Your Ultimate Guide to Securing Auto Loans for First-Time Car Buyers

Your Ultimate Guide to Securing Auto Loans for First-Time Car Buyers Carloan.Guidemechanic.com

The thrill of buying your very first car is an unforgettable milestone. It represents freedom, independence, and a new chapter in life. However, for many first-time car buyers, the excitement can quickly turn into anxiety when it comes to understanding and securing an auto loan. The world of financing can seem complex, filled with jargon and daunting decisions.

But what if we told you it doesn’t have to be? This comprehensive guide is specifically designed for you, the first-time car buyer, to demystify the auto loan process. We’ll walk you through every step, from preparing your finances to driving off the lot with confidence, ensuring you get the best deal possible. Our goal is to empower you with knowledge, turning a potentially overwhelming experience into an exciting journey toward car ownership.

Your Ultimate Guide to Securing Auto Loans for First-Time Car Buyers

I. The Foundation: Preparing for Your First Auto Loan

Before you even start browsing car models or stepping onto a dealership lot, the most crucial step is preparation. Laying a solid financial foundation will not only make the loan application smoother but also significantly improve your chances of securing favorable terms. Based on my experience, skipping this stage is one of the most common mistakes first-time buyers make, leading to higher interest rates and buyer’s remorse.

A. Understanding Your Credit Score (or Lack Thereof)

Your credit score is essentially your financial report card. Lenders use it to assess your creditworthiness – how likely you are to repay borrowed money. For first-time car buyers, this can be a particular challenge because you might have little to no credit history.

1. What is a Credit Score and Why It Matters

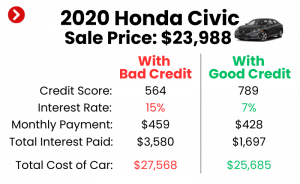

A credit score is a three-digit number, typically ranging from 300 to 850. A higher score indicates lower risk to lenders, often translating to better interest rates and loan terms. It’s built on factors like your payment history, the amount of debt you owe, the length of your credit history, and new credit applications. Lenders will heavily scrutinize this number when evaluating your auto loan application.

2. No Credit History? Strategies for Building One

If you’re a first-time buyer with no credit, don’t despair. Many people start from this position. Pro tips from us include opening a secured credit card, which requires a deposit that acts as your credit limit, or becoming an authorized user on a trusted family member’s credit card. These methods can help establish a payment history, which is vital for building a score. Even a small personal loan, paid diligently, can kickstart your credit profile.

3. Getting Your Credit Report

It’s imperative to know where you stand. You are entitled to a free credit report from each of the three major credit bureaus (Experian, Equifax, TransUnion) once every 12 months. Reviewing your report allows you to check for errors and understand your financial footprint. You can access these reports through AnnualCreditReport.com, a site authorized by federal law. (For more detailed information on understanding your credit report, we recommend checking resources from reputable financial institutions like the Consumer Financial Protection Bureau.)

B. Budgeting Like a Pro: What Can You Truly Afford?

Many first-time car buyers focus solely on the monthly car payment. However, the true cost of car ownership extends far beyond that single number. A realistic budget is your compass in this journey.

1. Beyond the Monthly Payment: Insurance, Maintenance, Fuel

When budgeting, consider all associated costs. Car insurance is mandatory and can be surprisingly high for new drivers or certain car models. Factor in fuel costs, which vary based on your commute and the car’s fuel efficiency. Don’t forget routine maintenance (oil changes, tire rotations) and potential repairs. These often overlooked expenses can quickly strain your budget if not accounted for.

2. The 20/4/10 Rule (or Similar Guideline)

A popular guideline for car affordability is the "20/4/10" rule. This suggests making a 20% down payment, financing the car for no more than four years (48 months), and ensuring your total monthly car expenses (payment, insurance, fuel) don’t exceed 10% of your gross monthly income. While a guideline, it provides a healthy framework for responsible spending. Adhering to such principles, based on my experience, prevents many buyers from becoming "car poor."

3. Calculating Your Debt-to-Income Ratio

Lenders look at your debt-to-income (DTI) ratio, which is the percentage of your gross monthly income that goes towards debt payments. A lower DTI indicates you have more disposable income to cover new loan payments. Aim for a DTI below 40% to demonstrate financial stability, although many lenders prefer it to be even lower, around 36% or less.

C. Saving for a Down Payment: Your Secret Weapon

A down payment is the initial amount of money you pay upfront for the car, reducing the amount you need to borrow. For first-time car buyers, especially those with limited credit, a substantial down payment is incredibly beneficial.

1. Why a Down Payment is Crucial for First-Timers

A larger down payment shows lenders your commitment and reduces their risk. This can often translate into a lower interest rate, as you’re financing less money. It also helps you avoid being "upside down" on your loan (owing more than the car is worth) early in ownership due to depreciation.

