Your Ultimate Guide to Securing the Best Car Loan in Austin, TX

Your Ultimate Guide to Securing the Best Car Loan in Austin, TX Carloan.Guidemechanic.com

Austin, Texas – a vibrant city known for its unique culture, booming tech industry, and a lifestyle that often requires a reliable set of wheels. Whether you’re commuting to work, exploring the beautiful Texas Hill Country, or simply running errands, a car is often an essential part of life here. But for many, buying a car means navigating the often-complex world of Car Loan Austin options.

Securing the right auto financing can feel overwhelming, with countless lenders, varying interest rates, and a myriad of terms and conditions. As an expert in auto financing and a seasoned SEO content writer, my mission is to demystify this process for you. This comprehensive guide is designed to be your one-stop resource, offering deep insights, practical advice, and actionable strategies to help Austin residents find the absolute best car loan for their needs. We’ll cover everything from understanding the basics to advanced negotiation tactics, ensuring you drive away with confidence.

Your Ultimate Guide to Securing the Best Car Loan in Austin, TX

Understanding Car Loans in Austin: The Foundation

Before diving into the specifics of finding the best Car Loan Austin, it’s crucial to understand what a car loan actually is and the fundamental terms associated with it. Think of a car loan as a specialized installment loan designed specifically for vehicle purchases. A lender provides you with the funds to buy a car, and you agree to repay that amount, plus interest, over a predetermined period.

The Austin auto market is dynamic, reflecting the city’s rapid growth and diverse population. This means there’s a wide array of options, but also a need for informed decision-making. Knowing the basics empowers you to make smarter choices.

Key Terms You Need to Know

When discussing Austin car financing options, you’ll frequently encounter specific terminology. Understanding these terms is the first step to becoming a savvy borrower:

- Principal: This is the initial amount of money you borrow to purchase the car. It’s the cost of the vehicle minus any down payment or trade-in value.

- Interest Rate (APR): The Annual Percentage Rate (APR) represents the total cost of borrowing money, expressed as a yearly percentage. It includes the interest rate plus any fees charged by the lender. A lower APR means lower overall costs for your Car Loan Austin.

- Loan Term: This is the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, or 72 months). A longer term usually means lower monthly payments but higher total interest paid over the life of the loan.

- Down Payment: The upfront cash amount you pay towards the purchase of the car. A larger down payment can reduce your principal, lower your monthly payments, and often lead to better loan terms.

- Secured vs. Unsecured Loan: Most Austin auto financing is secured, meaning the car itself acts as collateral. If you default on the loan, the lender can repossess the vehicle. Unsecured loans, while rare for cars, are not backed by collateral.

Based on my experience, many first-time car buyers in Austin focus solely on the monthly payment. While important, it’s critical to consider the total cost of the loan over its entire term. A low monthly payment spread over many years can actually result in paying significantly more in interest.

Preparing for Your Austin Car Loan Journey

Preparation is key to securing the most favorable Car Loan Austin terms. Approaching lenders armed with knowledge and a clear financial picture will put you in a strong negotiating position. This involves assessing your financial health and understanding what you can realistically afford.

Your Credit Score: The Cornerstone of Car Loans

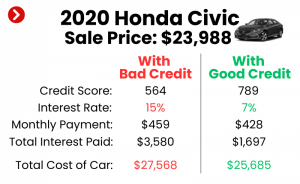

Your credit score is arguably the most significant factor lenders consider when evaluating your application for an Austin auto loan. It’s a three-digit number that reflects your creditworthiness based on your payment history, outstanding debts, length of credit history, and types of credit used.

- Checking Your Score: Before you even start looking at cars, obtain your credit report and score from all three major bureaus (Experian, Equifax, TransUnion). You can do this annually for free at AnnualCreditReport.com. Review it for any errors that could negatively impact your score.

- Improving Your Score: If your score isn’t where you want it to be, take steps to improve it. Pay down existing debts, especially credit card balances, and ensure all your bills are paid on time. Even small improvements can make a difference in the car loan rates Austin lenders offer you.

- Impact on Rates: Generally, the higher your credit score, the lower your interest rate will be. Lenders view borrowers with excellent credit as less risky, offering them the most competitive Austin car financing options.

Budgeting for Your New Ride: Beyond the Monthly Payment

Many people make the mistake of only budgeting for the monthly car payment. However, owning a car involves several other significant expenses. Pro tips from us include creating a comprehensive budget that accounts for everything:

- Insurance: Get quotes for car insurance before buying. Premiums vary widely based on the vehicle, your driving record, and where you live in Austin.

