Your Ultimate Guide to Securing Used Car Loans in NC: Drive Away with Confidence

Your Ultimate Guide to Securing Used Car Loans in NC: Drive Away with Confidence Carloan.Guidemechanic.com

The open roads of North Carolina beckon, and for many, the dream of exploring its scenic beauty or simply navigating daily life hinges on owning a reliable vehicle. While a brand-new car might be out of reach for some, a quality used car offers an excellent, cost-effective alternative. However, the path to ownership often involves navigating the world of financing. This is where understanding Used Car Loans NC becomes absolutely critical.

Securing the right loan can make all the difference, transforming a potentially stressful process into a smooth journey towards your next set of wheels. This comprehensive guide is designed to equip you with all the knowledge, insights, and expert tips you need to confidently find, apply for, and secure the best used car loan in North Carolina. We’ll delve deep into every facet, ensuring you’re empowered to make informed decisions and drive away with a deal that truly benefits you.

Your Ultimate Guide to Securing Used Car Loans in NC: Drive Away with Confidence

Why a Used Car in NC Makes Smart Financial Sense

Choosing a used car over a new one is often a savvy financial decision, especially in a state like North Carolina where diverse vehicle options are plentiful. The primary advantage lies in depreciation. New cars lose a significant portion of their value the moment they’re driven off the lot.

A used car has already absorbed much of this initial depreciation, meaning your investment holds its value better over time. This can lead to lower purchase prices, which in turn means you’ll need to borrow less. A smaller loan amount directly translates to lower monthly payments and less interest paid over the life of the loan.

Furthermore, insurance costs are typically lower for used vehicles, providing additional savings. This combination of reduced purchase price, slower depreciation, and lower insurance premiums makes financing a used car an attractive option for budget-conscious buyers across North Carolina.

Understanding the Landscape of Used Car Loans NC

North Carolina offers a robust financial market, providing numerous avenues for securing a used car loan. It’s essential to recognize that not all loans are created equal, and the best option for you will depend on your individual financial situation. Familiarizing yourself with the different types of lenders is your first step.

You’ll encounter traditional banks, local credit unions, convenient online lenders, and even in-house financing options directly through dealerships. Each category presents its own set of advantages and considerations. Exploring all these options ensures you cast a wide net in your search for competitive Used Car Loans NC.

The Pre-Approval Advantage: Your Secret Weapon for Used Car Loans NC

One of the most powerful tools in your car buying arsenal is loan pre-approval. This isn’t just a suggestion; it’s a strategic move that can save you time, money, and stress. Pre-approval means a lender has reviewed your financial information and tentatively agreed to lend you a specific amount at a particular interest rate, before you even choose a car.

What is Pre-Approval and Why is it Crucial?

When you get pre-approved, you’re essentially getting a conditional commitment from a lender. They assess your creditworthiness and provide you with an offer, usually valid for a certain period, like 30 days. This process provides immense clarity on your purchasing power.

Armed with a pre-approval, you know exactly how much you can afford, which helps you narrow down your car search to vehicles within your budget. It transforms you from a hopeful buyer into a confident, ready-to-purchase customer.

Empowering Your Negotiation at the Dealership

Based on my experience, walking into a dealership with a pre-approved loan in hand changes the entire dynamic of the negotiation. Dealers understand you’re serious and that you have external financing readily available. This puts you in a much stronger position to negotiate the vehicle’s price, rather than just focusing on the monthly payment.

You can compare the dealership’s financing offer directly against your pre-approval. If the dealer can beat your pre-approved rate, fantastic! If not, you already have a solid financing option secured. This prevents you from being pressured into less favorable terms often presented by dealerships late in the buying process.

Pro Tips from Us: Shop for Rates First

Pro tips from us: Always shop around for pre-approval rates from multiple lenders – banks, credit unions, and online providers – before you even set foot on a car lot. Most lenders will allow you to get pre-approved with a "soft inquiry" on your credit, which doesn’t harm your score. Once you’re ready to commit, the "hard inquiry" will occur. Doing this within a short window (typically 14-45 days) counts as a single inquiry for scoring purposes, minimizing impact. This diligence ensures you’re getting the most competitive rates for your Used Car Loans NC.