2. How Much to Aim For

While 20% is often recommended for new cars and 10% for used cars, any amount you can save will help. Even 5% can make a difference. The more you put down, the less you borrow, and the lower your monthly payments will be. It’s a direct way to save money over the life of the loan.

3. Impact on Interest Rates and Loan Terms

A significant down payment can directly influence the interest rate you’re offered. Lenders see you as a less risky borrower, making them more willing to offer competitive terms. Furthermore, it might allow you to choose a shorter loan term, which saves you a considerable amount in interest over time.

II. Navigating the Loan Landscape: Where to Find Financing

Once your financial foundation is set, the next step is to explore your financing options. You have several avenues for securing an auto loan, each with its own advantages and disadvantages. Understanding these will help you make an informed decision that best suits your financial situation.

A. Banks and Credit Unions: The Traditional Route

For many, local banks and credit unions are the go-to for loans. They offer a reliable and often competitive option, especially if you have an existing relationship.

1. Benefits: Often Better Rates, Established Relationships

Banks and credit unions, particularly credit unions, are known for offering some of the most competitive interest rates. If you’re an existing customer, your bank may offer you special deals or a smoother application process. Credit unions, being member-owned, often prioritize lower rates and better service for their members.

2. Process: Pre-Approval Importance

Applying for pre-approval from a bank or credit union before you visit a dealership is a smart move. It gives you a clear understanding of how much you can borrow, at what interest rate, and under what terms. This allows you to shop for a car with confidence, knowing your financing is already in place.

B. Dealership Financing: Convenience vs. Cost

Dealerships often offer their own financing options, acting as an intermediary between you and various lenders. This can be convenient, but it’s essential to approach it with caution.

1. "One-Stop Shop" Appeal

The primary advantage of dealership financing is convenience. You can shop for a car and secure a loan all in one place, which can save time. Dealerships work with multiple lenders, potentially finding you a deal, especially if you have a lower credit score.

2. Understanding Their Incentives and Potential Markups

Dealerships often have incentives to use their financing options. They might mark up the interest rate offered by the lender to earn a profit. While convenient, it’s crucial to compare their offer with your pre-approved loan to ensure you’re getting the best deal.

3. The "Finance Manager" Role

The finance manager at a dealership handles all the paperwork and loan finalization. They will present various financing options, extended warranties, and other add-ons. Be prepared to politely decline anything you don’t need or haven’t budgeted for.

C. Online Lenders: Speed and Comparison Shopping

The digital age has brought forth a plethora of online lenders, offering a modern approach to securing an auto loan. These platforms can be a powerful tool for comparison shopping.

1. Advantages: Quick Applications, Multiple Offers

Online lenders typically offer streamlined application processes that can be completed in minutes. Many platforms allow you to get multiple loan offers from different lenders by filling out a single application, making it easy to compare rates and terms from the comfort of your home.

2. Things to Watch Out For

While convenient, always ensure you’re dealing with reputable online lenders. Read reviews, check their accreditation, and be wary of any offers that seem too good to be true. Always compare their terms, including any origination fees, with traditional lenders.

III. The Application Process: Your Step-by-Step Guide

With your finances in order and an understanding of where to seek a loan, it’s time to tackle the application itself. This phase requires attention to detail and a clear understanding of what lenders are looking for.

A. Getting Pre-Approved: A Game Changer

Pre-approval is arguably the most valuable step in the car buying process for first-timers. It puts you in a powerful negotiating position.

1. What Pre-Approval Means and Its Benefits (Negotiating Power)

Pre-approval means a lender has reviewed your credit and financial information and tentatively agreed to lend you a certain amount of money at a specific interest rate, before you’ve even chosen a car. This acts like a cash offer at the dealership, giving you leverage to negotiate the car’s price without simultaneously negotiating financing terms. Based on my experience, dealers take pre-approved buyers more seriously.

2. Documents Needed for Pre-Approval

To get pre-approved, you’ll typically need to provide proof of income (pay stubs, tax returns), proof of residence (utility bill), identification (driver’s license), and your Social Security number. Having these documents ready will expedite the process.

3. Understanding the "Soft vs. Hard" Inquiry

When you check your own credit score or get pre-approved, it’s usually a "soft inquiry," which doesn’t affect your score. However, when you formally apply for a loan, the lender performs a "hard inquiry," which can temporarily ding your score by a few points. Multiple hard inquiries within a short period (typically 14-45 days, depending on the scoring model) for the same type of loan are usually grouped as one, so shop for rates within a concentrated timeframe.

B. Gathering Your Documents

Once you’re ready to apply, whether for pre-approval or the final loan, having all your paperwork organized is essential. This demonstrates professionalism and expedites the process.