- Fuel Costs: Consider your daily commute and the car’s fuel efficiency. Gas prices can fluctuate.

- Maintenance: All cars require regular maintenance (oil changes, tire rotations) and occasional repairs. Factor these into your budget.

- Registration and Taxes: Don’t forget state registration fees and sales tax on the vehicle purchase. In Texas, sales tax on vehicles is 6.25% of the sales price.

- Parking: If you live or work in areas of Austin with paid parking, this can add up.

A good rule of thumb is that your total car-related expenses, including your loan payment, should not exceed 10-15% of your net monthly income. This ensures your Car Loan Austin doesn’t become a financial burden.

The Power of a Down Payment and Trade-In

A substantial down payment can significantly impact your Austin car loan.

- Reduced Principal: Less money borrowed means less interest paid over time.

- Lower Monthly Payments: A smaller loan amount directly translates to more manageable monthly installments.

- Improved Loan Terms: Lenders are often more willing to offer lower APRs to borrowers who put more money down, as it reduces their risk.

- Avoid "Upside Down" Status: A larger down payment helps prevent you from owing more on the car than it’s worth, a common situation known as being "upside down" or having negative equity.

If you have an existing vehicle, consider trading it in. The value of your trade-in can act as a down payment, reducing the amount you need to finance. Get an independent appraisal of your trade-in value before visiting dealerships to ensure you get a fair offer.

Navigating Austin Car Loan Options and Lenders

Austin residents have a multitude of options when it comes to securing Austin auto financing. Each type of lender has its own advantages and disadvantages. Understanding these can help you choose the best path for your specific needs.

Dealership Financing: Convenience at a Cost?

Many car buyers find it convenient to handle financing directly at the dealership. Dealerships work with a network of lenders and can often provide on-the-spot approvals.

- Pros: One-stop shopping, potential for special manufacturer incentives (low APRs or cash back), quick approval process.

- Cons: Less transparency, limited lender options compared to shopping independently, potential for markups on interest rates. Dealers might focus on monthly payments rather than the total cost of the loan.

Common mistakes to avoid are accepting the first offer presented by the dealership without comparing it to outside options. Always arrive at the dealership with a pre-approved loan in hand – even if you don’t use it, it gives you significant leverage.

Banks and Credit Unions: Often Your Best Bet for Car Loan Austin

For many Austin drivers, traditional banks and local credit unions offer some of the most competitive car loan rates Austin.

- Banks (e.g., Bank of America, Wells Fargo): Offer a wide range of loan products, established reputations, and often have online application processes.

- Credit Unions (e.g., Austin Telco Credit Union, University Federal Credit Union – UFCU): These member-owned financial institutions are renowned for their personalized service and often provide lower interest rates and more flexible terms than larger banks, especially for members. Membership requirements are usually easy to meet for Austin residents.

Pro tips from us suggest that credit unions are often overlooked but can be a goldmine for best car loans Austin. Their not-for-profit structure allows them to pass savings onto their members. I’d highly recommend exploring options with local Austin credit unions. You can often get pre-approved for an Austin auto loan before you even step foot on a dealership lot, strengthening your negotiating power.

Online Lenders: Speed and Comparison

The digital age has brought forth a plethora of online lenders specializing in auto loans. These platforms can offer convenience and the ability to compare multiple offers quickly.

- Pros: Easy application process from home, quick decisions, access to a broad network of lenders, competitive rates.

- Cons: Less personalized service, potential for scams if not using reputable sites, some may not offer local Austin support.

When using online lenders for your Car Loan Austin, always verify their credentials and read reviews. Look for lenders with transparent terms and good customer service.

Specialty Lenders: Navigating Bad Credit Car Loan Austin

If you have a less-than-perfect credit score, don’t despair. There are lenders who specialize in bad credit car loan Austin options.

- Subprime Lenders: These lenders cater to individuals with low credit scores or limited credit history. They understand that life happens, and aim to provide financing solutions.

- Buy Here, Pay Here Dealerships: While convenient, these dealerships typically offer very high interest rates and often have less transparency. Exercise extreme caution and only consider this as a last resort.

For more information on improving your credit before applying, check out our guide on Boosting Your Credit Score for a Car Loan. This can help you secure better terms for your Austin car loan.

Securing a Car Loan in Austin with Less-Than-Perfect Credit

Having a low credit score doesn’t automatically disqualify you from getting a Car Loan Austin. It simply means you’ll need to be more strategic and perhaps temper your expectations regarding interest rates. Many lenders in Austin understand that financial situations can be complex, and they offer solutions for those with challenging credit histories.

