Your Ultimate Guide to Securing Your First Car Loan: A Comprehensive Walkthrough

Your Ultimate Guide to Securing Your First Car Loan: A Comprehensive Walkthrough Carloan.Guidemechanic.com

Buying your first car is an exhilarating milestone. It represents freedom, independence, and a significant step into adulthood. But for many, the path to ownership involves navigating the often-complex world of first time car loans. This isn’t just about picking a car; it’s about making a smart financial decision that impacts your future.

As an expert blogger and professional SEO content writer, I understand the questions and anxieties that come with this journey. My mission in this comprehensive guide is to demystify the process, providing you with unique, in-depth, and actionable insights. We’ll cover everything from preparing your finances to signing on the dotted line, ensuring you secure the best possible car loan for beginners. Let’s dive in and transform confusion into confidence!

Your Ultimate Guide to Securing Your First Car Loan: A Comprehensive Walkthrough

1. Laying the Foundation: Understanding What a Car Loan Truly Is

Before you even think about test drives, it’s crucial to grasp the fundamentals of a car loan. This isn’t just some abstract financial product; it’s a commitment that will be part of your monthly budget for years. Understanding its core components empowers you to make informed decisions.

What is a Car Loan?

At its simplest, a car loan is an agreement where a lender provides you with money to purchase a vehicle, and you agree to repay that money, plus interest, over a set period. The car itself typically serves as collateral, meaning if you fail to make your payments, the lender can repossess the vehicle. This is why most auto loans are considered "secured" loans.

Key Terms You Must Know

Navigating the loan landscape requires familiarity with its language. Here are the essential terms:

- Principal: This is the initial amount of money you borrow to buy the car. It’s the sticker price minus any down payment or trade-in value.

- Interest Rate: This is the cost of borrowing money, expressed as a percentage of the principal. A lower interest rate means you’ll pay less over the life of the loan.

- Annual Percentage Rate (APR): Often confused with the interest rate, the APR is a broader measure of the cost of borrowing. It includes the interest rate plus any additional fees or charges associated with the loan, such as origination fees. This gives you a more accurate picture of the total cost.

- Loan Term: This is the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A longer term usually means lower monthly payments but more interest paid overall.

- Down Payment: This is the upfront cash payment you make towards the purchase price of the car. A larger down payment reduces the amount you need to borrow, potentially leading to lower monthly payments and less interest.

Based on my experience, truly understanding these terms is the first, most critical step. Don’t let jargon intimidate you; arm yourself with this knowledge. It will be invaluable when comparing offers and negotiating.

2. Preparing for Success: Getting Your Finances in Order

Securing your first car loan isn’t a spontaneous act; it’s a strategic process that begins long before you step into a dealership. Preparation is key to getting favorable terms and avoiding common pitfalls.

How Much Can You Truly Afford? Beyond the Monthly Payment

Many first-time buyers make the mistake of focusing solely on the monthly payment. While important, it’s only one piece of the puzzle. You need to consider the total cost of car ownership.

Pro tip from us: Create a detailed budget that goes beyond just the loan payment. Think about:

- Car Insurance: This can be a significant expense, especially for new drivers or those with no driving history. Get quotes before you buy.

- Fuel Costs: Estimate your weekly or monthly fuel consumption based on your driving habits and local gas prices.

- Maintenance & Repairs: All cars need routine maintenance (oil changes, tire rotations) and eventually repairs. Factor in an emergency fund for unexpected issues.

- Registration & Taxes: These vary by state and can add a considerable upfront cost.

- Parking Fees: If you live in an urban area or work in a city, parking can be a recurring expense.

Common mistakes to avoid are underestimating these additional costs. A seemingly affordable monthly loan payment can quickly become unmanageable when combined with other car-related expenses. Aim for your total car expenses (loan, insurance, fuel, maintenance) to be no more than 15-20% of your net monthly income.

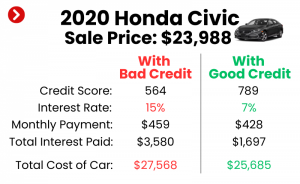

Your Credit Score: The Unseen Player

For a first time car loan with no credit history, this section is especially vital. Your credit score is a three-digit number that lenders use to assess your creditworthiness. A higher score indicates a lower risk, translating to better interest rates.

- Why it Matters: Lenders offer the best rates to borrowers with excellent credit (typically 700+). If you have no credit or a low score, you’ll likely face higher interest rates.

- How to Check It: You can get a free credit report from AnnualCreditReport.com once a year from each of the three major bureaus (Equifax, Experian, TransUnion). Many credit card companies and banks also offer free credit score monitoring.