1. Proof of Income, Residence, Identification

Ensure you have current pay stubs (usually the last two or three), bank statements, and potentially tax returns if you’re self-employed. A recent utility bill or rental agreement serves as proof of residence, and your driver’s license or state ID is necessary for identification.

2. Common Mistakes to Avoid

A common mistake is submitting incomplete or outdated documents. Double-check expiration dates on IDs and ensure income statements are recent. Another error is failing to disclose all existing debts, which can lead to delays or even loan denial if discrepancies are found. Transparency is key.

C. Understanding Loan Terms: Interest Rates, APR, and Loan Length

The terms of your loan are critical as they dictate the total cost of borrowing. It’s vital to understand what each component means for your wallet.

1. Fixed vs. Variable Interest Rates

Most auto loans come with a fixed interest rate, meaning your rate and monthly payment remain the same throughout the loan term. This provides predictability. Variable rates, while less common for auto loans, can fluctuate with market conditions, making your payments unpredictable. For first-time buyers, a fixed rate is generally recommended for stability.

2. The True Cost of APR

APR, or Annual Percentage Rate, is the total cost of your loan, expressed as a yearly percentage. It includes not only the interest rate but also any additional fees or charges associated with the loan. Always compare APRs, not just interest rates, as it gives you a more accurate picture of the loan’s true cost. A lower APR means you pay less overall.

3. Impact of Loan Term on Total Cost and Monthly Payments

The loan term is the length of time you have to repay the loan, typically ranging from 36 to 72 months. A shorter loan term means higher monthly payments but less interest paid over the life of the loan. Conversely, a longer term offers lower monthly payments but significantly increases the total interest you’ll pay. Based on my experience, many first-time buyers opt for longer terms to keep payments low, often unaware of the substantial extra cost over time.

IV. Choosing Your First Car: Smart Decisions

With your financing framework in place, you can now confidently select your first vehicle. This choice is more than just aesthetics; it’s about finding a reliable, affordable car that fits your lifestyle and budget.

A. New vs. Used: Weighing the Pros and Cons

One of the biggest decisions is whether to buy a new or used car. Each option presents distinct advantages and disadvantages, especially for first-time buyers.

1. Depreciation Factor

New cars depreciate rapidly, often losing 20-30% of their value in the first year alone. This means you could owe more than the car is worth very quickly. Used cars have already undergone this initial steep depreciation, offering better value for your money. For many first-time buyers, a quality used car is a financially smarter choice.

2. Reliability and Warranties

New cars come with factory warranties, providing peace of mind against unexpected repairs. Many certified pre-owned (CPO) used cars also come with warranties, though they might be shorter. Standard used cars might require you to purchase an extended warranty, or rely on your savings for repairs.

3. Affordability for First-Time Buyers

Given budget constraints and potential limited credit history, used cars are generally more affordable. Lower purchase prices mean smaller loans, which can lead to lower monthly payments and less interest paid overall, making them highly attractive for those new to car ownership.

B. Researching Car Models: Reliability and Resale Value

Once you decide between new and used, delve into specific models. Smart research goes beyond color and features.

1. Safety Ratings and Consumer Reviews

Prioritize safety. Check crash test ratings from organizations like the NHTSA and IIHS. Read consumer reviews on reliability and common issues for models you’re considering. Websites like Consumer Reports and J.D. Power are excellent resources.

2. Insurance Costs by Model

Insurance rates vary significantly by car model, even within the same brand. Sports cars, luxury vehicles, and certain popular models might have higher premiums due to repair costs or theft rates. Get insurance quotes for specific models before committing to a purchase to avoid an unwelcome surprise in your monthly budget.

C. The Test Drive and Inspection: Don’t Skip It!

This stage is non-negotiable. A thorough test drive and inspection are critical to ensuring you’re making a sound investment.

1. Beyond Aesthetics: Mechanical Checks

During the test drive, pay attention to more than just how it looks. Listen for unusual noises, check the brakes, test all lights and electronics, and ensure it handles smoothly at various speeds. Drive it on different types of roads if possible.

2. Independent Mechanic Inspection

For any used car, always, always, always get an independent pre-purchase inspection from a trusted mechanic. This small investment can save you thousands of dollars by uncovering hidden issues the dealer might not disclose. Common mistakes to avoid include trusting only the dealer’s inspection report.

V. Sealing the Deal: Negotiating and Finalizing

You’ve done your homework, secured pre-approval, and picked your car. Now it’s time for the final negotiation and paperwork. This is where your preparation truly pays off.

A. Negotiating the Car Price: Your Pre-Approval Advantage

Your pre-approval is your strongest negotiation tool. It allows you to focus solely on the car’s price, separate from the financing.

1. Separating Car Price from Loan Terms

When you have external financing ready, you can tell the dealer you’re pre-approved. This forces them to compete on the car’s price first, rather than confusing you with bundled payment offers that mix the car price, interest rate, and add-ons. Negotiate the lowest possible price for the vehicle itself. (For more advanced negotiation tactics, check out our guide on ‘Negotiating Car Prices Like a Pro’).

