Your Ultimate Guide to Securing Your First National Car Loan: Drive Away with Confidence

Your Ultimate Guide to Securing Your First National Car Loan: Drive Away with Confidence Carloan.Guidemechanic.com

The dream of owning your first car is exhilarating. It represents freedom, independence, and a significant milestone in many lives. But beneath the excitement lies a crucial step: securing a car loan. For first-time buyers, navigating the world of auto financing, especially when dealing with a reputable national lender, can feel like learning a new language. This comprehensive guide is designed to demystify the process of obtaining your First National Car Loan, ensuring you make informed decisions and drive off the lot with confidence.

Getting your first car loan is more than just signing papers; it’s about understanding a financial commitment that can impact your future. Many first-time car buyers approach this journey feeling overwhelmed, unsure of where to start or what to look out for. Our mission here is to empower you with the knowledge to not only get approved but to secure a loan that truly works for your financial situation.

Your Ultimate Guide to Securing Your First National Car Loan: Drive Away with Confidence

We’ll explore everything from preparing your finances and understanding credit scores to navigating the application process and deciphering loan terms. By the end of this deep dive, you’ll have a clear roadmap to successfully finance your first vehicle, setting a positive precedent for your financial journey ahead. Let’s embark on this exciting path together!

Understanding the Landscape: What Exactly is a "First National Car Loan"?

When we talk about a "First National Car Loan," we’re generally referring to an auto loan obtained for the first time from a large, established financial institution operating across the nation. These can include major banks, national credit unions, or well-known online lenders. The "first" aspect highlights that this is often your initial experience securing a significant loan, making it a crucial step in building your credit history.

For first-time buyers, these loans carry particular weight. They are an opportunity to establish a positive payment history, which is fundamental for future financial endeavors, from mortgages to personal loans. A national lender often provides standardized processes, competitive rates, and a broad range of options, making them a popular choice for those new to borrowing.

However, being a first-time borrower also means you might face unique challenges, such as a limited credit history. Understanding how these national lenders assess risk and what they look for in an applicant is paramount. This guide will equip you with the strategies to present yourself as a reliable borrower, even if your credit file is still in its infancy.

Chapter 1: The Essential Pre-Game: Preparing for Your First Car Loan

Before you even step foot in a dealership or fill out an online application, meticulous preparation is your greatest asset. This foundational work will not only increase your chances of approval for a First National Car Loan but also help you secure better terms.

A. Self-Assessment: What Can You Truly Afford?

One of the most critical steps in your car buying journey is a brutally honest assessment of your finances. This goes beyond just looking at the monthly payment. A car comes with numerous associated costs that can quickly add up and strain an unprepared budget.

Based on my experience, many first-time buyers overlook the total cost of car ownership. They focus solely on the sticker price or the advertised monthly payment, forgetting about the significant recurring expenses. This oversight can lead to financial stress down the line.

Start by creating a detailed budget that outlines your monthly income versus all your current expenses. Factor in rent, utilities, groceries, student loan payments, and any other regular outgoings. This will reveal how much disposable income you genuinely have available for car-related costs.

Remember to account for more than just the loan payment itself. You’ll need to budget for car insurance, which can be surprisingly high for new drivers, especially with a financed vehicle. Don’t forget fuel costs, routine maintenance (oil changes, tire rotations), and potential unexpected repairs. A realistic budget ensures your first car loan enhances your life, rather than becoming a burden.

B. Understanding Your Credit Score: Your Financial Report Card

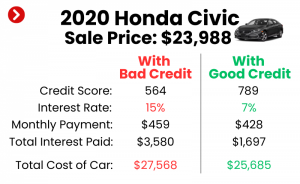

Your credit score is a three-digit number that lenders use to assess your creditworthiness. It’s essentially your financial report card, summarizing your history of borrowing and repaying debt. For a First National Car Loan, your credit score will heavily influence whether you get approved and what interest rate you’re offered.

Lenders use your score to gauge the risk associated with lending you money. A higher score indicates a lower risk, often leading to more favorable interest rates and better loan terms. Conversely, a lower score might result in higher interest rates or even a denial of your application.

It’s crucial to check your credit score and review your credit report before applying for any loan. You can obtain a free copy of your credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) once every 12 months via AnnualCreditReport.com. This allows you to identify any errors and understand your current financial standing.