- Tips for Building Credit:

- Secured Credit Card: These require a deposit, acting as your credit limit. Use it responsibly and pay it off in full each month.

- Become an Authorized User: If a trusted family member with good credit adds you to their credit card, their positive payment history can benefit your report.

- Small Installment Loan: A small personal loan, paid back consistently, can also help establish credit.

Even if you have no credit, don’t despair. Many lenders offer programs for car loan for beginners or those with limited credit history, though the terms might be less favorable initially. The goal is to start building a positive credit history as soon as possible.

Gathering Your Documents: Be Prepared

Lenders require specific documentation to verify your identity, income, and residency. Having these ready streamlines the application process.

You’ll typically need:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2 forms, or tax returns if self-employed.

- Proof of Residency: Utility bill, lease agreement, or mortgage statement.

- Social Security Number.

- Reference Contacts: Some lenders may ask for personal references.

Based on our years of helping people secure financing, having all your paperwork organized and accessible shows lenders you are responsible and serious, which can subtly work in your favor.

3. The Application Journey: From Pre-Approval to Driving Away

With your finances in order and documents ready, you’re prepared to embark on the actual loan application process. This stage involves strategic moves that can significantly impact your loan terms.

The Power of Pre-Approval: Your Secret Weapon

Pre-approval for a car loan is arguably the most crucial step for first-time buyers. It means a lender has provisionally agreed to lend you a certain amount of money at a specific interest rate, based on a preliminary review of your credit and finances.

Why it’s crucial for first-time buyers:

- Know Your Budget: You walk into the dealership knowing exactly how much you can afford, preventing you from falling in love with a car outside your price range.

- Negotiating Power: You become a cash buyer in the eyes of the dealership. This allows you to negotiate the car’s price separately from the financing, often leading to a better deal on the vehicle itself.

- Comparison Shopping: You can compare offers from multiple lenders without commitment. This ensures you’re getting the most competitive interest rate.

- Confidence: It removes much of the stress and uncertainty from the car-buying process.

Based on my experience in the automotive finance industry, pre-approval is a game-changer. It shifts the power dynamic from the dealership to you, the buyer. Don’t skip this step!

Choosing the Right Lender: Options Galore

You have several avenues for securing a car loan, each with its own advantages:

- Banks: Traditional banks are a common source. If you have an existing relationship with a bank, they might offer competitive rates or loyalty programs.

- Credit Unions: Often known for offering lower interest rates and more flexible terms than traditional banks, credit unions are an excellent option, especially for those with less-than-perfect credit.

- Online Lenders: Companies like LightStream, Capital One Auto Finance, and others offer convenient online applications and competitive rates. They can be a great option for comparing multiple offers quickly.

- Dealership Financing: While convenient, dealerships often mark up interest rates to earn a commission. They can be a good last resort, especially if you have challenging credit, but it’s best to have outside offers to compare against.

Pro tip: Apply for pre-approval with 2-3 different lenders (banks, credit unions, online) within a short window (typically 14-45 days, depending on the credit scoring model). This counts as a single "hard inquiry" on your credit report, minimizing the impact on your score while maximizing your chances of finding the best rate.

Negotiating the Best Deal: On the Car and the Loan

With your pre-approval in hand, you’re ready to negotiate. Remember, there are two separate negotiations: the price of the car and the terms of the loan.

- Negotiate the Car Price First: Since you have your own financing, focus solely on getting the lowest possible purchase price for the vehicle. Don’t mention your pre-approval until you’ve settled on the car price.

- Compare Financing Offers: Once you have a final car price, present your pre-approval offer to the dealership. They may try to beat it with their own financing options. Compare their offer (APR, loan term, monthly payment) to your pre-approved loan. Choose the one with the most favorable terms.

Common mistakes to avoid are letting the dealership "bundle" the car price and loan terms into one confusing monthly payment discussion. This makes it impossible to know if you’re getting a good deal on either. Stick to separate negotiations.

- For a deeper dive into smart negotiation tactics, explore our comprehensive guide:

4. Navigating the Minefield: Common Mistakes and How to Avoid Them

Even with preparation, the car loan process can present challenges. Being aware of common pitfalls will help you steer clear of costly errors.

Focusing Only on the Monthly Payment, Ignoring the APR

This is perhaps the most frequent mistake first time car loan applicants make. A low monthly payment can be enticing, but it often comes with a longer loan term (e.g., 72 or 84 months) and a higher overall cost due to more interest accumulating over time.

- Example: A $20,000 loan at 5% for 60 months might be $377/month. The same loan at 5% for 72 months might be $322/month. While the 72-month payment is lower, you’ll pay significantly more in total interest.