Key Factors Affecting Your Used Car Loan NC

Several critical elements come into play when lenders evaluate your application for a used car loan in North Carolina. Understanding these factors will help you prepare and position yourself for the best possible financing terms. Each plays a significant role in determining your eligibility and the interest rate you’ll be offered.

Your Credit Score: The Cornerstone of Your Loan

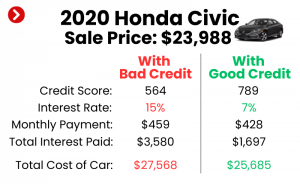

Your credit score is arguably the most influential factor in securing favorable Used Car Loans NC. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. Lenders use this score to assess the risk involved in lending you money.

Generally, FICO scores range from 300 to 850. A higher score signifies a lower risk to lenders, which typically translates to lower interest rates and better loan terms. Scores in the "excellent" (780+) and "good" (670-739) ranges will open doors to the most competitive offers. If your score is lower, don’t despair; options are still available, but understanding its impact is key.

The Power of a Down Payment

Making a substantial down payment can significantly improve your chances of securing a favorable used car loan. A larger down payment reduces the total amount you need to borrow, which in turn lowers your monthly payments and the overall interest you’ll pay over the life of the loan. It also signals to lenders that you’re a serious and responsible borrower, reducing their perceived risk.

Based on my experience, even a 10-20% down payment can make a noticeable difference in your loan terms. It creates immediate equity in the vehicle, making the loan more attractive to lenders. If possible, prioritize saving for a down payment before applying for Used Car Loans NC.

Loan Term: Balancing Monthly Payments and Total Cost

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A longer loan term means lower monthly payments, which can be appealing for budget management. However, it also means you’ll pay more in total interest over the life of the loan.

Conversely, a shorter loan term will result in higher monthly payments but significantly less interest paid overall. Carefully consider your budget and long-term financial goals when choosing a loan term. It’s a balance between affordability now and the total cost of ownership later.

Interest Rate (APR): What You’re Really Paying

The Annual Percentage Rate (APR) is the true cost of borrowing money. It includes not only the interest rate but also any additional fees charged by the lender, expressed as a yearly percentage. Comparing APRs from different lenders is crucial, as it provides a comprehensive picture of the loan’s cost.

Even a difference of one or two percentage points in APR can amount to hundreds, if not thousands, of dollars over the life of a used car loan. Always ask for the APR and use it as your primary comparison metric when evaluating offers for Used Car Loans NC.

Debt-to-Income Ratio: A Lender’s Perspective

Lenders also assess your debt-to-income (DTI) ratio, which compares your total monthly debt payments to your gross monthly income. This ratio helps them determine if you can comfortably afford additional debt. A lower DTI ratio indicates less financial strain and a greater ability to manage new loan payments.

While there isn’t a single universal threshold, most lenders prefer a DTI ratio of 36% or less, though some might go higher for auto loans if other factors are strong. Understanding your DTI can give you insight into how lenders view your financial capacity.

Navigating Different Credit Scenarios for Used Car Loans NC

Your credit score significantly influences the type of loan you can secure. However, regardless of your credit history, options are available for Used Car Loans NC. The key is to understand your standing and pursue the most appropriate strategies.

Excellent/Good Credit: Unlocking the Best Rates

If you boast an excellent or good credit score (typically 670 and above), you are in a prime position to secure the most competitive interest rates and favorable terms for your used car loan. Lenders view you as a low-risk borrower, eager to attract your business.

Focus on comparing pre-approved offers from various banks, credit unions, and online lenders. Don’t settle for the first offer; leverage your strong credit to negotiate for the absolute best APR available. You might also qualify for longer loan terms with attractive rates, giving you flexibility.

Fair/Average Credit: Strategies for Competitive Offers

For those with fair or average credit scores (typically in the 580-669 range), securing Used Car Loans NC is certainly possible, though the rates might not be as low as for those with excellent credit. This is where diligent research and strategic application become even more important.

Consider credit unions, which are often more forgiving and community-focused than large banks. Online lenders also specialize in various credit tiers and might offer competitive options. You might also improve your chances by making a larger down payment or opting for a slightly shorter loan term, which signals less risk to the lender.