Pro tip from us: Improving your credit score even slightly before applying can save you thousands of dollars over the life of your car loan. Pay down existing debts, ensure all bills are paid on time, and avoid opening new lines of credit in the months leading up to your car loan application.

C. Saving for a Down Payment: The Power of Upfront Cash

While it’s possible to get a car loan with no down payment, providing one offers significant advantages, especially for a first-time buyer. A down payment is the initial amount of money you pay upfront towards the purchase of the car, reducing the total amount you need to borrow.

The benefits of a down payment are manifold. Firstly, it lowers your monthly loan payments, making the car more affordable on a day-to-day basis. Secondly, it reduces the total interest you’ll pay over the life of the loan, saving you money in the long run.

Perhaps most importantly for a First National Car Loan applicant, a down payment can improve your chances of approval and help you secure a better interest rate. It demonstrates to lenders that you are serious about the purchase and have some financial stability. Lenders view a substantial down payment as a sign of reduced risk.

Common mistakes to avoid are trying to finance 100% of the car’s value, especially if you have limited credit history. This often leads to higher interest rates and a longer loan term, potentially putting you in an "upside-down" position where you owe more than the car is worth. Aim for at least 10-20% of the car’s purchase price as a down payment if possible.

Chapter 2: Navigating the Loan Process: Step-by-Step for First-Timers

With your finances in order and a clear understanding of your credit, you’re ready to dive into the loan application process. This chapter will guide you through finding the right lender and preparing for a smooth application.

A. Researching Lenders: Where to Find Your "First National Car Loan"

The landscape of auto lenders is diverse, and it’s essential to explore your options beyond just the dealership. While dealership financing can be convenient, it’s not always the most cost-effective choice. Your goal is to find the best possible terms for your First National Car Loan.

Major banks are a common source for auto loans. They offer a range of loan products and often have competitive rates for well-qualified buyers. Credit unions, on the other hand, are member-owned and frequently offer lower interest rates and more personalized service due to their non-profit structure.

Online lenders have also emerged as strong contenders, providing quick pre-approvals and streamlined application processes. It’s advisable to compare offers from several types of lenders before committing. Each will have different criteria and rates, so shopping around is crucial to secure the most favorable terms.

B. Pre-Approval: Your Secret Weapon

Pre-approval is a game-changer for first-time car buyers. It’s when a lender reviews your financial information and tentatively agrees to lend you a certain amount of money at a specific interest rate, before you’ve even chosen a car. This process usually involves a "soft" credit inquiry, which won’t impact your credit score.

The benefits of getting pre-approved for your First National Car Loan are immense. Firstly, it gives you a clear budget, so you know exactly how much car you can afford. This prevents you from falling in love with a vehicle that’s out of your price range.

Secondly, pre-approval transforms you into a cash buyer at the dealership. You walk in with your financing already secured, giving you significant negotiating power on the car’s price. You can focus solely on getting the best deal on the vehicle, rather than getting caught up in financing discussions.

To get pre-approved, you’ll typically fill out an application online or in person, providing details about your income, employment, and credit history. The lender will then provide you with a pre-approval letter stating the loan amount, interest rate, and term you qualify for.

C. Gathering Your Documents: Be Prepared

Once you’re ready to apply for your First National Car Loan, having all your necessary documents prepared in advance will make the process much smoother and faster. Delays often occur when applicants are missing key pieces of information.

Lenders will require various documents to verify your identity, income, and residence. You’ll typically need a valid government-issued photo ID, such as a driver’s license or passport. Proof of income is crucial, which usually means recent pay stubs (last 2-3 months), W-2 forms, or tax returns if you’re self-employed.

Proof of residence, such as a utility bill or bank statement with your current address, is also commonly requested. Additionally, lenders will want to see proof of insurance once you’ve chosen a vehicle, as it’s mandatory for financed cars.

Based on my experience, having all your documents ready and organized streamlines the application process significantly. It shows the lender you are prepared and serious, which can reflect positively on your application. A simple checklist can help you keep everything in order.

Chapter 3: Decoding the Terms: What to Look For in Your First Car Loan Agreement

Understanding the language of your loan agreement is vital. Don’t just focus on the monthly payment; delve into the details of your First National Car Loan to ensure you’re getting a fair deal and fully comprehending your commitment.