- Pro tip: Always compare the total cost of the loan (principal + total interest paid), not just the monthly payment. The APR gives you the best indicator of the true cost of borrowing.

Falling for Long Loan Terms

While longer loan terms (60+ months) result in lower monthly payments, they expose you to several risks:

- More Interest Paid: As mentioned, you pay significantly more interest over the life of the loan.

- Upside Down (Negative Equity): Cars depreciate quickly. With a long loan term, you might owe more on the car than it’s worth, especially in the early years. This is called being "upside down" or having "negative equity." If your car is totaled or stolen, insurance might not cover the full amount you owe, leaving you to pay the difference.

- Car Troubles Before Payoff: You might still be making payments on a car that’s experiencing major mechanical issues, or you might want to upgrade before the loan is paid off.

From our experience, aiming for the shortest loan term you can comfortably afford is always the wisest financial move.

Unnecessary Add-ons and Extras

Dealerships are experts at selling additional products and services. While some might offer value, many are overpriced or unnecessary.

Common add-ons include:

- Extended Warranties: Sometimes beneficial, but often marked up significantly. Research third-party options.

- GAP Insurance: This covers the "gap" between what you owe on your car and its actual cash value if it’s totaled. This is highly recommended if you make a small down payment or have a long loan term, but you can often get it cheaper from your own insurance company or a credit union.

- Rustproofing, Paint Protection, Fabric Protection: These are often high-profit items for dealerships and may not offer much long-term value, especially on newer vehicles with factory protection.

- VIN Etching: A deterrent for theft, but often overpriced.

Pro tip: Scrutinize every line item on the final purchase agreement. Ask for an explanation of anything you don’t understand and don’t be afraid to say "no" to add-ons you don’t want or need.

Not Reading the Fine Print

The loan agreement is a legally binding document. It’s imperative that you read and understand every clause before signing.

Look for:

- Prepayment Penalties: While rare in auto loans, some lenders charge a fee if you pay off your loan early.

- Late Payment Fees: Understand the grace period and associated charges.

- Default Clauses: What constitutes a default and the consequences.

- Assignment Clause: Can the lender sell your loan to another financial institution?

Common mistake to avoid is feeling rushed or intimidated into signing without fully understanding the terms. Take your time, ask questions, and if necessary, take the document home to review or have a trusted advisor look at it.

5. Beyond Approval: Managing Your First Car Loan Responsibly

Getting approved for your first car loan is a significant achievement, but the journey doesn’t end there. Responsible management of your loan is crucial for building good credit and maintaining financial health.

Making Payments On Time: The Cornerstone of Good Credit

This cannot be stressed enough: consistently making your car loan payments on time is paramount.

- Impact on Credit: Payment history is the most significant factor in your credit score. Timely payments will steadily build your credit, opening doors to better rates on future loans (like mortgages) and credit cards. Late payments, conversely, can severely damage your score.

- Avoiding Fees: Late payments often incur hefty fees, adding unnecessary costs to your loan.

- Preventing Repossession: Repeatedly missing payments can lead to default and, eventually, the repossession of your vehicle.

Pro tip: Set up automatic payments from your bank account to ensure you never miss a due date. If you anticipate a problem making a payment, contact your lender immediately to discuss options.

Understanding Car Insurance for Financed Vehicles

When you finance a car, the lender has a vested interest in protecting their asset (your car). This means they will require you to carry certain types of car insurance.

- Required Coverage: Lenders typically mandate comprehensive and collision coverage, in addition to your state’s minimum liability requirements.

- Collision coverage pays for damages to your car if it hits another vehicle or object.

- Comprehensive coverage pays for damages to your car from non-collision events like theft, vandalism, fire, or natural disasters.

- Gap Insurance (Again): As discussed, if you owe more on your car than it’s worth, GAP insurance can be a lifesaver. Your lender might require it or offer to include it in your loan. Compare their offer to what your own insurance provider or a credit union might offer separately.

Based on my experience, always get insurance quotes before finalizing your car purchase. The cost can vary wildly and significantly impact your monthly budget. You can find more information on understanding car insurance from trusted sources like the National Association of Insurance Commissioners (NAIC) or consumer finance websites. (External Link: https://www.naic.org/index.htm – Please replace with a more specific NAIC consumer guide URL if available or a similar government/consumer advocacy link if preferred.)

Refinancing Options: When and Why You Might Consider It

Refinancing means taking out a new loan to pay off your existing car loan, often with a different lender and new terms.

You might consider refinancing if:

- Your Credit Score Has Improved: If your score has significantly increased since you took out your initial first time car loan, you might qualify for a lower interest rate.

- Interest Rates Have Dropped: If market rates have fallen, you could get a better deal.

