-signer is equally liable for the loan.

-

Be Prepared with Documents: As detailed in the application process, having all your necessary documents organized and ready will streamline the process. This includes proof of income, residency, and identification.

Common mistakes to avoid are applying for too many loans at once, which can negatively impact your credit score. Also, don’t try to hide financial issues; honesty with the dealer can help them find the best solution for you. For more in-depth advice on managing your credit, you can consult resources like the Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov.

Life After Approval: Managing Your Westlake Loan

Congratulations, you’ve secured your Westlake Car Loan and are now driving your new vehicle! The journey doesn’t end here; in fact, this is where a significant opportunity begins. Managing your loan responsibly can have a profound positive impact on your financial future.

Making your payments on time, every time, is paramount. Westlake reports your payment history to major credit bureaus. Consistent, on-time payments will gradually build and improve your credit score, demonstrating your reliability as a borrower. This positive payment history is a powerful tool for rebuilding credit.

Westlake offers various payment options, including online portals, automatic deductions, and phone payments. Familiarize yourself with their system and choose the method that best suits you to avoid missed payments. Set up reminders if necessary.

As your credit improves over time (typically after 12-18 months of perfect payments), you might explore the option of refinancing your Westlake Car Loan. Refinancing with a prime lender could potentially secure you a lower interest rate, reducing your overall cost of borrowing and lowering your monthly payments. This is a common strategy for those who used a subprime loan to rebuild their credit. For more details on this, check out our guide on Refinancing Your Auto Loan for Better Rates.

Pros and Cons of a Westlake Car Loan

Like any financial product, a Westlake Car Loan comes with its own set of advantages and disadvantages. A balanced perspective is crucial for making an informed decision.

The Advantages: Opening Doors to Car Ownership

- Access for Challenged Credit: The most significant benefit is the opportunity for individuals with bad credit, no credit, or limited credit to secure auto financing. Westlake fills a critical gap that traditional lenders often leave open.

- Credit Building Opportunity: For those looking to improve their credit score, a Westlake loan can be an excellent tool. Consistent on-time payments are reported to credit bureaus, positively impacting your credit history and score. This can pave the way for better financial products in the future.

- Wide Dealership Network: Westlake partners with a vast network of dealerships, making it relatively easy to find a dealer who can process your application. This accessibility simplifies the car-buying process for many.

- Streamlined Application: The application process is typically efficient, with quick approval decisions, allowing you to drive away in your new car sooner.

The Disadvantages: Considerations to Keep in Mind

- Higher Interest Rates: Due to the increased risk associated with subprime lending, Westlake Car Loans generally come with higher interest rates compared to prime loans. This means you’ll pay more in interest over the life of the loan.

- Stricter Loan Terms: You might encounter stricter terms, such as specific requirements for vehicle age or mileage, and potentially a higher down payment requirement.

- Total Cost of Loan: While monthly payments might be manageable, the higher interest rates can significantly increase the total amount you pay for the vehicle over the loan term. It’s vital to calculate this total cost before committing.

- Potential for Dealer Markups: In some subprime lending scenarios, there might be opportunities for dealers to mark up interest rates beyond the initial approval from the lender. Always scrutinize your loan agreement carefully.

Understanding these pros and cons allows you to weigh the immediate benefit of vehicle ownership against the long-term financial implications. For many, the benefits of gaining reliable transportation and rebuilding credit outweigh the higher costs, especially if they plan to refinance later.

Conclusion: Driving Forward with Your Westlake Car Loan

Navigating the world of auto financing, particularly with challenged credit, can feel daunting. However, a Westlake Car Loan offers a powerful solution for many individuals looking to secure reliable transportation and simultaneously build a stronger financial future. By understanding Westlake’s role, preparing diligently, and managing your loan responsibly, you can transform a seemingly impossible goal into a tangible reality.

This article has provided an in-depth look at everything from who Westlake is and their application process, to critical factors influencing approval, and how to manage your loan effectively. Remember, knowledge is your most valuable asset when it comes to financial decisions. Armed with this comprehensive information, you are now well-equipped to approach the dealership and pursue a Westlake Car Loan with confidence.

Don’t let past financial bumps in the road define your future. Take the wheel, make informed choices, and drive towards your dreams today.