A. Interest Rates (APR): The Cost of Borrowing

The interest rate is arguably the most critical factor in your car loan. It’s the cost you pay to borrow the money, expressed as a percentage of the loan amount. When comparing loan offers, always look at the Annual Percentage Rate (APR), which includes the interest rate plus any additional fees, giving you a truer picture of the loan’s total cost.

Several factors influence the interest rate you’ll be offered for your First National Car Loan. Your credit score is paramount; a higher score typically qualifies you for lower rates. The loan term, down payment amount, and even the type of car (new vs. used) can also play a role.

Interest rates can be either fixed or variable. With a fixed rate, your interest rate remains the same throughout the life of the loan, providing predictable monthly payments. Variable rates, while sometimes starting lower, can fluctuate with market conditions, making your payments less stable. For a first-time borrower, a fixed rate often offers more peace of mind.

B. Loan Term: How Long Will You Be Paying?

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). The term significantly impacts both your monthly payment and the total interest you’ll pay over the life of the loan.

A shorter loan term means higher monthly payments but less interest paid overall. This is because you’re paying off the principal more quickly, giving interest less time to accrue. Conversely, a longer loan term results in lower monthly payments, making the car seem more affordable in the short term.

However, longer terms also mean you’ll pay significantly more in total interest. For a First National Car Loan, finding the sweet spot between an affordable monthly payment and minimizing total interest paid is key. While a 72 or 84-month loan might offer very low monthly payments, it often means paying thousands more in interest and potentially being upside down on your loan for a longer period.

C. Fees and Charges: Hidden Costs to Uncover

Beyond the interest rate, be vigilant for various fees and charges that can be tacked onto your First National Car Loan. These can sometimes inflate the overall cost of borrowing and should be factored into your decision-making.

Common fees include origination fees, which are charges for processing the loan, and documentation fees, which cover the cost of preparing the paperwork. Some loans might also include prepayment penalties, which are fees charged if you pay off your loan early. This is less common with auto loans but still worth checking.

Pro tip from us: Always ask for a full breakdown of all fees associated with the loan. Reputable lenders will be transparent about these costs. Don’t hesitate to question any fee you don’t understand or feel is excessive. Sometimes, certain fees can be negotiated or waived.

D. Understanding the Fine Print: Read Before You Sign

The loan agreement is a legally binding document. It contains all the terms and conditions of your First National Car Loan, including interest rates, payment schedules, late payment penalties, and what happens in case of default. It is absolutely crucial that you read and understand every single clause before you sign.

Do not feel rushed or pressured by the lender or dealership to sign immediately. Take your time to review the entire document thoroughly. If there’s anything you don’t understand, ask for clarification. A reputable lender will be happy to explain any complex terms.

Common mistakes to avoid are signing without fully comprehending the commitment or assuming certain terms are implied. If it’s not in writing, it’s not part of the agreement. This diligence will protect you from unexpected surprises and ensure your first car loan experience is a positive one.

Chapter 4: Special Considerations for First-Time Car Loan Applicants

As a first-time borrower, you might encounter unique challenges and opportunities. Understanding these special considerations can help you navigate the process more effectively and establish a strong financial foundation.

A. Building Credit with Your First Loan

Your First National Car Loan is more than just a means to get a car; it’s a powerful tool for building your credit history. Making timely payments on a significant loan like an auto loan demonstrates financial responsibility and contributes positively to your credit score.

Payment history is the most significant factor in calculating your credit score. By consistently making your car loan payments on time, every time, you’ll establish a solid track record that future lenders will look upon favorably. This can pave the way for easier access to other forms of credit, like mortgages or personal loans, down the road.

The importance of consistency cannot be overstated. Even a single late payment can negatively impact your credit score and remain on your credit report for years. Treat your first car loan as an opportunity to prove your reliability as a borrower.

B. Dealing with Limited or No Credit History

Many first-time car buyers have limited or no credit history, which can make securing a First National Car Loan challenging. Lenders rely on credit history to assess risk, and without it, you might be seen as an unknown quantity.

One common strategy for those with limited credit is to apply with a co-signer. A co-signer is someone with good credit who agrees to be equally responsible for the loan if you fail to make payments. This can significantly increase your chances of approval and help you secure a better interest rate. However, ensure both you and your co-signer understand the full implications; if you default, their credit will also be damaged.

Another option might be a secured loan, where the car itself acts as collateral. While these might be easier to obtain, ensure you understand the terms. Some lenders also offer specific programs for first-time buyers or recent graduates, so inquire about these.