- You Want a Different Loan Term: You might want to shorten the term to pay off the loan faster or lengthen it to reduce monthly payments (though the latter usually costs more in interest).

Pro tip: Don’t refinance just for a slightly lower payment. Calculate how much you’ll save in total interest over the life of the loan to determine if it’s truly beneficial.

Early Payoff Strategies: Pros and Cons

Paying off your car loan early can save you money on interest and free up monthly cash flow.

- Pros:

- Saves money on interest.

- Frees up monthly budget.

- Eliminates debt faster.

- Cons:

- You might have better uses for that extra cash (e.g., high-interest credit card debt, emergency fund, investments).

- Some loans have prepayment penalties (though rare for auto loans).

Pro tip: If you have extra cash, consider making additional principal-only payments. This directly reduces the amount you owe and thus the interest you’ll pay. Always confirm with your lender that extra payments are applied directly to the principal.

6. Special Scenarios: First Time Car Loan Without Perfect Credit

What if you’re a first time car loan applicant with no credit history, or perhaps a less-than-stellar credit score? Don’t lose hope. While the path might be different, it’s still achievable.

No Credit History: Building Your Financial Footprint

Many young adults face the challenge of securing their first loan with literally no credit history. Lenders see this as an unknown, making them hesitant.

Strategies for a first time car loan with no credit:

- Secured Car Loan: Some lenders offer secured loans specifically designed for those with no credit. The interest rates might be higher, but it’s a way to get approved and start building credit.

- Co-Signer: Having a trusted family member with good credit co-sign your loan can significantly improve your chances of approval and secure a better interest rate. We’ll delve into co-signers next.

- Build Credit First: As discussed in Section 2, use secured credit cards or small installment loans to establish a positive payment history before applying for a car loan.

- Look for "First-Time Buyer" Programs: Some dealerships or lenders offer special programs for first-time car buyers, often with more lenient credit requirements, though they might require a larger down payment.

Bad Credit: Realistic Expectations and Strategic Steps

If your credit score is low, securing a traditional loan with favorable terms will be challenging. However, it’s not impossible.

-

Realistic Expectations: Expect higher interest rates. Lenders view bad credit as a higher risk, and they compensate by charging more.

-

Explore Subprime Lenders (with Caution): Some lenders specialize in loans for individuals with bad credit. While they offer a solution, their interest rates can be very high. Thoroughly research their reputation and read reviews.

-

Focus on a Larger Down Payment: A substantial down payment reduces the lender’s risk and the amount you need to borrow, increasing your chances of approval.

-

Consider a Used, More Affordable Car: A less expensive car means a smaller loan, which is easier to get approved for and manage with bad credit.

-

Improve Your Credit First: If possible, take time to improve your credit score before applying. Pay off existing debts, dispute errors on your credit report, and make all payments on time. Even a few months of diligent effort can make a difference.

-

For a deeper dive into boosting your credit score, see our comprehensive guide:

The Role of a Co-Signer: A Helping Hand (and a Shared Risk)

A co-signer is someone with good credit who agrees to take legal responsibility for your loan if you fail to make payments.

- How it Works: The co-signer’s credit history is used in conjunction with yours, making your application stronger and potentially securing a lower interest rate.

- Benefits:

- Increases your chances of approval.

- Can lead to better loan terms and lower interest rates.

- Helps you establish your own credit history if you make timely payments.

- Risks for the Co-Signer:

- Full Responsibility: The co-signer is equally responsible for the loan. If you miss payments, their credit score will be negatively impacted, and they could be sued by the lender.

- Debt-to-Income Ratio: The loan appears on the co-signer’s credit report, potentially affecting their ability to secure their own loans in the future.

- Relationship Strain: If you default, it can severely damage your relationship with the co-signer.

Pro tip: Only ask someone you trust implicitly, and who trusts you equally, to co-sign. Ensure both parties fully understand the risks and responsibilities involved. It’s a significant favor that should not be taken lightly.

Conclusion: Driving Towards Smart Financial Decisions

Securing your first time car loan is a significant financial step that requires diligence, research, and a clear understanding of the process. By focusing on preparation, knowing your financial limits, and understanding the terms, you can navigate the complexities with confidence.

Remember, the goal isn’t just to get a car loan, but to get a smart car loan that aligns with your financial goals and helps build a strong credit foundation. From understanding APRs to avoiding unnecessary add-ons, every decision matters. Take your time, ask questions, and empower yourself with knowledge.

We hope this comprehensive guide has equipped you with the insights needed to make an informed decision. Your journey to car ownership is an exciting one – make it a financially sound one too! Drive safe, and drive smart.