Is it Possible? Absolutely, With Considerations.

Yes, it is entirely possible to get a bad credit car loan Austin. However, it’s crucial to understand that these loans typically come with higher interest rates to offset the increased risk lenders take. Your focus should be on finding the most manageable terms available, rather than just getting approved.

Strategies for Bad Credit Car Loan Austin

If your credit score is a hurdle, consider these strategies to improve your chances and secure better terms:

- Larger Down Payment: As discussed, a substantial down payment signals to lenders that you are committed and reduces the loan amount they need to finance. This significantly mitigates their risk.

- Find a Co-signer: A co-signer with good credit can dramatically improve your chances of approval and help you secure a lower interest rate. The co-signer essentially guarantees the loan, taking on equal responsibility if you default. Choose someone you trust and who understands the commitment.

- Choose a Less Expensive Vehicle: Opting for a more affordable used car rather than a brand-new one will reduce the total amount you need to borrow, making the loan more attainable and less risky for lenders.

- Shop Around: Even with bad credit, it’s vital to get quotes from multiple lenders. Don’t settle for the first offer. Compare terms, rates, and fees carefully. Some credit unions or specialized lenders might be more accommodating.

- Show Proof of Income Stability: Lenders want to see that you have a stable job and consistent income to repay the loan. Provide thorough documentation of your employment history and income.

Based on my experience, for individuals seeking bad credit car loan Austin, demonstrating stability in employment and residence can often compensate somewhat for a lower credit score. Lenders look at the whole picture, not just one number.

Rebuilding Credit Through an Auto Loan

Successfully managing a Car Loan Austin, even one with a higher interest rate due to bad credit, can be an excellent way to rebuild your credit history. Making timely payments consistently shows financial responsibility. Over time, as your credit score improves, you might even consider refinancing your car loan for a lower interest rate, saving you money in the long run.

The Application Process: Your Step-by-Step Guide for Austin Residents

Once you’ve done your homework, budgeted wisely, and explored your options, it’s time to tackle the application process for your Austin auto loan. This stage requires meticulous attention to detail and a proactive approach.

Gathering Your Documents

Lenders will require various documents to verify your identity, income, and financial stability. Having these ready in advance will streamline the process.

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Recent pay stubs (typically 1-2 months), W-2s, tax returns (if self-employed), or bank statements.

- Proof of Residency: Utility bill, lease agreement, or mortgage statement with your Austin address.

- Social Security Number: For credit checks.

- Vehicle Information (if already chosen): VIN, make, model, year, mileage.

- Trade-in Information (if applicable): Title, registration, loan payoff amount.

Filling Out Applications and Understanding Offers

When applying for your Car Loan Austin, remember that each application typically results in a "hard inquiry" on your credit report. Multiple hard inquiries in a short period can slightly lower your score. However, credit bureaus usually treat multiple auto loan inquiries within a 14-45 day window as a single inquiry, recognizing that you’re rate shopping.

- Apply to Multiple Lenders: Apply to 3-5 lenders (banks, credit unions, online lenders) within that strategic window. This allows you to compare offers without significant credit score impact.

- Understand the Loan Offers: Don’t just look at the monthly payment. Scrutinize the APR, the loan term, and any associated fees (e.g., origination fees). A lower APR with a slightly higher monthly payment over a shorter term often saves you more money overall.

- Read the Fine Print: Before signing, carefully read the entire loan agreement. Ensure you understand every clause, including prepayment penalties (rare for auto loans but possible), late payment fees, and default clauses.

Based on my experience, the biggest mistake people make during the application phase is rushing. Take your time, ask questions, and don’t feel pressured to sign anything until you’re completely comfortable. This is particularly true when dealing with how to get a car loan in Austin that truly benefits you.

Negotiating the Best Deal

Having multiple pre-approved offers for your Car Loan Austin gives you immense negotiating power, especially at the dealership.

- Separate Car Price from Financing: Negotiate the price of the car first, as if you were paying cash. Once you’ve agreed on a vehicle price, then discuss financing.

- Leverage Your Pre-approvals: Present the dealership with your best pre-approved loan offer. They may be able to beat it or match it, as they want your business.

- Be Prepared to Walk Away: If you don’t feel you’re getting a fair deal on either the car or the financing, be prepared to leave. There are many dealerships and lenders in Austin.