Common mistakes to avoid are jumping into a large loan with no credit without a co-signer or proper preparation. Starting with a smaller, more affordable first car can also be a wise move, allowing you to build credit more safely before taking on a larger financial commitment.

C. The Role of Car Insurance

Car insurance is not just a legal requirement in most places; it’s an absolute necessity, especially when you have a financed vehicle. Lenders require you to carry comprehensive and collision insurance to protect their investment (the car) in case of an accident, theft, or damage.

The cost of car insurance needs to be a significant line item in your car budget. For first-time drivers or those new to owning a car, insurance premiums can be quite high. Factors like your age, driving record, the type of car you buy, and even your credit score can influence your rates.

Before finalizing your First National Car Loan and purchasing a car, get multiple insurance quotes. This will give you a realistic idea of the ongoing costs and help you avoid any budget surprises. Remember, the monthly loan payment is only one piece of the car ownership puzzle.

Chapter 5: After Approval: Making the Most of Your First Car Loan

Congratulations, you’ve secured your First National Car Loan and driven away in your new vehicle! But the journey doesn’t end there. Responsible management of your loan and vehicle will ensure a positive financial future and protect your investment.

A. Making Timely Payments: The Golden Rule

This cannot be stressed enough: consistently making your car loan payments on time is the single most important action you can take. It’s the golden rule of credit building and financial responsibility. Every on-time payment reinforces your creditworthiness and helps improve your credit score.

Consider setting up automatic payments from your bank account to avoid missing deadlines. This eliminates the risk of forgetting a payment and incurring late fees or, worse, damaging your credit history. Monitor your bank statements and loan statements regularly to ensure everything is processed correctly.

Your First National Car Loan is a significant financial commitment, and treating it with the respect it deserves will pay dividends in your financial future. A spotless payment record will open doors to better rates and terms on future loans.

B. Refinancing Opportunities

Over time, your financial situation and credit score might improve significantly. This could open up opportunities to refinance your First National Car Loan. Refinancing involves taking out a new loan to pay off your existing one, often with more favorable terms.

It makes sense to consider refinancing if your credit score has improved since you first took out the loan, or if interest rates have dropped. A lower interest rate could significantly reduce your monthly payments or the total amount of interest you pay over time.

Typically, it’s wise to wait about 6-12 months after starting your loan to consider refinancing, giving your credit score a chance to reflect your positive payment history. Always compare potential refinancing offers carefully, looking at the new interest rate, term, and any associated fees.

C. Protecting Your Investment

Your car is a valuable asset, and for a financed vehicle, it’s also collateral for your loan. Protecting this investment is crucial. Regular maintenance, as recommended by the manufacturer, will keep your car running smoothly and help retain its value.

Beyond basic maintenance, consider the value of Gap Insurance. This insurance covers the "gap" between what you owe on your loan and what your car is worth if it’s totaled or stolen. Cars depreciate quickly, and it’s common to owe more than the car is worth, especially in the early years of a loan. Gap insurance protects you from this financial shortfall.

Your First National Car Loan enables you to own a car, but responsible ownership extends to maintaining the vehicle itself. A well-maintained car is not only safer and more reliable but also holds its value better, which is beneficial if you decide to sell or trade it in later.

Conclusion: Driving Towards a Confident Financial Future

Securing your First National Car Loan is a significant step, marking your entry into the world of major financial commitments. As we’ve explored, this journey is much smoother and more rewarding when approached with thorough preparation, a clear understanding of the process, and a commitment to responsible financial habits.

From diligently assessing your affordability and bolstering your credit score to navigating lender options and deciphering loan agreements, every step plays a crucial role. Remember, your first car loan is not just about getting a set of keys; it’s a powerful opportunity to establish a positive credit history that will serve you well for years to come.

By taking the time to educate yourself, asking the right questions, and being proactive in managing your loan, you’re not just securing a car—you’re building a foundation for a confident financial future. Drive away knowing you made an informed decision, ready to enjoy the freedom your first car brings.

For more insights into managing your finances and making smart purchasing decisions, explore our other articles like "Mastering Your Budget: Essential Tips for Smart Spending" or learn how to boost your financial health with "Unlocking Your Potential: A Comprehensive Guide to Improving Your Credit Score". For reliable information on credit reports and scores, visit the Consumer Financial Protection Bureau at consumerfinance.gov. Your journey to financial literacy has just begun, and we’re here to guide you every step of the way.