Bad Credit Used Car Loans NC: Finding Your Path Forward

Having a low credit score (below 580) can make securing a used car loan more challenging, but it is by no means impossible in North Carolina. Bad credit used car loans NC exist, but they typically come with higher interest rates to offset the increased risk lenders take on. The goal here is to find a manageable loan that helps you rebuild your credit.

Options include seeking lenders who specialize in subprime auto loans, or working with a co-signer who has good credit. A co-signer essentially shares responsibility for the loan, making it less risky for the lender and potentially securing you a better rate. A larger down payment is also incredibly beneficial in this scenario.

Common mistakes to avoid are jumping at the first "guaranteed" approval without scrutinizing the terms. High-interest rates and predatory fees can trap you in a cycle of debt. Always read the fine print, understand the total cost, and ensure the monthly payments are genuinely affordable within your budget. Pro tips from us: If you’re in this situation, focus on securing a reliable car you can afford to pay off, and use this loan as an opportunity to consistently make on-time payments, which will gradually improve your credit score for future financial endeavors.

The Application Process: What You’ll Need

Once you’ve identified potential lenders and are ready to apply for your Used Car Loans NC, you’ll need to gather several key documents. Being prepared will streamline the process and prevent unnecessary delays. Lenders require this information to verify your identity, assess your financial stability, and confirm your ability to repay the loan.

Essential Documents for Your Loan Application

Typically, you’ll need the following:

- Proof of Identity: A valid government-issued ID, such as a driver’s license or state ID.

- Proof of Income: Recent pay stubs (typically 2-3 months), tax returns (if self-employed), or bank statements showing consistent deposits.

- Proof of Residence: Utility bills, lease agreements, or mortgage statements showing your current address in North Carolina.

- Social Security Number: For credit checks.

- Vehicle Information: Once you’ve chosen a car, you’ll need its VIN, mileage, and purchase price.

- Proof of Insurance: Lenders require full coverage insurance on the vehicle before finalizing the loan.

The process usually involves submitting your application, undergoing a credit check, and then receiving a loan offer. Once you accept, the closing process will finalize the paperwork and transfer funds.

Where to Find Your Used Car Loan NC: Lender Types in Detail

North Carolina offers a diverse range of lenders, each with unique characteristics that might appeal to different buyers. Understanding these options is key to finding the best fit for your Used Car Loans NC.

Banks: Traditional and Reliable

Major banks like Wells Fargo, Bank of America, and local North Carolina banks often provide competitive rates for borrowers with strong credit histories. They offer a sense of security and established processes. While they might be less flexible for those with challenging credit, their rates for well-qualified buyers are often very attractive. It’s worth checking with your current bank, as they might offer preferred rates to existing customers.

Credit Unions: Member-Focused and Competitive

Credit unions, such as State Employees’ Credit Union (SECU) or Coastal Credit Union, are non-profit financial cooperatives owned by their members. They are known for their personalized service and often offer more favorable interest rates and flexible terms than traditional banks, especially for used car loans. Membership is usually required, but it’s often easy to join by living or working in a specific area or being affiliated with certain organizations.

Internal Link Opportunity: For a deeper dive into securing the most competitive auto loan rates, consider exploring our comprehensive guide on .

Online Lenders: Speed and Convenience

Online lenders like Capital One Auto Finance, LightStream, or Carvana Auto Finance have revolutionized the car loan process with their speed and convenience. They allow you to apply, get approved, and sometimes even complete the entire car purchase online from the comfort of your home in NC. These platforms often cater to a wider range of credit scores and can be an excellent source for comparing multiple offers quickly. Their streamlined process makes them a popular choice for many modern car buyers.

Dealership Financing: One-Stop Shop

Many dealerships offer in-house financing, often referred to as "dealer-arranged financing." This can be convenient as it allows you to handle the car purchase and loan application all in one place. Dealerships work with a network of lenders and can sometimes offer promotional rates. However, it’s crucial to exercise caution here.