Beyond the Loan: Important Considerations for Austin Drivers

Securing your Car Loan Austin is a significant milestone, but your responsibilities and opportunities don’t end there. There are several other crucial aspects to consider to protect your investment and optimize your financial situation.

Insurance Requirements

In Texas, liability insurance is legally required for all drivers. However, if you have a Car Loan Austin, your lender will almost certainly require you to carry full coverage insurance (collision and comprehensive). This protects their investment in the event of an accident, theft, or other damage.

- Shop for Insurance: Just like car loans, insurance rates vary widely. Get quotes from multiple providers before finalizing your purchase.

- Understand Coverage: Know what your policy covers and your deductible amounts.

- GAP Insurance: Consider Guaranteed Asset Protection (GAP) insurance. If your car is totaled and you owe more on the loan than the car’s actual cash value, GAP insurance covers the difference. This is especially relevant if you made a small down payment or have a long loan term.

Refinancing Options in Austin

Even if you secured a Car Loan Austin with a higher interest rate due to initial credit challenges, you’re not stuck with it forever. Refinancing your auto loan can be a smart financial move.

- When to Refinance: Consider refinancing if your credit score has improved significantly since you took out the original loan, if interest rates have dropped, or if you want to change your loan term (e.g., shorten it to save on interest or lengthen it to lower monthly payments).

- How it Works: You apply for a new loan to pay off your existing one. If approved for a lower APR, you’ll save money over the life of the loan. Many Austin banks and credit unions offer competitive refinancing options.

For more detailed guidance on improving your financial standing and exploring refinancing, check out this helpful resource on consumer credit and loans from a trusted external source like the Consumer Financial Protection Bureau: CFPB Auto Loans.

Paying Off Your Loan Early

If your financial situation improves, you might consider paying off your Austin auto loan earlier than scheduled. This can save you a substantial amount in interest.

- Check for Prepayment Penalties: Most auto loans do not have prepayment penalties, but it’s always wise to confirm this in your loan agreement.

- Make Extra Payments: Even making one extra payment per year or adding a small amount to your monthly payment can significantly reduce the total interest paid and shorten your loan term.

Austin Specific Car Loan Advice and Resources

Austin’s unique economic landscape and community spirit offer distinct advantages when it comes to financing a car in Austin. Leveraging local resources can often lead to more personalized service and better deals.

Leveraging Local Austin Institutions

While national banks are always an option, exploring local Austin-based financial institutions can yield excellent results.

- Community Credit Unions: As mentioned earlier, Austin boasts excellent credit unions like Austin Telco Credit Union and University Federal Credit Union (UFCU). These institutions are often lauded for their member-centric approach, lower fees, and competitive Austin car loan rates. They frequently have special programs or more lenient criteria for local residents.

- Local Banks: Smaller, community-focused banks in Austin might also offer more flexible terms or a more personal touch than their larger national counterparts.

When seeking the best car loans Austin, don’t overlook these local gems. They often have a vested interest in supporting the local community and its residents.

Understanding Texas Auto Loan Regulations

While much of auto lending is federally regulated, states also have specific laws that protect consumers. In Texas, for instance, there are regulations concerning maximum interest rates for certain types of loans, disclosure requirements, and repossession laws.

- Disclosure Requirements: Lenders are legally required to provide you with a clear breakdown of all loan terms, including the APR, total interest paid, and total payment amount.

- Lemon Law: While not directly related to financing, Texas has a "Lemon Law" that protects consumers who purchase new vehicles with significant defects. Understanding your rights as a car owner in Texas is crucial.

For more insights into state-specific auto financing details, you might find our article on Navigating Texas Auto Regulations helpful. This can give you an edge in understanding your rights as you secure your Car Loan Austin.

Conclusion: Driving Forward with Confidence in Austin

Navigating the world of Car Loan Austin doesn’t have to be a daunting task. By arming yourself with knowledge, preparing thoroughly, and approaching the process strategically, you can secure favorable financing that aligns with your financial goals. From understanding the nuances of your credit score to comparing offers from diverse lenders, every step you take contributes to a smoother, more cost-effective car buying experience.

Remember, the ultimate goal isn’t just to get approved for a loan, but to secure an Austin auto loan that fits comfortably into your budget and helps you achieve your transportation needs without undue financial stress. Be patient, be diligent, and don’t hesitate to ask questions. With this comprehensive guide as your roadmap, you are well-equipped to make informed decisions and drive away in your perfect vehicle, confidently navigating the vibrant streets of Austin, Texas. Happy driving!