2. Being Prepared to Walk Away

The most powerful negotiation tactic is being willing to walk away if the deal isn’t right. There are always other cars and other dealerships. Don’t feel pressured into a purchase that doesn’t meet your budget or expectations. Patience often leads to better outcomes.

B. Understanding the Fine Print: Reading the Loan Agreement

Before you sign anything, meticulously read the entire loan agreement. This document legally binds you to the terms, so comprehending every detail is paramount.

1. Key Sections to Scrutinize

Pay close attention to the interest rate (APR), the total loan amount, the loan term, any fees (origination, documentation), and the total cost of the loan over its lifetime. Ensure these match what you agreed upon. Confirm the payment schedule and any penalties for late payments.

2. Beware of Add-ons and Hidden Fees

Dealerships often try to sell extended warranties, paint protection, GAP insurance (Guaranteed Asset Protection), or service packages. While some might be beneficial, many are overpriced or unnecessary. Politely decline anything you don’t want or haven’t researched. Ensure all "documentation fees" are legitimate and not excessive.

C. Insurance: A Non-Negotiable Requirement

You cannot drive off the lot without proof of insurance. Lenders require full coverage (collision and comprehensive) to protect their investment.

1. Types of Coverage

Understand the difference between liability (required by law, covers damage to others), collision (covers damage to your car in an accident), and comprehensive (covers non-collision damage like theft, vandalism, natural disasters). For a financed car, collision and comprehensive are typically mandatory.

2. Getting Quotes Before You Buy

Get several insurance quotes for the specific car you plan to buy before finalizing the purchase. This will give you an accurate estimate of your monthly or annual insurance costs, which is a significant part of your overall car budget. Different companies offer different rates for the same coverage, so shopping around can save you hundreds of dollars.

VI. Post-Purchase: Managing Your Auto Loan Responsibly

Congratulations, you’ve bought your first car! The journey doesn’t end here. Responsible loan management and vehicle maintenance are crucial for building good credit and protecting your investment.

A. Making Payments On Time: Building Good Credit

Your auto loan is a powerful tool for establishing or improving your credit history. Consistent, on-time payments are paramount.

1. Importance of Payment History

Payment history is the single most important factor in your credit score. Every on-time payment you make contributes positively to your credit report. Conversely, even a single late payment can significantly harm your score and stay on your report for years. This is your chance to prove you are a responsible borrower.

2. Setting Up Automatic Payments

To avoid missed payments, set up automatic payments from your bank account. This ensures your payment is always made on time, every time, without you having to remember. It’s a simple yet highly effective strategy for responsible loan management.

B. Refinancing Options: When and Why

Even after you’ve secured your first auto loan, you might have opportunities to improve its terms down the road. This is known as refinancing.

1. Improving Your Credit Score

If your credit score has significantly improved since you took out your initial loan (e.g., after 6-12 months of on-time payments), you might qualify for a lower interest rate. Refinancing means taking out a new loan to pay off your old one, ideally with better terms.

2. Lowering Interest Rates

Interest rates can fluctuate, and your personal financial situation can change. If market rates have dropped or your financial profile has strengthened, refinancing could lead to lower monthly payments or a reduced total cost of the loan. Always calculate if the savings outweigh any potential refinancing fees.

C. Maintaining Your Vehicle: Protecting Your Investment

Your car is a significant asset, and proper maintenance is key to its longevity and retaining its value. This directly impacts your financial well-being.

1. Regular Servicing

Follow the manufacturer’s recommended maintenance schedule. Regular oil changes, tire rotations, brake checks, and fluid top-ups are not just about keeping your car running smoothly; they prevent more expensive problems down the line. A well-maintained car is a reliable car.

2. Long-Term Cost Savings

While maintenance costs money, it’s an investment that saves you more in the long run. Neglecting routine service can lead to major breakdowns, expensive repairs, and a shorter lifespan for your vehicle. Protecting your asset ensures it serves you well and retains better resale value if you decide to upgrade in the future.

Conclusion

Embarking on the journey to buy your first car and secure an auto loan is a significant step. While it may seem daunting at first, remember that knowledge is your greatest asset. By understanding your credit, meticulously budgeting, exploring your financing options, diligently preparing your documents, and negotiating wisely, you’ve equipped yourself to make informed decisions.

Your first auto loan isn’t just about getting a car; it’s about building a foundation of financial responsibility that will benefit you for years to come. Drive away with confidence, knowing you’ve navigated the process like a pro. Keep making those payments on time, maintain your vehicle, and enjoy the freedom your first car brings. If you have more questions or want to delve deeper into specific topics, feel free to explore our other articles on car ownership and financial planning.