Pro tips from us: Always get an independent pre-approval from a bank or credit union before stepping into a dealership. This way, you have a benchmark to compare against any financing offers the dealer presents. Without a pre-approval, you might not know if the dealer’s rate is truly competitive or simply convenient. Don’t let the ease of a one-stop shop overshadow the importance of securing the best possible terms for your Used Car Loans NC.

Common Pitfalls and How to Avoid Them with Used Car Loans NC

Navigating the world of used car financing can have its traps. Being aware of common mistakes can help you steer clear of costly errors and ensure a smoother process for your Used Car Loans NC.

Not Getting Pre-Approved

As discussed, skipping pre-approval puts you at a significant disadvantage. You lose negotiation power and might settle for a higher interest rate offered by the dealership. Always secure external financing before you start serious car shopping.

Focusing Only on the Monthly Payment

While a low monthly payment is appealing, focusing solely on it can lead to longer loan terms and significantly more interest paid over time. Always consider the total cost of the loan, not just the individual monthly installment. A low payment on a 72-month loan might cost you much more than a slightly higher payment on a 48-month loan.

Ignoring the Total Cost of the Loan

Beyond the monthly payment, understand the total amount you will repay over the life of the loan, including principal and interest. Sometimes, a seemingly good deal can hide a much higher total cost due to a high APR or extended term. Always do the math.

Skipping a Pre-Purchase Inspection (PPI)

This isn’t directly a loan pitfall, but it’s a critical part of buying a used car that impacts your loan. Financing a lemon means you’re paying a loan for a car that constantly needs repairs. Always invest in a professional pre-purchase inspection by an independent mechanic before finalizing any used car purchase. It’s a small expense that can save you thousands.

Lack of Negotiation

Whether it’s the car’s price or the loan’s interest rate, negotiation is often possible. Don’t be afraid to haggle on the vehicle’s price and compare loan offers from different lenders to get the best deal. Everything is negotiable in the car buying process.

For more information on consumer protection when financing a vehicle, you can consult trusted resources like the Federal Trade Commission (FTC) at www.consumer.ftc.gov. They offer valuable advice on avoiding scams and understanding your rights.

Making Your Used Car Loan NC Work For You

Securing your used car loan is a significant step, but managing it effectively is equally important. Once the papers are signed and you’re driving your new-to-you vehicle, your focus shifts to responsible loan management.

Budgeting for Payments

Integrate your monthly car payment into your overall budget. Ensure it’s a comfortable amount that doesn’t strain your finances. Factor in other car-related expenses like insurance, fuel, maintenance, and potential repairs. Having a clear budget prevents financial stress and missed payments.

Understanding Your Loan Agreement

Read your loan agreement thoroughly. Understand the interest rate, the total amount to be repaid, any prepayment penalties (though these are less common with auto loans), and the due date for your payments. Knowledge of your terms empowers you to manage the loan effectively.

Early Payoff Options

If your financial situation improves, consider paying off your loan early. This can save you a substantial amount in interest. Check if your loan has any prepayment penalties – most auto loans do not, but it’s always wise to confirm. Even making extra payments when you can, or rounding up your monthly payment, can significantly reduce the loan term and total interest.

Refinancing Possibilities

If you secured your Used Car Loans NC with a less-than-ideal credit score or interest rate, or if market rates have dropped, refinancing might be an option. Refinancing involves taking out a new loan to pay off your existing one, ideally at a lower interest rate or with more favorable terms. This can save you money and potentially lower your monthly payments.

Internal Link Opportunity: To gain further control over your financial landscape, explore our detailed article on .

Conclusion: Drive Away with Confidence

Navigating the process of securing Used Car Loans NC doesn’t have to be a daunting task. By arming yourself with knowledge, understanding the various options, and adopting a strategic approach, you can confidently secure a loan that aligns with your financial goals and helps you get behind the wheel of your ideal used car.

Remember the pillars of smart financing: diligent research, the invaluable advantage of pre-approval, comparing offers from diverse lenders, and understanding every aspect of your loan. Avoid common pitfalls by focusing on the total cost, not just monthly payments, and always verifying the vehicle’s condition with a pre-purchase inspection. With these insights, you’re well-equipped to make informed decisions and enjoy the freedom of the open road across North Carolina. Start your research today, and embark on your journey to smart car ownership!